Broadcom strengthens its position in AI and maintains upside potential for the stock

Broadcom delivered a strong Q1 2026 performance, confirming robust demand for AI chips and sustained revenue growth. The company exceeded market expectations and issued solid guidance. If support at 320 USD holds, this could act as a catalyst for a renewed advance in the share price.

Broadcom Inc. (NASDAQ: AVGO) delivered very strong results for Q1 of the 2026 financial year. Revenue reached 19.31 billion USD (+29% year-on-year), while non-GAAP EPS increased to 2.05 USD (+28% year-on-year). The figures came in slightly above analyst expectations, confirming sustained demand for the company’s AI infrastructure solutions.

The primary growth driver once again was the semiconductor business. Revenue from the Semiconductor Solutions segment rose to 12.52 billion USD (+52% year-on-year), with AI chip sales expanding particularly rapidly. Revenue from AI semiconductors increased to 8.4 billion USD (+106% year-on-year), supported by strong demand from major cloud providers.

The infrastructure software segment showed more modest momentum. Revenue from Infrastructure Software grew by just 1% to 6.80 billion USD, indicating that Broadcom’s current growth is largely driven by its semiconductor operations and demand for AI chips.

At the same time, the company continues to deliver exceptionally high profitability. Adjusted EBITDA reached 13.13 billion USD, representing 68% of total revenue.

Guidance for the next quarter also appears strong. Broadcom expects revenue of 22 billion USD and anticipates AI semiconductor revenue rising to 10.7 billion USD.

This article examines Broadcom Inc., outlining its revenue structure, reviewing its quarterly performance, and presenting expectations for 2026. It also includes a technical analysis of AVGO shares, which forms the basis for the Broadcom stock forecast for 2026.

About Broadcom Inc.

Broadcom Inc. is a US-based technology company specialising in developing chips for networking equipment, servers, data centres, wireless communications, and software for cloud and enterprise solutions. Founded in 1961 as a division of HP, it was spun off as Avago Technologies in 1991. In 2009, Avago Technologies went public on NASDAQ, and its shares have been traded under the ticker AVGO ever since. In 2016, Avago Technologies acquired Broadcom Corporation for 37.0 billion USD and adopted its name.

Broadcom Inc.’s main revenue streams

Broadcom’s revenue is divided into two main segments:

- Semiconductor business: approximately 75% of revenue is derived from the sale of chips for data centres, cloud computing, AI accelerators, network processors, and chips for servers, storage, networking equipment, and wireless modules for smartphones and Wi-Fi.

- Infrastructure software: the remaining 25% of revenue comes from enterprise software for cloud computing, cybersecurity and networking solutions, VMware products, automation components, and DevOps platforms.

Broadcom Inc. Q1 2025 financial results

On 6 March, Broadcom released its Q1 2025 financial results for the quarter ended 2 February 2025. The key figures are as follows:

- Revenue: 14.9 billion USD (+25%)

- Net profit: 7.8 billion USD (+67%)

- Earnings per share (EPS): 1.60 USD (+307%)

- Operating profit (non-GAAP): 9.82 billion USD (+44%)

Net revenue by segment:

- Semiconductor solutions: 8.2 billion USD (+55%)

- Infrastructure software: 6.7 billion USD (+47%)

Broadcom reported strong financial results for Q1 of the 2025 financial year, with revenue rising by 25% year-on-year. This growth was primarily driven by a 77% increase in AI-related revenue, which reached 4.1 billion USD, and a 47% rise in infrastructure software revenue, totalling 6.7 billion USD. The successful integration of VMware, acquired in 2023, also played a significant role in this expansion, strengthening Broadcom’s position in the enterprise software market.

CEO Hock Tan highlighted the strong demand for custom AI chips from cloud computing giants, which heavily invest in AI-driven data centres.

Looking ahead to Q2 2025, Broadcom expects revenue to reach 14.9 billion USD, slightly above analysts’ estimates. The company anticipates further growth in the AI semiconductor segment, with AI-related revenue projected to increase to 4.4 billion USD in the next quarter.

