Market Week Ahead (June 29 – July 3): Jobs Data to Set the Dollar's Course into July

Oil markets stabilised at the end of last week as Middle East tensions eased and traders unwound much of the geopolitical premium that had supported Brent through the first half of June. With conflict risk fading from prices, attention has returned to macro fundamentals: the supply-demand balance, the global growth outlook and OPEC+ strategy. The calendar is heavy with US labour data: JOLTS on Tuesday and Non-Farm Payrolls on Thursday, the latter brought forward from its usual Friday slot for the US Independence Day holiday. Below we work through the main releases — Eurozone flash inflation and Australia's manufacturing PMI on Wednesday, then Thursday's payrolls — with the technical levels and market sentiment that matter for each asset.

In Brief

- JOLTS and Consumer Confidence (Tuesday, June 30) — early read on labour demand ahead of Thursday's main event.

- Eurozone Flash CPI (Wednesday, July 1) — key inflation signal for ECB rate expectations; central bank speakers including Powell and Lagarde add intraday risk.

- Australia Manufacturing PMI (Wednesday, July 1) — first major Australian macro release of July, with China data adding context.

- Non-Farm Payrolls and Unemployment Rate (Thursday, July 2) — the week's defining release for the dollar, equities and gold.

- OPEC+ Meeting (Sunday, July 5) — output decision will set the tone for oil at Monday's open.

Eurozone flash CPI on Wednesday adds a European dimension to the week. Any deviation from the 3.2% consensus would shift ECB rate expectations and move EUR/USD. Scheduled commentary from Fed Chair Powell, ECB President Lagarde and Bank of England Governor Bailey will add intraday volatility to an already data-dense session.

OPEC+ meets on Sunday, July 5 after the trading week closes, but the alliance's output decision will shape the mood in oil markets at Monday's open. With geopolitical risk largely absent from prices, the focus shifts back to supply strategy and the demand outlook.

Key Events of the Week

| Date | Event | Instruments | Importance |

|---|---|---|---|

| Tue, Jun 30 | US JOLTS + Consumer Confidence | S&P 500, USD Index, US Treasuries | ●● Medium |

| Wed, Jul 1 | Eurozone Flash CPI | EUR/USD, DAX, European bonds | ●●● High |

| Wed, Jul 1 | Australia Manufacturing PMI | AUD/USD, Australian bonds, Iron Ore | ●● Medium |

| Thu, Jul 2 | US Non-Farm Payrolls + Unemployment Rate | S&P 500, USD Index, Gold, US Treasuries | ●●● High |

| Sun, Jul 5 | OPEC+ Meeting | Brent, WTI, USD/CAD, Oil & Gas equities | ●●● High |

Instant Access to Global Markets with RoboForex MobileTrader

30

Jun

JOLTS Forecast

7.60M

Previous

7.681M

Why It Matters

The JOLTS report is a reliable leading indicator of US labour market conditions. It measures the number of open positions and captures employer demand for workers before the official employment data hits. Paired with the Conference Board Consumer Confidence index on the same day, these figures help set market expectations ahead of Thursday's Non-Farm Payrolls — the week's defining release.

Market Reaction

Strong data would confirm US economic resilience and support the case for rates staying elevated. A softer reading would point to early labour-market cooling, shifting sentiment toward risk assets and adding pressure on the dollar ahead of Thursday's payrolls.

Market Sentiment

Broader sentiment on the US economy remains moderately positive. After a strong May jobs report, most investors expect labour demand to hold up despite elevated borrowing costs, even as the market accepts that a gradual cooling in hiring is exactly what the Fed wants to see before it can be confident inflation is heading back to target. A firm JOLTS number would strengthen the "higher for longer" case into Thursday, while a soft one would count as the first concrete sign of labour-market easing. On the chart, the S&P 500 is consolidating after June's correction, holding above support as MACD recovers from its recent dip; solid US data would open the way for a retest of the 750 resistance area.

Source: RoboForex. Past performance is not indicative of future results.

Key Levels — S&P 500

| Level | Value |

|---|---|

| Resistance | 745.00 / 750.00 |

| Support | 725.00 / 715.00 |

| Target | 750.00 |

1

Jul

Forecast

3.2% y/y

Previous

3.2% y/y

Why It Matters

Wednesday's flash CPI estimate is the week's leading European macro release. Following the ECB's June meeting, markets continue to assess the likelihood of further policy adjustments in the second half of the year. Any deviation from the 3.2% consensus would directly feed into ECB rate forecasts and move the euro. Scheduled remarks from ECB President Lagarde, Fed Chair Powell and Bank of England Governor Bailey on the same day will amplify intraday volatility across FX markets.

