JPMorgan shares may test support before resuming their advance

JPMorgan reported a strong quarter, maintained a robust balance sheet, and continued its share buyback program, although part of its profit was driven by one-off items. The base-case scenario for JPM shares envisages a correction towards 313 USD, followed by an advance towards 370 USD.

JPMorgan Chase & Co. (NYSE: JPM) reported stronger-than-expected results for the second quarter of 2026, surpassing both market expectations and the previous quarter's performance. Revenue increased by 27%, net profit rose by 41%, and earnings per share grew by 47%. However, part of the improvement was driven by one-off gains from transactions involving Visa shares and certain equity investments.

The Commercial & Investment Bank made the largest contribution to the group's performance, with revenue increasing by 27% and net profit rising by 46%. Credit quality remained stable. The CET1 ratio stood at a robust 14.1%, and the bank continued to return capital to shareholders through dividends and share buybacks.

The outlook for 2026 became more optimistic for net interest income but more cautious regarding expenses. This suggests that JPMorgan expects business activity to remain strong, although higher costs are likely to continue weighing on efficiency.

This article examines JPMorgan Chase & Co., provides a fundamental analysis of JPM shares, and reviews the bank's quarterly financial results, enabling a comparison of its performance across different reporting periods. It also presents a technical analysis of JPM based on the prevailing price action and offers a forecast for JPMorgan Chase & Co. shares for 2026.

About JPMorgan Chase & Co.

JPMorgan Chase & Co. traces its origins to the Bank of the Manhattan Company, founded in 1799. The modern conglomerate was shaped by a long history of consolidation, culminating in the 2000 merger between Chase Manhattan Corporation and J.P. Morgan & Co. The company did not undergo an IPO, having been formed through successive mergers and acquisitions. Nevertheless, JPMorgan Chase shares are listed on the New York Stock Exchange under the ticker symbol JPM.

JPMorgan Chase provides a broad range of financial services, including investment and commercial banking, retail banking services, asset and wealth management, and risk and payment management solutions. It is the largest US bank by assets and one of the leading investment, commercial, and retail banking institutions. Globally, the company holds a prominent position in investment and financial services and is classified as a systemically important financial institution.

JPMorgan Chase & Co.’s main revenue streams

JPMorgan Chase & Co.’s revenue comes from several key sources:

- Consumer & Community Banking: the largest revenue segment, comprising income from retail banking, including interest on loans and deposits, credit card fees, ATM charges, and other banking services for individuals and small businesses.

- Corporate & Investment Bank: revenue generated from investment banking services, such as commissions on stock and bond offerings, advisory fees for mergers and acquisitions, and income from capital markets trading activities, including fixed income and equities.

- Commercial Banking: income from services provided to medium and large businesses, including loans, cash flow management, and other commercial banking services.

- Asset & Wealth Management: revenue from managing investments for institutional and individual clients, including asset management fees, withdrawals from deposit accounts, and other investment-related income.

- Net Interest Income: profit derived from the difference between interest earned on loans and investments and interest paid on deposits.

JPMorgan Chase’s revenue is highly diversified across a wide range of financial services, from retail to investment banking. This diversification enables the bank to maintain a stable revenue stream even amid changing market conditions.

JPMorgan Chase & Co. Q3 2024 financial results

Banks are traditionally the first to report earnings at the end of each quarter. JPMorgan Chase & Co.’s Q3 2024 results are outlined below, compared with the corresponding period in 2023:

Revenue: 43.3 billion USD (+6%)

Net Income: 12.9 billion USD (–2%)

Earnings per Share (EPS): 4.37 USD (+1%)

Net Interest Income: 23.5 billion USD (+3%)

Consumer & Community Banking revenue: 17.8 billion USD (–3%)

Commercial & Investment Bank revenue: 17.0 billion USD (+8%)

Asset & Wealth Management revenue: 5.4 billion USD (+9%)

Corporate Revenue: 3.1 billion USD (+97%)

Assets under Management: 3.9 trillion USD (+23%)

Client Assets: 5.7 trillion USD (+23%)

In its commentary on the results, JPMorgan Chase’s management emphasised that the bank continues to deliver stable performance despite a challenging economic environment. Q3 2024 revenue exceeded expectations, although net income declined slightly due to higher provisions for credit losses. CFO Jeremy Barnum noted that consumers remain in a strong financial position and that the increase in provisions was driven by growth in the loan portfolio rather than any deterioration in credit quality.