Broadcom Inc. Q2 2025 financial results

On 5 June, Broadcom published its Q2 2025 financial results for the quarter ended 4 May 2025. Below are its key figures:

- Revenue: 15.0 billion USD (+20%)

- Net income: 7.8 billion USD (+44%)

- Earnings per share (EPS): 1.58 USD (+43%)

- Operating profit (non-GAAP): 9.79 billion USD (+37%)

Net revenue by segment:

- Semiconductor solutions: 8.4 billion USD (+17%)

- Infrastructure software: 6.6 billion USD (+25%)

Broadcom’s Q2 report for the 2025 financial year painted a strong picture for investors, highlighting the company’s solid position in the AI and semiconductor sectors. Revenue rose by 20% from last year, largely driven by a rapid 46% increase in AI revenue to 4.4 billion USD. This growth reinforced Broadcom’s pivotal role as a supplier of custom AI chips and networking solutions to major companies, such as Google, Meta, and ByteDance.

In Q2 of the 2025 financial year, the company repurchased shares worth 3.2 billion USD. This demonstrated management’s confidence in the long-term value of the business and its ability to generate stable cash flow.

Broadcom issued an optimistic outlook for Q3, anticipating revenue of 15.8 billion USD, slightly above Wall Street’s expectations. CEO Hock Tan emphasised that AI semiconductor revenue would increase to 5.1 billion USD next quarter, marking the tenth consecutive quarter of growth. This guidance reflected the company’s confidence in sustained demand for its AI and networking products, including the recently unveiled Tomahawk 6 switch, which enhances network performance and efficiency for AI workloads.

Despite strong financial results and a positive outlook, Broadcom’s shares fell by 5% following the release of the report. Market participants were concerned about a potential slowdown in the AI market, which could lead the company to miss its targets. In addition, Broadcom’s stock price had surged by 92% in the last two months, highlighting a high valuation that may be difficult to sustain amid trade restrictions. Nevertheless, analysts remained optimistic about the company’s future. For instance, Japanese investment banking and securities firm Mizuho Securities named Broadcom one of the best semiconductor stocks, citing its high profitability and strong free cash flow, supported by AI trends.

Overall, Broadcom’s Q2 2025 results confirmed its strategic leadership in the AI and semiconductor sector, with continued investment in AI technology, robust relationships with key clients, and a positive outlook, making the company’s shares an attractive investment.

Broadcom Inc. Q3 2025 financial results

On 4 September, Broadcom released its Q3 2025 financial results for the quarter ended 3 August 2025. The key figures are as follows:

- Revenue: 15.95 billion USD (+22% year-on-year)

- Net income: 8.40 billion USD (+37% year-on-year)

- Earnings per share (EPS): 1.69 USD (+36% year-on-year)

- Operating profit (non-GAAP): 10.45 billion USD (+31% year-on-year)

Net revenue by segment:

- Semiconductor solutions: 9.17 billion USD (+26% year-on-year)

- Infrastructure software: 6.79 billion USD (+17% year-on-year)

Broadcom’s Q3 2025 financial results exceeded analyst expectations and confirmed the company’s resilience amid intense competition and a rapidly growing AI sector. Revenue reached 15.95 billion USD, up 22% compared with the same period last year. The primary growth driver was AI-related solutions, where revenue grew 63% year-on-year to 5.2 billion USD.

The revenue mix was still split between two key areas: semiconductors and infrastructure software. The semiconductor business accounted for more than 75% of total revenue, with the emphasis in the quarter under review placed on orders for hyperscale data centres. Broadcom reported that its backlog of contracted orders reached 110 billion USD, with around half attributable to the AI segment. In the software segment (including VMware), steady growth was observed, supported by the transition to a subscription model and a focus on cloud-based solutions.

The company’s financial performance remained strong. Non-GAAP operating profit totalled approximately 10.7 billion USD, with an EBITDA margin of 67%. Adjusted earnings per share reached 1.69 USD (+36% year-on-year), exceeding the consensus forecast. Gross margin declined slightly due to the higher share of deliveries in the AI segment; however, this was offset by strong operating efficiency.

Management provided a positive outlook for Q4 of the 2025 financial year. Revenue was expected at 17.4 billion USD, up 24% from a year earlier and above analyst expectations. In the AI segment, Broadcom expected to generate 6.2 billion USD, which implied growth of 66% compared with the same quarter in 2024. The company also confirmed that it had secured a contract with a new hyperscale customer worth more than 10 billion USD for the supply of server solutions with AI accelerators (XPU), to be delivered over the coming years.