Market Reaction

An above-consensus CPI reading would support the euro and reduce the probability of near-term ECB easing. A miss would reinforce expectations of continued rate cuts and weigh on EUR/USD. The euro's reaction to the central bank speakers could rival the CPI release itself if any of them signals a shift in policy direction.

Market Sentiment

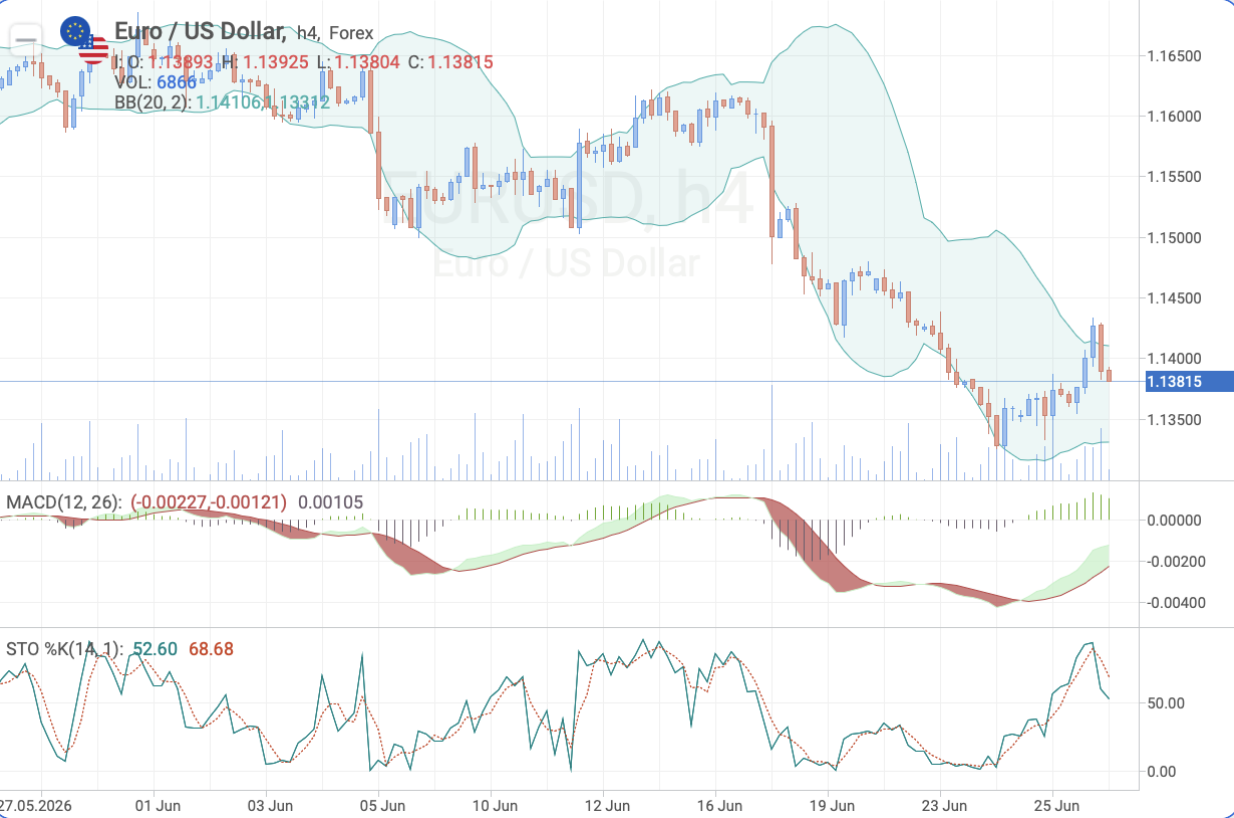

Consensus on EUR/USD remains moderately negative. Despite gradual inflation stabilisation, the Eurozone economy is growing slowly, which limits the ECB's room to keep policy restrictive. Most participants expect the easing cycle to continue. A renewed inflation uptick would force a reassessment of that view and provide the euro with a short-term boost. EUR/USD is trading inside a descending channel following the dollar's recovery in the second half of June. MACD is gradually stabilising, but buying momentum remains weak. While the pair holds below the 1.1450 resistance, a retest of nearby support looks the more likely path. A CPI beat would support a corrective bounce; a miss would accelerate the move toward 1.1280.

