Super Micro Computer stock forecast for 2026 – can SMCI return to growth?

Super Micro Computer surprised the market with strong revenue growth and profits exceeding expectations. The company continues to benefit from the AI infrastructure boom, but margins remain under pressure. Therefore, not only sales growth but also the company’s ability to improve profitability will be key.

Super Micro Computer, Inc. (NASDAQ: SMCI) delivered very strong revenue growth in Q2 of the 2026 financial year. Sales rose to 12.68 billion USD, up from 5.69 billion USD a year earlier, representing a 123% year-on-year increase. Net income reached 400.56 million USD, compared with 320.60 million USD last year, and diluted EPS increased to 0.60 USD from 0.51 USD, reflecting profit growth, albeit at a slower pace than revenue expansion.

The results exceeded market expectations. Non-GAAP EPS came in at 0.69 USD, versus a consensus estimate of around 0.49 USD. Revenue of 12.68 billion USD also significantly surpassed the analyst forecast of approximately 10.4 billion USD.

The main driver of the quarter was exceptionally strong demand for AI servers. Additionally, around 1.5 billion USD of shipments were carried over from the previous quarter, partially offsetting weaker Q1 results.

However, a key weakness remained: gross margin fell to 6.3% from 11.8% a year ago, due to tariffs, memory component shortages, and other cost pressures.

Management also provided a strong outlook, forecasting revenue of at least 12.3 billion USD for Q3 and raising full-year revenue guidance to at least 40 billion USD for the 2026 financial year.

This article examines Super Micro Computer, Inc., detailing its revenue sources, analysing the company’s quarterly performance, and outlining expectations for the 2026 financial year. A technical analysis of SMCI shares is also provided, which forms the basis for the Super Micro Computer stock forecast for 2026.

About Super Micro Computer, Inc.

Super Micro Computer was founded in 1993 by Charles Liang. The company designs and manufactures server hardware, including motherboards, servers, data storage solutions, GPU systems, and other computing technologies. Proprietary manufacturing facilities in the Netherlands, the US, and Taiwan allow it to tailor its products to the specific demands of different markets.

Super Micro employs a modular approach to deliver customised solutions for data centres, cloud services, and enterprise clients. The company went public on 29 March 2007, listing on the NASDAQ under the ticker SMCI.

Super Micro Computer, Inc.’s primary revenue streams

Super Micro Computer generates revenue from the following sources:

- Server systems – the largest revenue segment, which includes:

- Rackmount servers – high-performance servers designed for data centres, cloud computing, and AI workloads.

- GPU-optimised systems – servers built for artificial intelligence (AI), machine learning, and deep learning applications.

- Blade and multi-module servers – high-density solutions for enterprises and hyperscale environments.

- Data storage systems – this segment includes all-flash and hybrid storage solutions, as well as software-defined storage (SDS) architectures.

- Embedded and IoT systems – encompasses revenue from industrial and edge computing products, including IoT and edge servers used in smart cities, automation, and real-time data processing. It also includes industrial computing solutions for healthcare, telecommunications, and manufacturing.

- Networking and power technologies – this segment comprises:

- High-performance networking equipment – Ethernet switches, network adapters, and interconnects for data centres.

- Power supply units (PSUs) and cooling systems – modular, energy-efficient, and redundant power supplies, along with air and liquid cooling solutions.

- Components and accessories – revenue from individual hardware components, such as motherboards, chassis, processors, memory, storage devices, and accelerators.

Super Micro’s business model is centred on modular and customisable computing systems catering to enterprises, cloud providers, and the artificial intelligence industry.

