Market Week Ahead (July 13 – 17): US Inflation to Test the Market's Optimism

15 minutes for reading

The past week ended without fresh signals from the Federal Reserve. Minutes from the June meeting confirmed the regulator's cautious stance: most Fed officials still consider it premature to discuss rate cuts and want to see more convincing evidence that inflation is slowing. The message supported the dollar and led the market to fully abandon expectations of rapid policy easing.

Geopolitical risk returned to the spotlight as well. Tensions around the Strait of Hormuz rose after new incidents in the region, bringing a risk premium back into oil prices. Diplomatic efforts between the US and Iran continue, but the possibility of fresh supply disruptions remains a factor that could push inflation expectations higher.

In the week ahead, market attention will centre on US inflation, Chinese economic statistics, the Bank of Canada rate decision, UK GDP and US retail sales. Together, these releases will help investors gauge the resilience of the global economy and assess how justified current expectations are regarding the next steps of the major central banks.

In Brief

- US CPI (Tuesday, July 14) — the main event of the week. After the firm tone of the Fed minutes, the June report will determine whether the high-rates scenario holds through year-end.

- China GDP, Industrial Production and Retail Sales (Wednesday, July 15) — a broad check on how steadily the world's second-largest economy is recovering.

- Bank of Canada Rate Decision (Wednesday, July 15) — the rate is expected to stay unchanged, so the updated forecast and the regulator's comments will drive the Canadian dollar.

- UK GDP (Thursday, July 16) — a key test of the British economy's resilience after an unexpected dip in activity the previous month.

- US Retail Sales (Friday, July 17) — the closing report of the week, showing whether the American consumer stays active after the inflation data lands.

Key Events of the Week

| Date | Event | Instruments | Importance |

|---|---|---|---|

| Tue, Jul 14 | US Consumer Price Index (CPI) | S&P 500, Nasdaq 100, US Dollar Index | ●●● High |

| Wed, Jul 15 | China GDP + Industrial Production + Retail Sales | AUD/USD, Iron Ore, Copper | ●●● High |

| Wed, Jul 15 | Bank of Canada Rate Decision | USD/CAD, Canadian bonds, Brent | ●● Medium |

| Thu, Jul 16 | UK GDP | GBP/USD, FTSE 100, UK gilts | ●● Medium |

| Fri, Jul 17 | US Retail Sales | EUR/USD, US Dollar Index, US Treasuries | ●●● High |

Instant Access to Global Markets with RoboForex MobileTrader

14

Jul

Forecast

3.9% y/y

Previous

4.2% y/y

Why It Matters

Consumer inflation is the Federal Reserve's main reference point for interest rate decisions. After the firm tone of the June meeting minutes, the market has practically given up on expectations of an early rate cut. The June CPI report will now show whether progress in the fight against inflation continues or whether price pressure is starting to build again. Investors will pay particular attention to core inflation, which better reflects underlying price trends by excluding volatile components. Any deviation from the consensus could substantially reshape market expectations for future Fed policy.

Market Reaction

A softer-than-expected reading would confirm that disinflation remains on track and support demand for US stocks. A stronger print would revive expectations of additional policy tightening, add pressure on stock indices and strengthen the dollar. Watch the S&P 500, Nasdaq 100 and the US Dollar Index for the sharpest moves.