Source: RoboForex. Past performance is not indicative of future results.

Key Levels — EUR/USD

| Level | Value |

|---|---|

| Resistance | 1.1450 / 1.1500 |

| Support | 1.1330 / 1.1280 |

| Target | 1.1280 |

1

Jul

Forecast

51.6

Previous

50.7

Why It Matters

The manufacturing PMI is the first significant Australian macro release of July. As a timely gauge of new orders, output, employment and business activity, it gives markets an early read on the economy's trajectory before official data arrives. The 50-point threshold separating expansion from contraction makes any reading above or below it an immediate signal for AUD. China's PMI data, released a few hours earlier, will provide additional context — China remains Australia's largest trading partner, and any weakness there tends to weigh on the Australian dollar ahead of the domestic release.

Market Reaction

A PMI above forecast would support AUD/USD and strengthen the case for a more durable economic recovery. A reading below expectations would add to selling pressure on the Australian dollar and revive concerns about the pace of industrial recovery, with iron ore also sensitive to the result.

Market Sentiment

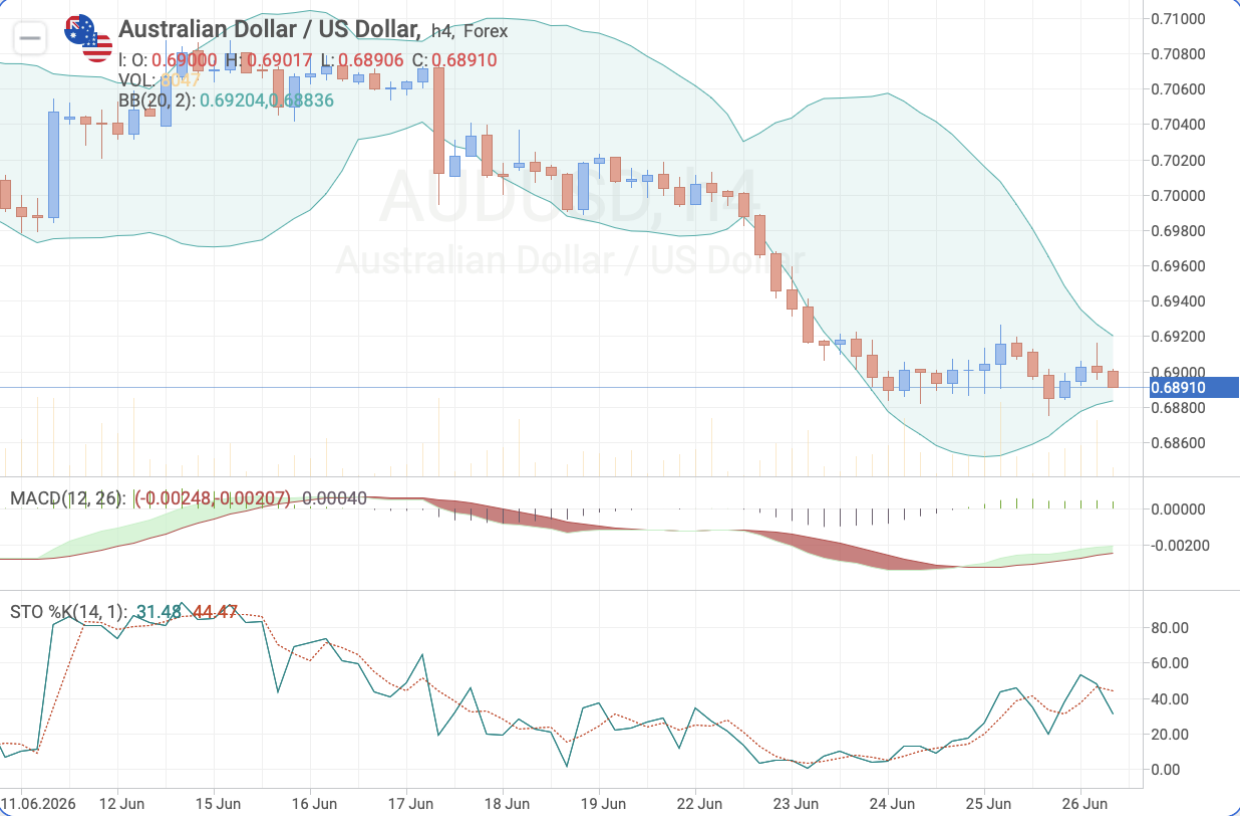

Consensus on AUD/USD is neutral with a modest downside bias. The preliminary June PMI reading of 51.2 already pointed to improving manufacturing activity, but new orders remain soft and output has continued to contract despite the headline gain. Investors want confirmation that the recovery is broadening. A final reading at or above the 51.6 forecast would provide that confirmation and give the Australian dollar room to recover. AUD/USD has been grinding lower since a failed recovery attempt late in June. MACD is still negative, though the bearish momentum is gradually fading. A sustained move below 0.6920 would keep 0.6840 within reach on the downside. A strong PMI would trigger a short-term bounce; the medium-term trend would need more than one data point to reverse.

Source: RoboForex. Past performance is not indicative of future results.