Super Micro Computer, Inc. Q2 2025 financial results

On 25 February, amid the threat of delisting, Super Micro Computer released its Q2 2025 financial results for the quarter ended 31 December 2024. Below are the key figures:

- Revenue: 5.68 billion USD (+54%)

- Net profit: 320.59 million USD (+8%)

- Earnings per share: 0.51 USD (no change)

- Gross profit: 670.02 million USD (+18%)

Charles Liang, Chair and CEO of Super Micro, described Q2 FY2025 as relatively strong despite challenges, highlighting a 54% year-on-year revenue increase. This growth was driven by robust demand for AI solutions from both existing and new customers. He acknowledged certain obstacles, including cash flow pressures and market concerns regarding the delayed financial report. Liang identified the transition from Nvidia Hopper to Blackwell GPUs as a key growth factor, with supply expected to increase in the current quarter (Q3 FY 2025).

CFO David Weigand provided further details, noting that gross margin stood at approximately 11.9%, down from 13.1% in Q1 of the 2025 financial year, due to changes in product mix and customer base. He emphasised that AI-related platforms accounted for over 70% of revenue, reinforcing the company’s strong position in the enterprise and cloud provider markets.

For Q3 of the 2025 financial year, ended 31 March 2025, the company projected revenue in the range of 5.00–6.00 billion USD, signalling continued growth, although at a more moderate pace due to competitive dynamics in the AI server market.

Charles Liang has set an ambitious target of 40.00 billion USD in revenue by early FY2026, citing underutilised production capacity in Malaysia, the US, and Taiwan. He underscored Super Micro’s leadership in direct liquid cooling (DLC) technology, forecasting that over 30% of new data centres globally will adopt this technology within 12 months, positioning SMCI as a key player in this transition. Liang also highlighted plans to expand manufacturing operations in Europe, the US, and Taiwan to meet growing demand, particularly for AI infrastructure solutions.

Super Micro Computer, Inc. Q3 2025 financial results

On 6 May, Super Micro Computer released its Q3 2025 financial results for the quarter ended 31 March 2025. Below are the key figures:

- Revenue: 4.60 billion USD (+19%)

- Net profit: 108.77 million USD (–73%)

- Earnings per share: 0.31 USD (–53%)

- Gross profit: 440.21 million USD (–27%)

- Gross margin: 9.6% (–590 bps)

Super Micro recorded revenue of 4.6 billion USD, slightly above the revised forecast but still below Wall Street expectations, which had been buoyed by the AI euphoria earlier this year. Adjusted earnings per share stood at 0.31 USD, also lower than in previous quarters, suggesting that the hypergrowth phase had begun to slow, at least temporarily. Management attributed the shortfall to delays in customer orders and uncertainties in the supply chain.

A major strength remains the long-term driver of widespread adoption of AI infrastructure. Super Micro is at the centre of this trend, producing high-density server systems with liquid cooling that hyperscale clients actively purchase. A recent partnership with DataVolt demonstrates that the company is expanding its presence in the Middle East, where a data centre boom is underway.

Financially, the company appears stable, holding approximately 1.4 billion USD in cash on its balance sheet, although debt remains significant – around 1.9 billion USD – and is increasing. Moreover, much of the revenue growth in recent quarters has come from a very narrow segment: AI servers. Should this market cool (for example, due to saturation or increased competition from Dell, HPE, and NVIDIA), it would put pressure on margins.

The company’s guidance for Q4 2025 anticipates revenue of 5.6–6.4 billion USD and earnings per share in the range of 0.40–0.50 USD. However, the full-year revenue forecast has been lowered to 21.8–22.6 billion USD from the previous estimate of 23.5–25.0 billion USD, citing delayed customer spending and economic uncertainty.

Super Micro Computer, Inc. Q4 2025 financial results

On 5 May, Super Micro Computer, Inc. released its Q4 2025 financial results for the period ended 30 June 2025. Key financial results are as follows:

- Revenue: 5.76 billion USD (+7%)

- Net profit: 195.15 million USD (–34%)

- Earnings per share: 0.41 USD (–24%)

- Gross profit: 544.10 million USD (0%)

- Gross margin: 9.5% (–590 bps)

Super Micro Computer, Inc.’s Q4 2025 results came in below expectations. Revenue reached 5.8 billion USD versus forecasts of around 5.96 billion USD, primarily reflecting changes in contract terms with major clients and delays in the delivery of key components, including Nvidia GPUs. Non-GAAP earnings per share were 0.41 USD, also below market expectations. Non-GAAP gross margin declined to 9.5%, continuing its downward trend amid rising costs, including personnel, taxes, and logistics.