Broadcom Inc. Q4 2025 financial results

On 11 December, Broadcom released its Q4 2025 financial results for the quarter ended 2 November 2025. The key figures are as follows:

- Revenue: 18.02 billion USD (+28%)

- Net income (non-GAAP): 9.71 billion USD (+39%)

- Earnings per share (non-GAAP): 1.95 USD (+37%)

- Operating income (non-GAAP): 12.22 billion USD (+34%)

Net revenue by segment:

- Semiconductor solutions: 11.07 billion USD (+35%)

- Infrastructure software: 6.94 billion USD (+19%)

Broadcom’s results for Q4 of the 2025 financial year were strong and exceeded market expectations. Revenue amounted to 18 billion USD (+28% y/y), compared with a forecast of 17.5 billion USD, while adjusted earnings per share (non-GAAP EPS) reached 1.95 USD, above analysts’ expectations (1.87 USD). The main growth driver was AI chips: revenue from the semiconductor segment increased to 11.1 billion USD (+35% y/y), of which 6.5 billion USD came from AI-related products (+74% y/y). The infrastructure software business, including VMware, also grew to 6.90 billion USD (+19% y/y). As a result, Broadcom consistently generates earnings from both hardware solutions and software infrastructure. The company maintained high profitability, with non-GAAP EBITDA of 12.2 billion USD (68% of revenue), free cash flow of 7.5 billion USD, and a 10% dividend increase to 0.65 USD per share.

The outlook for Q1 2026 was also positive, with expected revenue at 19.1 billion USD (+28% y/y), the EBITDA margin projected at 67%, and sales of AI chips expected to rise to 8.2 billion USD. Broadcom stated that it had an order backlog for AI solutions of 73 billion USD over the next 18 months.

Broadcom Inc. Q1 2026 financial results

On 4 March, Broadcom released its Q1 2026 financial results for the quarter ended 1 February 2026. The key figures are as follows:

- Revenue: 19.31 billion USD (+29%)

- Net income (non-GAAP): 10.19 billion USD (+30%)

- Earnings per share (non-GAAP): 2.05 USD (+28%)

- Operating income (non-GAAP): 12.83 billion USD (+30%)

Net revenue by segment:

- Semiconductor Solutions: 12.52 billion USD (+52%)

- Infrastructure Software: 6.80 billion USD (+1%)

Broadcom’s Q1 2026 results were strong and slightly exceeded market expectations. Revenue reached 19.31 billion USD, up 29% year-on-year, compared with analyst forecasts of 19.18 billion USD. Adjusted EPS came in at 2.05 USD, slightly above the consensus estimate of around 2.03 USD.

The main driver of growth was the AI-related business. Revenue from AI chips rose to 8.4 billion USD, representing a 106% year-on-year increase. Strong demand was seen for AI accelerators and networking equipment for data centres. The company’s overall semiconductor business expanded to 12.52 billion USD, marking 52% year-on-year growth. By contrast, the infrastructure software segment was broadly flat at 6.80 billion USD, increasing by just 1%.

Broadcom continues to maintain exceptionally high profitability. Adjusted EBITDA reached 13.13 billion USD, equivalent to approximately 68% of revenue. Free cash flow totalled 8.01 billion USD, or around 41% of revenue. The company also announced a new 10 billion USD share buyback program and maintained its quarterly dividend at 0.65 USD per share.

Guidance for Q2 2026 was also positive. Broadcom expects revenue of around 22.0 billion USD (+47% year-on-year), significantly above the LSEG consensus of approximately 20.56 billion USD. The company also forecasts an adjusted EBITDA margin of 68%, while revenue from AI chips is expected to rise to 10.7 billion USD. Broadcom additionally stated that it now sees the potential to exceed 100 billion USD in AI chip revenue by 2027, signalling very strong management confidence in sustained demand from major hyperscale clients.

Analysis of key valuation multiples for Broadcom Inc.