Key Levels — AUD/USD

| Level | Value |

|---|---|

| Resistance | 0.6920 / 0.6950 |

| Support | 0.6880 / 0.6840 |

| Target | 0.6840 |

2

Jul

NFP Forecast / Unemployment

+90K / 4.5%

Previous

+172K / 4.3%

Why It Matters

The monthly jobs report is among the most market-moving macro releases on the calendar. Employment conditions feed directly into Fed rate decisions, and with the holiday schedule pushing the release to Thursday, it will be the focal point of the entire week. Both the headline payrolls figure and the unemployment rate deserve attention: the first shows how many jobs were created, the second shows whether broader labour market conditions are beginning to ease. A rise in unemployment to 4.5% alongside a soft payrolls number would be the clearest signal yet that the US economy is cooling under the weight of elevated rates.

Market Reaction

A strong report would reinforce expectations for rates staying high and give the dollar a boost into the July 4 holiday weekend. A weak reading would sharpen rate-cut expectations for later in the year and support demand for risk assets and gold. With market liquidity thinner than usual heading into the US holiday, price moves in either direction could be amplified.

Market Sentiment

Dollar sentiment remains moderately bullish. After May's jobs report significantly beat expectations, most investors expect another confirmation of US economic resilience. The bar is high, however: expectations are already elevated, so even a modest miss could trigger meaningful profit-taking on long dollar positions. A report showing solid job creation with stable unemployment would keep the "higher for longer" narrative intact and support dollar-positive trades across major pairs. The S&P 500 has spent the past sessions rebuilding its uptrend after June's correction, with buyers defending the 725–715 zone. A strong payrolls print would push the index back toward 750 resistance; a weak one would put that support range back under pressure.

Source: RoboForex. Past performance is not indicative of future results.