On a positive note, operating cash flow reached 864 million USD, reflecting strong conversion of revenue into cash and indicating resilient operational efficiency. Despite short-term challenges, the company delivered robust international growth: revenue in the Asia-Pacific region increased by 91% YoY, in EMEA by 66%, while the US market recorded a 33% decline.

Management reaffirmed its strategic focus on expanding the hyperscale and AI client base, targeting 6–8 major customers in FY 2026. Guidance for Q1 FY 2026 projects revenue in the range of 6–7 billion USD and non-GAAP EPS of 0.40–0.52 USD. For the full 2026 financial year, the company expects revenue of at least 33 billion USD. However, some analysts consider this forecast overly optimistic, citing intensifying competition, declining margins, and reliance on a limited number of key clients.

Super Micro Computer, Inc. Q1 2026 financial results

On 5 May, Super Micro Computer released its Q1 results for the 2026 financial year (Q4 of the 2025 calendar year), ended 30 June 2025. The key figures are as follows:

- Revenue: 5.02 billion USD (–15%)

- Net income: 239.90 million USD (–50%)

- Earnings per share: 0.35 USD (–52%)

- Gross profit: 474.45 million USD (–39%)

- Gross margin: 9.5% (–360 bps)

Super Micro delivered a weak quarter, missing market expectations: revenue of around 5.0 billion USD and non-GAAP EPS of 0.35 USD came in below analysts’ forecasts of approximately 5.8–6.0 billion USD in revenue and around 0.46 USD in EPS.

On a non-GAAP basis, profitability declined sharply year-on-year: gross margin fell to 9.5% from 13.1% a year earlier, adjusted net income decreased to about 240 million USD, and non-GAAP EPS dropped to 0.35 USD from 0.73 USD. Revenue contracted by roughly 15% year-on-year and around 13% quarter-on-quarter, while operating cash flow was negative at approximately –918 million USD due to higher inventory and receivables. The balance sheet shows 4.2 billion USD in cash and cash equivalents and approximately 4.8 billion USD in debt, indicating that the company moved into a modest net-debt position.

The main reason for the weak quarterly figures was the deferral of deliveries for several large AI projects at clients’ request, as they awaited new systems based on NVIDIA Blackwell and updated configurations. As a result, part of the existing order backlog was not recognised in the reported revenue.

However, management issued an aggressive outlook: for Q2 FY 2026, the company expected revenue of 10–11 billion USD and non-GAAP EPS of 0.46–0.54 USD, implying nearly a twofold increase in quarterly sales. For the full 2026 financial year, Super Micro planned to generate revenue of at least 36 billion USD (compared with the previous guidance of around 33 billion USD), based on a rapidly growing order book, including more than 13 billion USD in systems built on NVIDIA Blackwell Ultra. Management also stated its goal of achieving sequential growth in each quarter of the year.

Super Micro Computer, Inc. Q2 2026 financial results

On 3 February 2026, Super Micro Computer (NASDAQ: SMCI) released its Q2 2026 financial results for the quarter ended 31 December 2025. Key figures compared with the same period last year are as follows:

- Revenue: 12.68 billion USD (+123%)

- Net income: 400.56 million USD (+25%)

- Earnings per share: 0.60 USD (+18%)

- Gross profit: 798.57 million USD (+19%)

- Gross margin: 6.3% (–550 bps)

The quarter was very strong in revenue. Sales reached 12.68 billion USD, net income was 400.56 million USD, diluted EPS rose to 0.60 USD, and gross profit increased to 798.57 million USD. However, the main weakness persisted – gross margin fell to 6.3% from 11.8% a year ago, and non-GAAP gross margin declined to 6.4% from 11.9%.

Compared with market expectations, this was no longer a weak quarter like Q1 2026; the company comfortably exceeded both analyst forecasts and its own internal guidance.