Below are the key valuation multiples for Broadcom Inc. based on Q1 2026 financial results, calculated using a share price of 342 USD.

| Multiple | What it indicates | Value | Comment |

|---|---|---|---|

| P/E (TTM) | Price paid for 1 USD of earnings over the past 12 months | 169 | ⬤ An extremely high valuation even for a leading chipmaker. |

| P/S (TTM) | Price paid for 1 USD of annual revenue | 25 | ⬤ Extremely expensive, with the price reflecting a substantial advance premium for long-term growth in the AI business. |

| EV/Sales (TTM) | Enterprise value to sales, accounting for debt | 26 | ⬤ A very aggressive valuation. |

| P/FCF (TTM) | Price paid for 1 USD of free cash flow | 60 | ⬤ Based on current cash flow, Broadcom appears highly expensive. |

| FCF Yield (TTM) | Free cash flow yield to shareholders | 1.7% | ⬤ Free cash flow yield stands at 1.7% – a low level, implying that the market is betting on significant further growth in FCF. |

| EV/EBITDA (TTM) | Enterprise value to operating profit before depreciation and amortisation | 38 | ⬤ A very high valuation even for a leader in AI chips. |

| EV/EBIT (TTM) | Enterprise value to operating profit | 50 | ⬤ Elevated valuation with virtually no margin of safety if growth were to slow. |

| P/B | Price to book value | 21 | ⬤ The market is paying 21 USD for every 1 USD of book equity, reflecting very high expectations and a substantial share of intangible assets. |

| Forward P/E | Forward price-to-earnings (P/E) ratio | ||

| Net Debt/EBITDA | Debt burden relative to EBITDA | 1.1 | ⬤ Debt levels remain moderate. |

| Interest Coverage (TTM) | Ability to cover interest expenses with operating profit | 11 | ⬤ Interest expenses are well covered by operating profit. |

Broadcom appears to be a strong company in terms of business quality and cash generation. Revenue is growing rapidly, adjusted EBITDA and free cash flow remain at high levels, and the debt burden is moderate, placing no material pressure on the balance sheet. However, by valuation metrics, the stock remains very expensive. A P/E of around 65x, P/S and EV/Sales above 20x, P/FCF above 50x, and EV/EBITDA above 36x indicate that the market has already priced in strong AI revenue growth, high margins, and continued earnings expansion. At the same time, a forward P/E of around 31.6 suggests that even after accounting for expected profit growth, Broadcom still trades at a notable premium.

Overall, the current share price appears justified only if the company maintains very high revenue and earnings growth for several more years, supported by sustained demand for AI chips and infrastructure software. If growth begins to normalise more quickly than the market expects, even the current valuation could prove excessive.