The bank anticipated a gradual decline in net interest income (NII) during Q4 2024, potentially reaching a trough in mid-2025, followed by a recovery supported by loan portfolio expansion and higher credit card turnover. The bank identified the deteriorating geopolitical landscape, the sizable US budget deficit, and changes to existing trade agreements as potential risks.

JPMorgan Chase & Co. Q4 2024 financial results

JPMorgan Chase & Co. released its Q4 2024 results on 15 January 2025. As forecast by the bank’s management, quarterly net interest income declined by 2%. Key highlights of the report are outlined below in comparison with the corresponding period in 2023:

Revenue: 42.8 billion USD (+11%)

Net Income: 14.0 billion USD (+50%)

Earnings Per Share (EPS): 4.81 USD (+58%)

Net Interest Income: 23.0 billion USD (–2%)

Consumer & Community Banking revenue: 18.4 billion USD (–6%)

Commercial & Investment Bank revenue: 17.6 billion USD (+18%)

Asset & Wealth Management revenue: 5.8 billion USD (+13%)

Corporate Revenue: 2.0 billion USD (+13%)

Assets under Management: 4.0 trillion USD (+18%)

Client Assets: 5.9 trillion USD (+18%)

The bank’s Chair and CEO, Jamie Dimon, noted that all business segments performed strongly. The Corporate and Investment Bank (CIB) saw strong client activity. There was also a double-digit increase in payment fees for four consecutive quarters, contributing to a record annual payment income. Retail banking continued to attract new clients across all areas, from consumer banking to asset management, resulting in nearly two million new accounts opening in 2024.

Dimon noted that the bank maintains a resilient balance sheet, including a loss-absorbing capacity of 547 billion USD and 1.4 trillion USD in cash and marketable securities. He assessed the US economy as steady, with a low unemployment rate and stable consumer spending. However, he highlighted two main risks: the potentially inflationary effects of future expenditure and geopolitical instability.

JPMorgan Chase & Co. projected net interest income (excluding markets) of approximately 90 billion USD in 2025, a decrease of 2 billion USD compared to 2024.

The bank anticipated expenses of approximately 95.0 billion USD, representing an increase of 3.9 billion USD compared with 2024. The rise in costs was attributed by management to inflation.

JPMorgan Chase & Co. Q1 2025 financial results

JPMorgan Chase & Co. released its Q1 2025 results on 11 April 2025. The key highlights are provided below in comparison with the corresponding period in 2024:

Revenue: 45.3 billion USD (+8%)

Net Income: 14.6 billion USD (+9%)

Earnings per Share (EPS): 5.07 USD (+58%)

Net Interest Income: 23.4 billion USD (+1%)

Consumer & Community Banking Revenue: 18.3 billion USD (+4%)

Commercial & Investment Bank Revenue: 19.7 billion USD (+12%)

Asset & Wealth Management Revenue: 5.7 billion USD (+12%)

Corporate Revenue: 2.3 billion USD (+5%)

Assets under Management: 4.1 trillion USD (+15%)

Client Assets: 6.0 trillion USD (+15%)

JPMorgan Chase & Co. delivered strong results for Q1 of the 2025 financial year, exceeding Wall Street expectations. The primary growth drivers were the Investment Banking division and trading operations, with Investment Banking fees increasing by 12% and trading revenue rising by 21%, including a record 3.8 billion USD in the equity markets segment.

However, Jamie Dimon warned of significant turbulence on the horizon, mentioning geopolitical tensions, persistent inflation, the elevated budget deficit, and the threat of global trade wars. The bank also increased provisions for potential credit losses to 3.3 billion USD, indicating a rising risk of non-payment from consumers.

The increase in credit loss reserves is a signal of a dual nature. On the one hand, JPMorgan is demonstrating excellent financial results and resilience in its key businesses. On the other hand, growing macroeconomic risks could exert pressure on future profits.