Key Levels — S&P 500

| Level | Value |

|---|---|

| Resistance | 745.00 / 750.00 |

| Support | 725.00 / 715.00 |

| Target | 750.00 |

5

Jul

Why It Matters

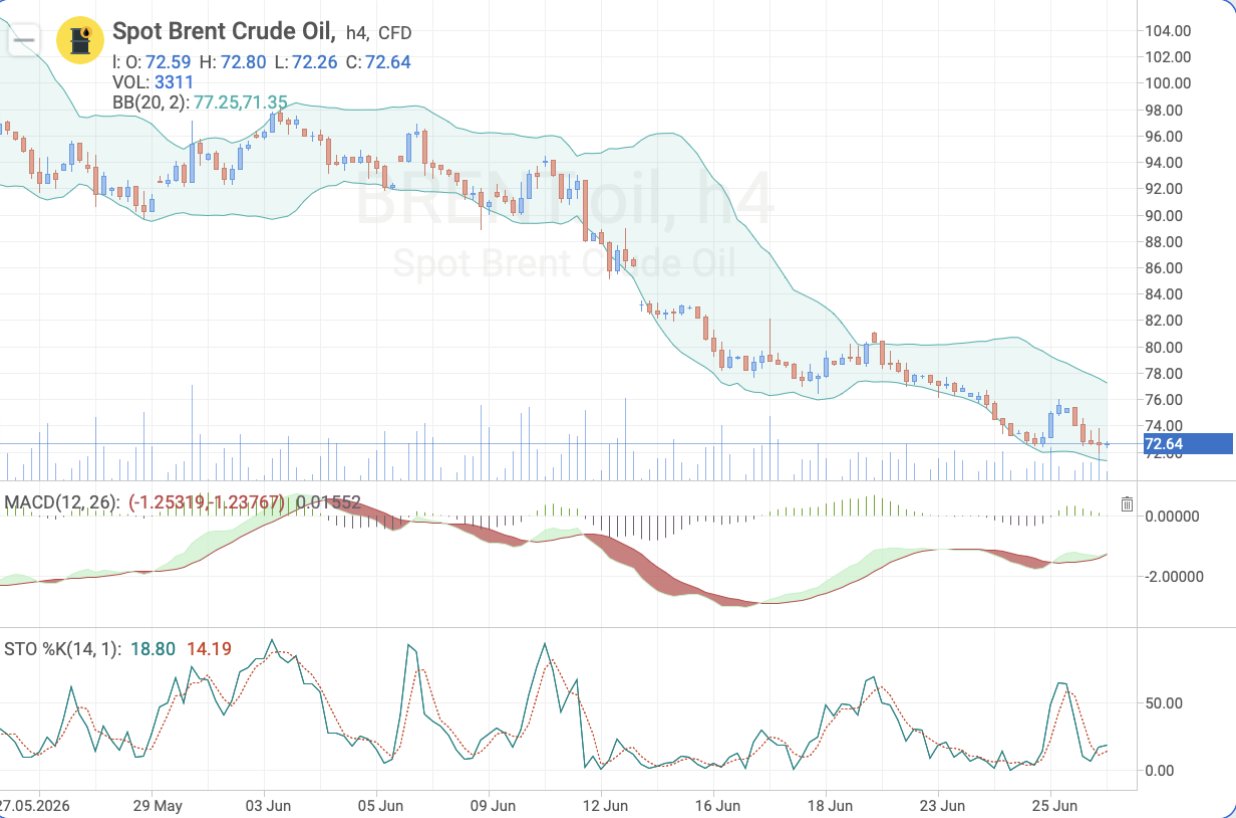

The OPEC+ meeting takes place after the trading week closes, but the alliance's output decision will drive oil market sentiment at Monday's open. Following the Israel-Iran ceasefire, Brent quickly retreated to pre-escalation levels as traders removed most of the geopolitical premium from prices. The focus has now returned to fundamentals: production strategy, demand expectations and whether OPEC+ sticks to its planned output increases. If the alliance confirms additional production growth, downward pressure on oil could continue. A more cautious stance would give Brent room to recover from its recent lows.

Market Reaction

Confirmation of higher output targets would add selling pressure on Brent and WTI and weigh on the Canadian dollar and oil sector equities. A pause or pullback in the production increase plan would bring buyers back into the oil market and support a recovery from recent levels. The Monday open gap risk is elevated given the Sunday timing of the decision.

Market Sentiment

Oil market sentiment is neutral. After the sharp drop in prices, investors believe the majority of the geopolitical premium has already left Brent. Attention is gradually shifting toward the global demand outlook and the actions of major producers. If OPEC+ holds its course on raising output, the market will test recent lows. A more measured signal from the alliance would support a Brent recovery early in July. Brent is trading below its nearest resistance, with MACD still in negative territory even as the selling pressure eases. As long as the contract stays under 75.00 USD per barrel, the 69.50 support area remains the natural downside target.

Source: RoboForex. Past performance is not indicative of future results.

Key Levels — Brent

| Level | Value |

|---|---|

| Resistance | 75.00 / 77.00 USD |

| Support | 71.30 / 69.50 USD |

| Target | 69.50 USD |

Track the forecasts and actual figures for each event — the gap between consensus and actual readings is what determines how sharply prices move. Learn more about how to read the economic calendar and trade the news.

Conclusion

The week runs from a Tuesday JOLTS release through to a Thursday payrolls report, with Eurozone inflation and Australian PMI filling Wednesday. Thursday is the focal day: Non-Farm Payrolls will determine the dollar's direction into the July 4 holiday weekend and set the tone for the first full trading week of July.

The Sunday OPEC+ decision adds an oil market dimension that carries over into Monday. If the alliance confirms higher production, the fading geopolitical premium offers no buffer for prices, and Brent may test its recent lows. A payrolls report that surprises to the downside, combined with a cautious OPEC+ outcome, would give risk assets and commodity currencies a meaningful window to recover ground lost during June.

Any information provided in articles on this website is based solely on the personal opinions of the authors. These articles should not be construed as trading recommendations or a call to action. The authors and RoboForex accept no responsibility for the results of any trades made on the basis of these recommendations and reviews. Past performance is not indicative of future results. Trading stocks and CFDs involves a high risk of capital loss.