The primary growth driver was the recovery of deferred shipments, along with exceptionally strong demand for AI infrastructure. Management reported that around 1.5 billion USD of revenue came from shipments delayed from Q1, while AI GPU platforms accounted for more than 90% of quarterly revenue. The bulk of sales came from large data centres and the OEM segment, which generated 10.7 billion USD, or 84% of total revenue. This concentration also represents a notable risk, considering that one major client accounted for approximately 63% of quarterly sales, highlighting continued dependence on a few large customers.

Margins remain a concern despite explosive revenue growth. The company is generating far more revenue, but less profit per dollar of sales.

Cash flow quality has improved but remains imperfect. Operating cash flow in Q2 was negative at 24 million USD, compared with –918 million USD in Q1, and free cash flow was around –45 million USD. At the end of the quarter, the company held 4.1 billion USD in cash against 4.9 billion USD in bank debt and convertible bonds, resulting in net debt of approximately 787 million USD. Inventory increased to 10.6 billion USD and accounts receivable to 11.0 billion USD, reflecting an aggressive working capital investment in anticipation of future shipments.

Management’s outlook also appears strong. For Q3 2026, the company expects at least 12.3 billion USD in revenue (+167% YoY), GAAP EPS of no less than 0.52 USD, non-GAAP EPS of no less than 0.60 USD (+94% YoY), and a 30-basis-point improvement in gross margin relative to Q2.

The full-year revenue forecast has been raised to 40 billion USD, up from the previous 36 billion USD, implying an 82% increase from 2025.

In summary, Super Micro delivered a strong quarter in terms of revenue, EPS, and guidance, but certain vulnerabilities remain. The results confirm the huge demand for its AI servers and indicate that Q1 underperformance was largely due to deferred shipments rather than a collapse in demand. At the same time, the business is growing at the expense of very low margins, high working capital consumption, and significant reliance on a few major clients. The key question now is not whether Super Micro is growing, but whether the company can sustain this sales volume while gradually improving margins.

Analysis of key valuation multiples for Super Micro Computer, Inc.

Below are the key valuation multiples for Super Micro Computer, Inc. based on Q2 2026 financial results, calculated using non-GAAP metrics and a share price of 32 USD:

| Multiple | What it indicates | Value | Commentary |

|---|---|---|---|

| P/E (TTM) | Price paid for 1 USD of earnings over the past 12 months | 21.8 | ⬤ For a server manufacturer, the stock is no longer cheap, especially given its unstable margin. |

| P/S (TTM) | Price paid for 1 USD of annual revenue | 0.68 | ⬤ Based on revenue, the stock looks inexpensive, as the market is not assigning a high growth premium. |

| EV/Sales (TTM) | Enterprise value to sales, accounting for debt | 0.71 | ⬤ Even accounting for debt, the business is valued at less than one year of revenue. |

| P/FCF (TTM) | Price paid for 1 USD of free cash flow | 43.2 | ⬤ The FCF valuation is already high, as cash flow has dropped sharply in recent quarters. |

| FCF Yield (TTM) | Free cash flow yield to shareholders | 2.3% | ⬤ FCF yield is low. |

| EV/EBITDA (TTM) | Enterprise value to operating profit before depreciation and amortisation | 18.2 | ⬤ For a hardware business, this is a fairly high level. |

| EV/EBIT (TTM) | Enterprise value to operating profit | 19.2 | ⬤ Valuation based on operating profit is already demanding. |

| P/B | Price to book value | 2.7 | ⬤ Moderate premium to capital. |

| Forward P/E | Forward price-to-earnings (P/E) ratio | 17.2 | ⬤ Below the current P/E, suggesting the market expects profit growth but does not consider it risk-free. |

| Net Debt/EBITDA | Debt burden relative to EBITDA | 0.74 | ⬤ Debt levels are low and manageable. |

| Interest Coverage (TTM) | Ability to cover interest expenses with operating profit | 12 | ⬤ Interest coverage is strong. |

Based on revenue, Super Micro shares appear inexpensive. The P/S and EV/Sales ratios are below 1, which is considered a low valuation for a company with rapidly increasing sales. The balance sheet also looks solid, with low debt, a Net Debt/EBITDA ratio below 1, and earnings sufficient to comfortably cover interest payments.