Since the start of the year, JPMorgan’s share price has fallen by more than 5%, despite a strong quarterly report, indicating market caution. However, there were several advantages to long-term investment.

Firstly, JPMorgan remains a systemically important bank with a global network, resilient cash flow, and a diversified business model. It is one of the few banks capable of generating profits in any phase of the economic cycle – whether expansion, stagnation, or recession.

Secondly, JPMorgan’s dividend yield remains consistently high – as of April 2025, it stands at around 2.5-3% per annum. The company follows a policy of regular dividend increases, making the shares attractive to income-focused investors.

Thirdly, the bank is actively repurchasing its own shares. In Q1 2025, JPMorgan Chase & Co. pursued an active capital return policy, executing a buyback program worth 7.1 billion USD. This reflects confidence in its prospects and provides effective support for the share price. Buybacks not only return capital to shareholders but also reduce the number of shares in circulation, thereby increasing earnings per share over time.

JPMorgan Chase & Co. Q2 2025 financial results

JPMorgan Chase & Co. released its financial results for Q2 2025 on 15 July 2025. Below are the key figures compared with the same period in 2024:

Revenue: 45.7 billion USD (–10%)

Net Income: 15.0 billion USD (–17%)

Earnings Per Share (EPS): 5.24 USD (–14%)

Net Interest Income: 23.3 billion USD (+2%)

Consumer & Community Banking Revenue: 18.8 billion USD (+6%)

Commercial & Investment Bank Revenue: 19.5 billion USD (+9%)

Asset & Wealth Management Revenue: 5.8 billion USD (+10%)

Corporate Revenue: 1.5 billion USD (–85%)

Assets Under Management: 4.3 trillion USD (+18%)

Client Assets: 6.4 trillion USD (+19%)

Despite declines in both revenue and net income, JPMorgan Chase & Co.’s results for Q2 2025 exceeded analyst expectations. The bank reported net income of 15 billion USD and EPS of 5.24 USD, compared with market expectations of around 4.96 USD, and revenue came in at 45.7 billion USD, slightly above consensus.

Two business segments stood out: the Commercial and Investment Banking division recorded a 9% increase in revenue, with net income reaching 6.7 billion USD, supported by a 15% rise in trading income and a 7% increase in investment banking fees. This performance was particularly notable amid heightened market volatility. Asset and Wealth Management also continued to perform strongly, with assets under management rising 18% to 4.3 trillion USD and fee income growing at a double-digit pace, underscoring the strength of the bank’s diversified revenue base beyond interest income.

In terms of shareholder returns, management announced a dividend increase to 1.40 USD per share following Q2 results, with a further rise to 1.50 USD per share implemented in Q3 2025. The bank also repurchased shares worth approximately 7 billion USD and reaffirmed its intention to pursue selective M&A opportunities and organic growth, while maintaining a disciplined capital allocation approach.

One of the key positive signals was the upward revision to full-year net interest income (NII) guidance. CFO Jeremy Barnum raised the forecast to 95.5 billion USD from 94.5 billion USD, citing steady loan growth across mortgages, auto lending, and credit cards. Credit card charge-offs were expected to remain around 3.6%, suggesting a controlled risk profile and supporting the outlook for interest income. The increase in the dividend to 1.50 USD in Q3 further reflects management’s confidence in the stability of cash flows.

The decline in reported revenue and profit was largely attributable to the high base effect. In Q2 2024, JP Morgan recorded a significant one-off gain related to its acquisition of First Republic. Additionally, net interest margins began to normalise as deposit costs increased and loan growth moderated.

The sharp decline in the corporate segment revenue reflects the absence of such one-off gains in Q2 2025. In 2024, the bank reported a bargain purchase gain of over 8 billion USD, meaning current results represent a more normalised earnings level for this division.

Nevertheless, management remained cautious. CEO Jamie Dimon once again highlighted several risks, including tariff-related tensions, fiscal deficits, geopolitical uncertainty, and signs of overheating in certain asset classes. Non-performing assets also remained elevated at around 11.4 billion USD, particularly within credit card and corporate lending segments.