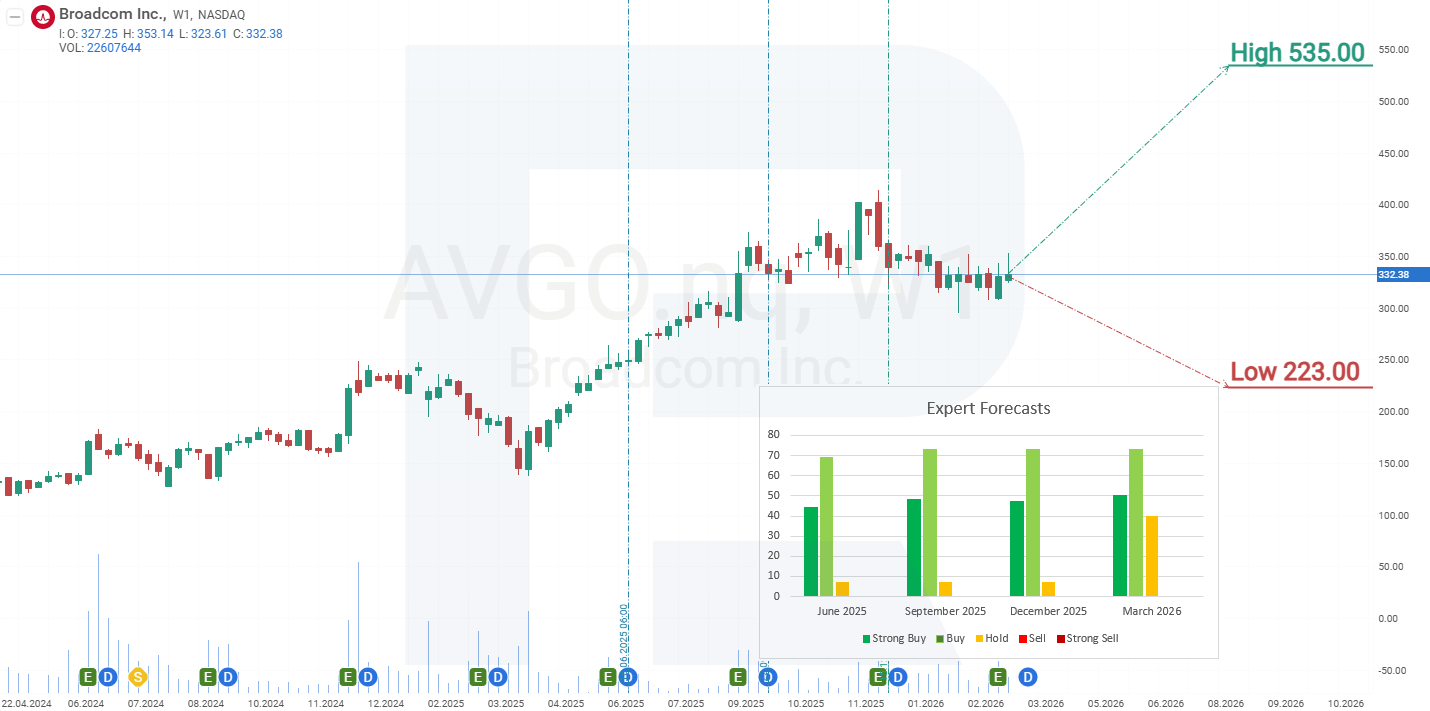

Expert forecasts for Broadcom Inc. stock

- Barchart: 36 out of 42 analysts rated Broadcom shares as a Strong Buy, 3 as Buy, and 3 as Hold. The upper price target is 630 USD, and the lower bound is 360 USD.

- MarketBeat: 30 out of 33 analysts assigned a Buy rating to the shares, and 3 recommended Hold. The upper price target is 545 USD, and the lower bound is 300 USD.

- TipRanks: 27 out of 29 analysts rated the shares as Buy, and 2 as Hold. The upper price target is 630 USD, and the lower bound is 360 USD.

- Stock Analysis: 14 of 29 experts rated the shares as a Strong Buy, 13 as a Buy, and 2 as a Hold. The upper price target is 582 USD, and the lower bound is 223 USD.