Market Sentiment

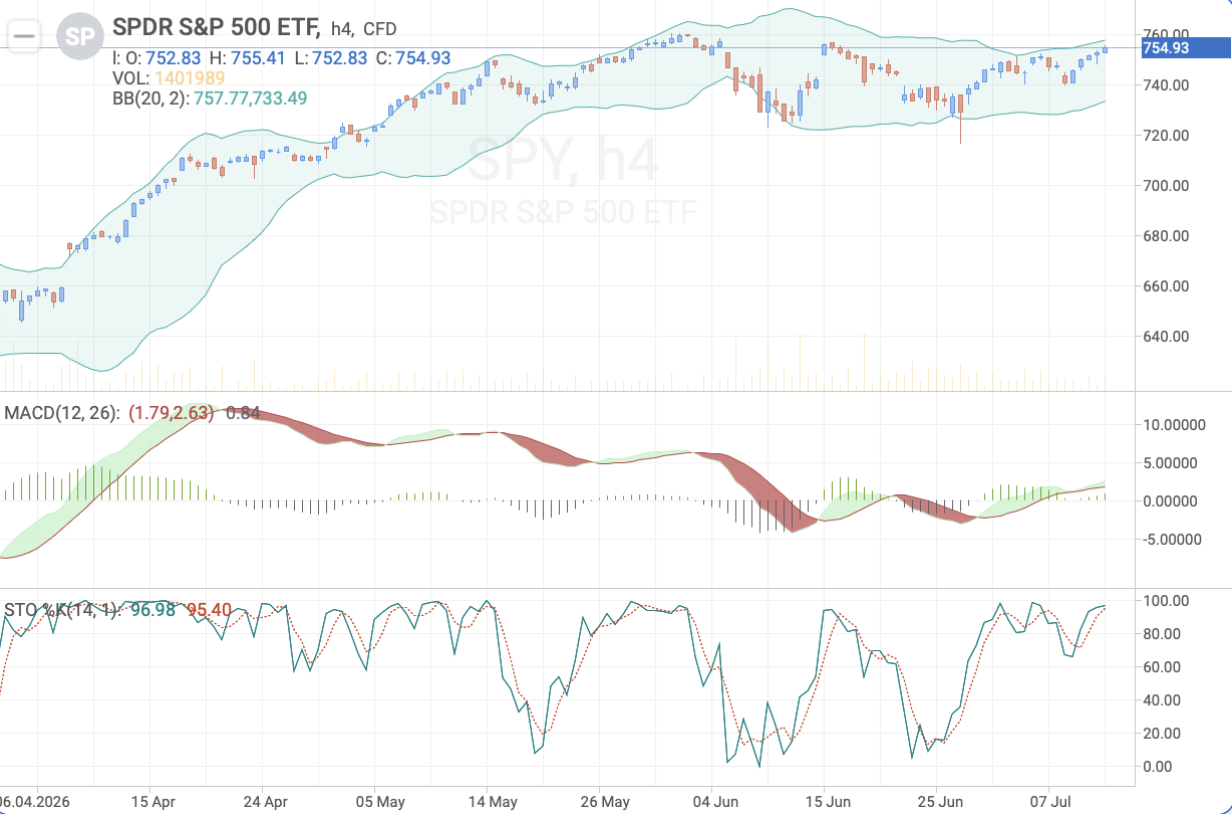

Consensus remains moderately positive for US stocks, provided inflation keeps cooling. After the firm Fed minutes, however, the market has become considerably more sensitive to any inflation surprise. On the chart, the S&P 500 holds near record highs, but upward momentum is gradually fading. MACD stays in positive territory while its histogram declines, signalling a loss of bullish drive. A high inflation print would trigger profit-taking and return the index to support at 740.

Source: RoboForex. Past performance is not indicative of future results.

Key Levels — S&P 500

| Level | Value |

|---|---|

| Resistance | 760.00 / 765.00 |

| Support | 748.00 / 740.00 |

| Target | 740.00 |

15

Jul

GDP Forecast

4.7% y/y

Previous

5.0% y/y

Why It Matters

China remains the world's largest consumer of raw materials and one of the key drivers of the global economy. Alongside GDP, investors will receive industrial production and retail sales figures, giving a full picture of domestic demand and the pace of economic recovery. For commodity currencies, Chinese statistics often become the main driver of price action: any sign of a slowdown would add pressure on the Australian dollar, while strong data would support demand for risk assets.

Market Reaction

A stronger GDP print would lift AUD/USD along with iron ore and copper prices. Weaker figures would confirm the slowdown scenario and weigh on commodity currencies and industrial metals.

Market Sentiment

Consensus remains cautious. After a series of mixed macroeconomic reports, the market expects further cooling of the Chinese economy, so a strong GDP reading would support risk appetite and strengthen the Australian dollar. On the chart, AUD/USD is gradually recovering after the June decline and holds above support at 0.6930. MACD has moved back into positive territory, signalling improving short-term momentum. Strong Chinese statistics would push the pair toward a test of the psychological 0.7000 level.