JPMorgan Chase & Co. Q3 2025 financial results

On 14 October 2025, JPMorgan Chase & Co. released its Q3 2025 financial results. The key figures compared with the same period in 2024 are as follows:

Revenue: 47.1 billion USD (+9%)

Net Income: 14.4 billion USD (+12%)

Earnings Per Share (EPS): 5.07 USD (+16%)

Net Interest Income: 24.1 billion USD (+2%)

Consumer & Community Banking Revenue: 19.5 billion USD (+9%)

Commercial & Investment Bank Revenue: 19.9 billion USD (+17%)

Asset & Wealth Management Revenue: 6.1 billion USD (+12%)

Corporate Revenue: 1.7 billion USD (–45%)

Assets Under Management: 4.6 trillion USD (+18%)

Client Assets: 6.8 trillion USD (+20%)

JPMorgan’s Q3 2025 results came in above market expectations. Net income totalled 14.4 billion USD, with EPS at 5.07 USD (versus a consensus forecast of roughly 4.85 USD). Revenue reached 47.1 billion USD, up 9% year-on-year, mainly supported by strong trading and investment banking activity. Compared with the previous quarter, profit was slightly down (−4%), primarily due to higher expenses and increased provisions for potential credit losses.

The Commercial and Investment Bank division generated 19.9 billion USD (+17% y/y), driven by a 16% rise in fees and 25% growth in trading income. The Consumer & Community Banking segment contributed 19.5 billion USD (+9% y/y), with card spending up 9% and the charge-off rate falling from 3.4% in the previous quarter to 3.15%. The Asset & Wealth Management business also delivered solid growth: assets under management rose to 4.6 trillion USD (+18%), and segment profit reached 1.7 billion USD.

The bank continued to return capital to shareholders: during the quarter, it paid out 4.1 billion USD in dividends and repurchased 8 billion USD worth of shares. Return on tangible common equity (ROTCE) stood at 20%, indicating strong business efficiency.

Management upgraded the forecast for net income for 2025 to 95.8 billion USD. In Q4, the bank projected approximately 25 billion USD in interest income and around 24.5 billion USD in expenses. The forecast for charge-offs on cards was also slightly improved.

The main issues in Q3 were related to the increase in credit expenses, which amounted to 3.4 billion USD in the past quarter, including charge-offs and the creation of new reserves. Part of the expenses was related to losses resulting from the bankruptcy of the auto lender Tricolor (around 170 million USD). Management noted that future results could be impacted by a combination of geopolitical tensions, potential new tariffs, high inflation, and worsening credit quality.

JPMorgan Chase & Co. Q4 2025 financial results

On 13 January 2026, JPMorgan Chase & Co. released its Q4 results for the 2025 financial year. Below are the key figures compared with the same period in 2024:

Revenue: 46.8 billion USD (+7%)

Net income: 13.0 billion USD (–7%)

Earnings per share (EPS): 4.63 USD (–4%)

Net interest income: 25.1 billion USD (+7%)

Consumer & Community Banking revenue: 19.4 billion USD (+6%)

Commercial & Investment Bank revenue: 19.4 billion USD (+10%)

Asset & Wealth Management revenue: 6.5 billion USD (+13%)

Corporate revenue: 1.5 billion USD (–26%)

Assets under management: 4.8 trillion USD (+18%)

Client assets: 7.1 trillion USD (+20%)

For Q4 2025, JPMorgan Chase reported strong revenue. However, the bottom line was impacted by a one-off reserve related to the Apple Card transaction. Net income totalled 13.0 billion USD, earnings per share were 4.63 USD, and revenue reached 45.8 billion USD (46.8 billion USD on a managed basis, up 7% year-on-year).

Excluding the one-off factor, the results are significantly stronger. The bank set aside a 2.2 billion USD reserve for the future purchase of the Apple Card portfolio, which reduced EPS by 0.60 USD. Without this reserve, earnings per share would have been 5.23 USD, exceeding market expectations, while revenue met consensus estimates.

Income sources showed positive dynamics. Net interest income rose to 25.1 billion USD (+7% year-on-year), non-interest income reached 21.7 billion USD (+7%), and Markets revenue hit 8.2 billion USD (+17%) due to high client activity. Expenses increased to 24.0 billion USD (+5%), partially offsetting the positive impact of revenue growth.