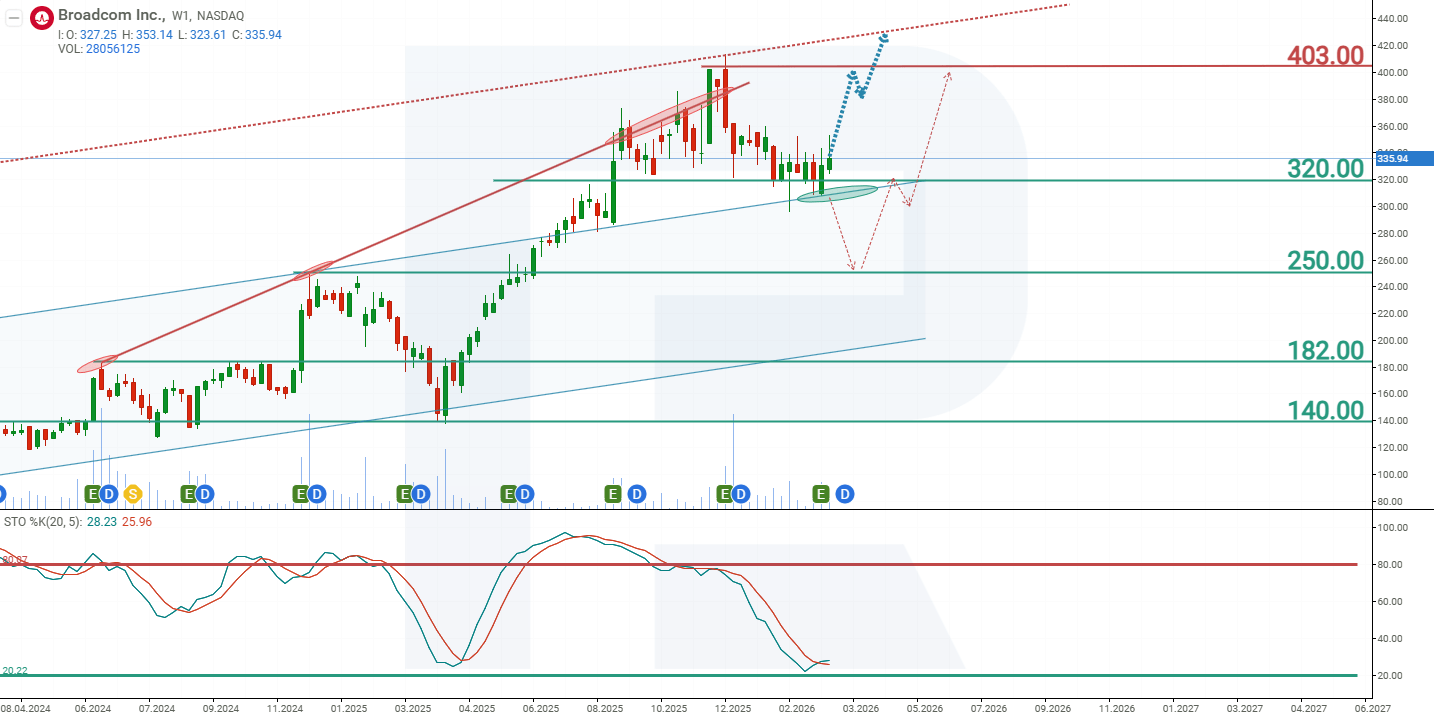

Broadcom Inc. stock price forecast for 2026

In July 2025, Broadcom shares broke above the upper boundary of an ascending channel. They continued to advance by the width of the channel, which represented the technical target for the move. As a result, a record high was set at 415 USD. However, valuations above 400 USD already implied a noticeable premium to fair value, prompting some investors to take profits following the Q3 2025 earnings release, which led to a 20% decline in the share price. The move towards 415 USD was accompanied by pullbacks and rising volatility, signalling buyer fatigue and a willingness among short-term traders to exit positions.

As of March 2026, the shares are trading near support at 320 USD. The Stochastic indicator is approaching the oversold zone, suggesting that the correction may be nearing completion. Notably, in April 2025, when the strong upward move began, the Stochastic indicator was at a similar level to its current reading, which may signal that the present correction is nearing its end. Based on the prevailing price dynamics in Broadcom shares, the potential price scenarios for AVGO in 2026 are as follows:

The primary forecast for Broadcom Inc. shares anticipates further upside towards resistance at 403 USD. If this level is breached, the share price could rise to 430 USD.

The alternative forecast for Broadcom Inc. stock assumes a break below support at 320 USD. In that case, the share price could decline to 250 USD, from which a resumption of the broader uptrend would be expected. Given that a significant proportion of Broadcom shares is held by institutional investors, including index funds, broader capital outflows from these funds could weigh on AVGO’s share price regardless of the company’s financial performance. However, if the company’s financial position remains stable, such a decline could be viewed as a potential buying opportunity.

Risks of investing in Broadcom Inc. stock

When investing in Broadcom’s stock, it is essential to consider the risks the company may face. Below are the key events that could negatively impact Broadcom’s revenue:

- A slowdown in artificial intelligence spending: as AI is a key growth driver, any reduction in spending due to market saturation, an economic downturn, or shifting priorities could directly affect semiconductor revenue. Although investor expectations for AI-related growth are high, slower-than-expected progress could undermine investor confidence and earnings forecasts.

- Dependence on key clients: CEO Hock Tan has mentioned three major cloud clients developing their own AI chips. If these companies succeed, their reduced reliance on Broadcom could harm the profitability of its semiconductor segment.

- Geopolitical and trade risks: Broadcom is exposed to risks from escalating trade tensions between the US and China. Potential tariffs under the Trump administration or export restrictions on AI chips to China could disrupt supply chains or limit access to traditional markets.

- Competition in the semiconductor sector: Broadcom faces competitive pressures from companies like AMD and NVIDIA in the AI and networking solutions space. NVIDIA’s dominance in AI GPUs and the potential revival of Intel (with Broadcom reportedly interested in its chip business) could reduce Broadcom’s market share.

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex bears no responsibility for trading results based on trading recommendations described in these analytical reviews.