However, when looking at profitability, particularly cash flow, the picture is less favourable. The P/E is around 22, the EV/EBITDA is about 18, and the EV/EBIT is roughly 19, which can no longer be considered low for a company with unstable margins. The main issue is weak free cash flow. As a result, the P/FCF ratio is high, and the FCF yield is low. This indicates that the market still believes in revenue growth but is uncertain whether it will quickly translate into stable cash flow.

Overall, SMCI shares appear cheap based on revenue, but not in terms of earnings or cash quality. If the company can stabilise its margins and increase free cash flow, the valuation could become significantly more attractive. Conversely, if cash flow remains weak, the low revenue-based valuation alone will not provide strong support for the stock.

Expert forecasts for Super Micro Computer, Inc. stock

- Barchart: 6 out of 19 analysts rated Super Micro Computer shares as Strong Buy, 2 as Moderate Buy, 8 as Hold, 1 as Sell, and 2 as Strong Sell. The upper price target is 64 USD, and the lower bound is 15 USD.

- MarketBeat: 5 out of 15 analysts assigned a Buy rating to the shares, 8 recommended Hold, and 2 recommended Sell. The upper price target is 64 USD, and the lower bound is 27 USD.

- TipRanks: 2 out of 10 analysts rated the shares as Buy, 6 as Hold, and 2 as Sell. The upper price target is 63 USD, and the lower bound is 26 USD.

- Stock Analysis: 4 out of 16 experts rated the shares as Strong Buy, 1 as Buy, 8 as Hold, and 3 as Strong Sell. The upper price target is 70 USD, and the lower bound is 26 USD.