Source: RoboForex. Past performance is not indicative of future results.

Key Levels — AUD/USD

| Level | Value |

|---|---|

| Resistance | 0.6970 / 0.7000 |

| Support | 0.6930 / 0.6900 |

| Target | 0.7000 |

15

Jul

Forecast

2.25%

Previous

2.25%

Why It Matters

After several months of policy easing, the Bank of Canada is most likely to keep its interest rate unchanged. The market's focus will therefore shift to the updated Monetary Policy Report and the regulator's comments on inflation, the economy and the future path of rates. Additional attention will go to the Bank's assessment of how oil prices and trade uncertainty affect the Canadian economy. Any change in rhetoric would meaningfully reshape market expectations for the next meetings.

Market Reaction

If the regulator opens the door to further easing in the second half of the year, the Canadian dollar would come under pressure. Firmer language on rates would support CAD, moving USD/CAD lower and lifting yields on Canadian government bonds. Brent prices form the backdrop for both scenarios.

Market Sentiment

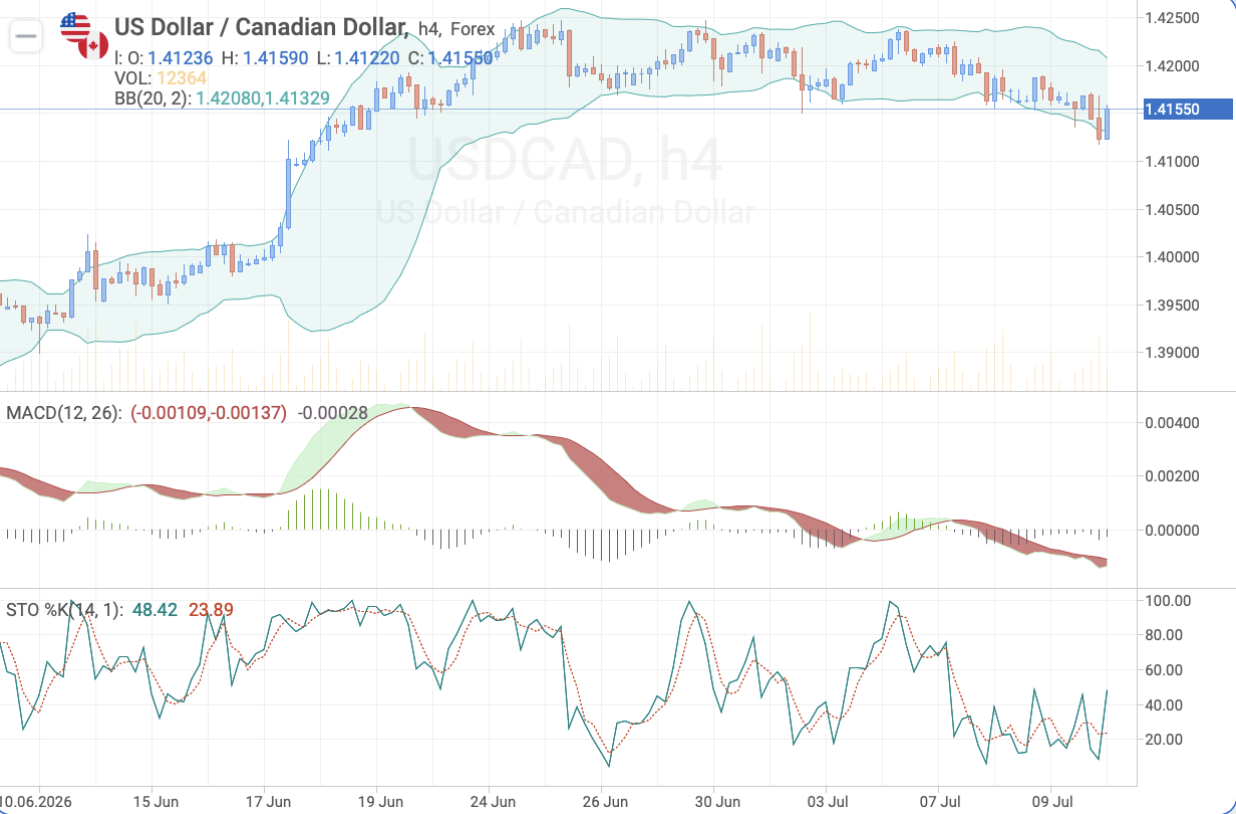

Consensus remains neutral. The base case is a hold at 2.25%, so the main driver of price action will come from the Bank of Canada's comments. On the chart, USD/CAD is gradually correcting after the June rally and testing support around 1.4120. MACD stays in negative territory, reflecting a weakening of the upward impulse. If the Bank of Canada keeps a firmer tone, pressure on the pair would build with a downside target of 1.4080.

Source: RoboForex. Past performance is not indicative of future results.

Key Levels — USD/CAD

| Level | Value |

|---|---|

| Resistance | 1.4180 / 1.4220 |

| Support | 1.4120 / 1.4080 |

| Target | 1.4080 |

16

Jul

Forecast

+0.1% m/m

Previous

−0.1% m/m

Why It Matters

The UK economy remains one of the most sensitive among G7 countries to high interest rates. After the unexpected GDP contraction in the previous month, investors will assess whether the slowdown was temporary or whether the economy is genuinely losing momentum. The release will be one of the last major reference points for the Bank of England ahead of its next meeting and will help fine-tune expectations for future monetary policy.

Market Reaction

A return to growth would lower expectations of early Bank of England rate cuts and support the pound, GBP/USD and UK gilt yields. Another weak reading would reinforce the slowdown scenario and add pressure on the British currency while giving the FTSE 100 exporters a relative lift.

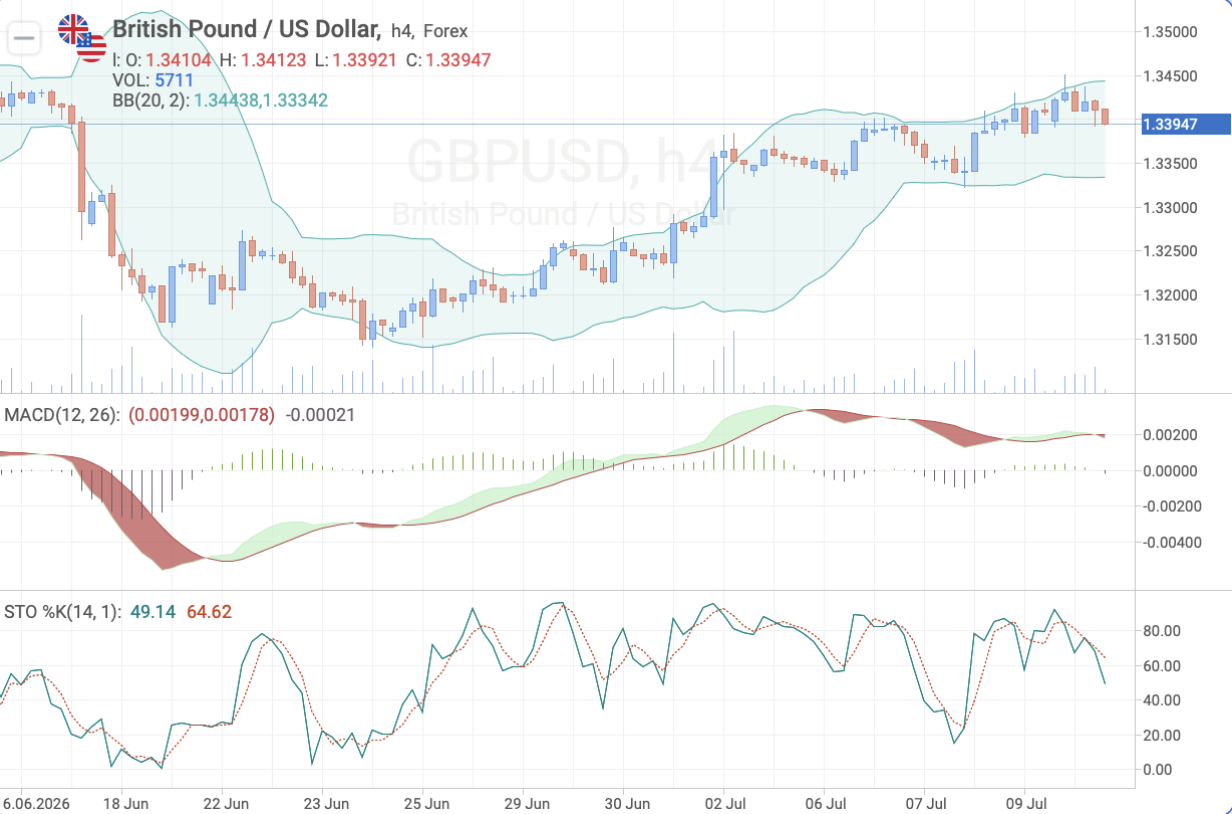

Market Sentiment

Consensus remains cautiously positive for the pound, with the economy expected to return to moderate growth after the weak May report. On the chart, GBP/USD stays within an uptrend, though the pace of gains has slowed after the pair refreshed local highs. MACD is gradually losing upward momentum, which raises the probability of a correction. Weak GDP data would return the pair to support at 1.3330.

Source: RoboForex. Past performance is not indicative of future results.

Key Levels — GBP/USD

| Level | Value |

|---|---|

| Resistance | 1.3450 / 1.3500 |

| Support | 1.3380 / 1.3330 |

| Target | 1.3330 |

17

Jul

Forecast

+0.5% m/m

Previous

+0.9% m/m

Why It Matters

Retail sales are one of the key indicators of consumer activity, which generates almost 70% of the American economy. Coming after the inflation data, this report will show whether domestic demand stays resilient against the backdrop of high interest rates. Strong sales would confirm the strength of the US economy and support the dollar. Weak statistics would reinforce expectations of a gradual cooling in economic activity and reshape market expectations for future Fed policy.

Market Reaction

A beat would strengthen the dollar and push Treasury yields higher, pressuring EUR/USD. A miss would add pressure on the US Dollar Index and open room for a corrective rebound in major currency pairs.

Market Sentiment

Consensus remains moderately positive for the dollar. Despite the gradual cooling of inflation, the American consumer still shows high activity. If sales exceed the forecast again, the market may fully abandon expectations of an early Fed rate cut; a weak report would increase pressure on the dollar instead. On the chart, EUR/USD continues to trade in a wide sideways range after the June recovery. MACD is gradually losing positive momentum, and buyers have yet to secure a foothold above resistance at 1.1450. If US statistics beat expectations once again, the pair may resume its decline with a nearby target around 1.1360.