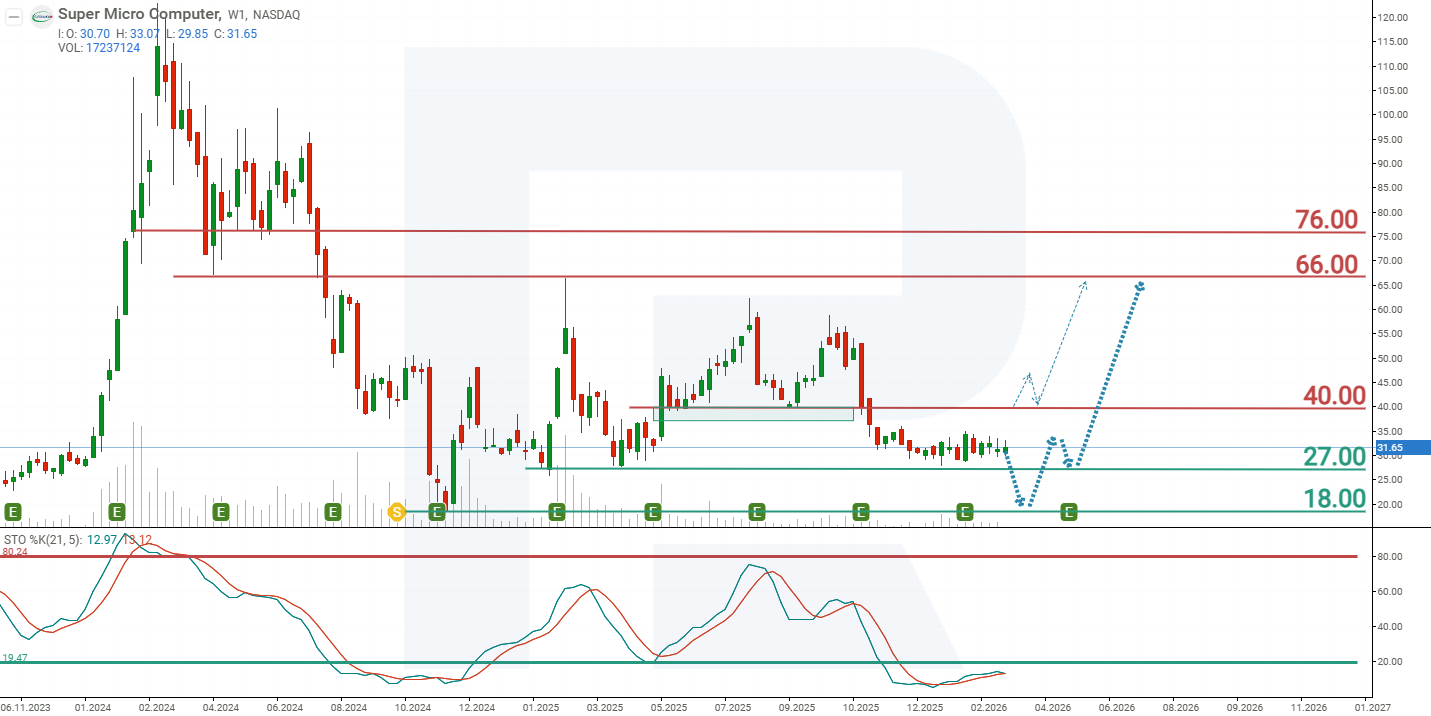

Super Micro Computer, Inc. stock price forecast for 2026

Following an 85% decline from its all-time high, Super Micro Computer shares have yet to establish a stable uptrend. The stock is trading within a wide range of 27-60 USD, occasionally breaking out of this range. Following the release of the quarterly report, there have been no significant changes – the shares remain near support at 27 USD. The Stochastic indicator is in the oversold zone, but its lines are crossing from above, suggesting the potential for another downward wave. Based on the current performance of Super Micro Computer shares, the expected price movements for SMCI in 2026 are as follows:

The primary forecast for Super Micro Computer shares anticipates a break below support at 27 USD, followed by a decline to 18 USD. At this level, investor interest in the stock is expected to rise, potentially driving SMCI shares up to 40 USD. A breakout above this resistance could catalyse further gains towards 66 USD.

An alternative forecast for Super Micro Computer stock assumes a break above the 40 USD resistance level. In this scenario, the stock is expected to rise towards 66 USD.

Risks of investing in Super Micro Computer, Inc. stock

Investing in Super Micro Computer shares involves several factors that could negatively impact the company’s revenue and profits, as well as investor returns:

- Corporate governance and financial reporting risks. In its 2025 annual report, the company acknowledged that the process of addressing significant internal control deficiencies was not yet complete. Auditor BDO explicitly noted that, as of 30 June 2025, Supermicro did not maintain effective internal control over financial reporting. The identified weaknesses were related to deficiencies in IT controls, segregation of duties, completeness and accuracy of data, and timely disclosure of certain related-party transactions. For the market, this is a sensitive issue, as such deficiencies increase the risk of reporting errors, restatements, and a loss of investor confidence.

- High customer concentration. The company already has significant revenue concentration: in FY2025, four customers each accounted for 10% or more of sales, and in Q2 2026, a single large data centre client contributed approximately 63% of total revenue. This means that a delay, cancellation, or renegotiation of even one major contract could have a significant impact on revenue and profitability.

- Dependence on a limited number of suppliers and component shortages. Supermicro notes that it relies on a restricted pool of suppliers for certain components, and the prices and availability of critical materials remain volatile. Supply disruptions, shortages of GPUs, memory, SSDs, or other components could result in delivery delays, higher costs, and weaker financial performance.

- Weak cash flow and growing financing needs. As of December 2025, the company held around 4.1 billion USD in cash, while total bank debt and convertible bonds amounted to 4.9 billion USD. In the first six months of FY2026, operating cash flow was negative, totalling –941 million USD, primarily due to increases in accounts receivable and inventory. Consequently, even amid business growth, the company may require additional capital, which could lead to shareholder dilution or further increases in leverage.

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex bears no responsibility for trading results based on trading recommendations described in these analytical reviews.