Source: RoboForex. Past performance is not indicative of future results.

Key Levels — EUR/USD

| Level | Value |

|---|---|

| Resistance | 1.1450 / 1.1480 |

| Support | 1.1400 / 1.1360 |

| Target | 1.1360 |

Track the forecasts and actual figures for each event — the gap between consensus and actual readings is what determines how sharply prices move. Learn more about how to read the economic calendar and trade the news.

Conclusion

The week builds from Tuesday's US inflation report, which sets the tone for everything that follows. Wednesday brings a double dose of central bank and macro input with Chinese statistics and the Bank of Canada decision, Thursday tests the UK economy, and Friday's retail sales close the week with a verdict on the American consumer.

The combination of a cooling CPI and steady retail sales would confirm the soft-landing scenario and support demand for stocks and risk assets. A hot inflation print, on the other hand, would revive the high-rates narrative, strengthen the dollar and put stock indices under pressure. With tensions around the Strait of Hormuz keeping a risk premium in oil prices, inflation expectations carry extra weight this week, and the market's reaction to Tuesday's report will shape trading well into the second half of July.

Any information provided in articles on this website is based solely on the personal opinions of the authors. These articles should not be construed as trading recommendations or a call to action. The authors and RoboForex accept no responsibility for the results of any trades made on the basis of these recommendations and reviews. Past performance is not indicative of future results. Trading stocks and CFDs involves a high risk of capital loss.