Results varied by segment. Consumer & Community Banking generated 3.6 billion USD in profit on revenue of 19.4 billion USD (+6% year-on-year), but profit declined due to the Apple Card reserve and higher credit costs. The Commercial & Investment Bank segment performed better: profit of 7.3 billion USD (+10%), revenue of 19.4 billion USD (+10%), with markets offsetting weakness in investment banking fees. Asset & Wealth Management also saw growth: profit of 1.8 billion USD (+19%) and revenue of 6.5 billion USD (+13%).

Credit metrics worsened on paper, but the cause was mainly one-off. Credit costs were 4.7 billion USD, write-offs were 2.5 billion USD, with the main contribution coming from the 2.2 billion USD reserve for the Apple Card. The current card portfolio remains stable: net charge-offs was 3.14%.

In terms of capital management and shareholder returns, the bank remained active. During the quarter, it paid 4.1 billion USD in dividends (1.50 USD per share) and repurchased 7.9 billion USD worth of shares.

The 2026 forecast indicated stable revenue growth alongside higher expenses. JPMorgan expected net interest income of around 103 billion USD, expenses of approximately 105 billion USD, and credit card net charge-offs of about 3.4%. This implied continued strong income generation, but with higher costs already factored in.

JPMorgan Chase & Co. Q1 2026 financial results

On 14 April 2026, JPMorgan Chase & Co. (NYSE: JPM) released its Q1 2026 results, compared with the same period in 2025. Key figures are as follows:

Revenue: 50.5 billion USD (+10%)

Net Income: 16.5 billion USD (+13%)

Earnings Per Share (EPS): 5.94 USD (+17%)

Net Interest Income: 25.5 billion USD (+7%)

Consumer & Community Banking Revenue: 19.6 billion USD (+7%)

Commercial & Investment Bank Revenue: 23.4 billion USD (+19%)

Asset & Wealth Management Revenue: 6.4 billion USD (+11%)

Corporate Revenue: 1.2 billion USD (-47%)

Assets Under Management: 4.8 trillion USD (+16%)

Client Assets: 7.1 trillion USD (+18%)

JPMorgan delivered a stronger and cleaner report for Q1 2026 than the previous quarter. Unlike Q4 2025, when earnings were weighed down by a 2.2 billion USD reserve related to the Apple Card portfolio, there was no comparable one-off pressure this quarter. Net income reached 16.5 billion USD, EPS reached 5.94 USD, and revenue totalled 50.5 billion USD, a 10% year-on-year increase, comfortably surpassing market expectations of 5.45 USD EPS and 49.2 billion USD revenue.

Revenue dynamics were positive across key segments. Net interest income rose to 25.5 billion USD (+9% year-on-year), while non-interest income increased to 25.1 billion USD (+11%). Trading operations and investment banking were the main contributors, with market-driven revenues reaching a record 11.6 billion USD (+20%), and investment banking fees increasing by 28%. Expenses rose to 26.9 billion USD (+14%), reflecting higher employee compensation, marketing, brokerage fees, and technology investments.

Lending remained stable. Total credit costs amounted to 2.5 billion USD, compared with 3.3 billion USD a year earlier. Net loan charge-offs remained virtually unchanged at 2.3 billion USD, while the net increase in reserves fell to 191 million USD from 973 million USD a year earlier. The credit card net charge-off rate stood at approximately 3.46–3.47%.

The bank continued to return capital to shareholders. During the quarter, it paid dividends totalling 4.1 billion USD, or 1.50 USD per share, and repurchased shares worth 8.1 billion USD. The CET1 capital ratio remained robust at 14.3%, while tangible book value per share increased by 8% to 128.38 USD. This confirmed that the bank's balance sheet remained very strong despite returning significant capital to shareholders.

The outlook for 2026 remained confident but more cautious. JPMorgan expected net interest income of around 103 billion USD, or approximately 95 billion USD excluding market-related businesses. The credit card net charge-off rate was projected at 3.4%, while adjusted expenses were expected to reach 105 billion USD. This indicated that management expected to maintain a high level of income despite higher costs, while retaining a prudent approach due to the bank's exposure to market conditions and interest rates.

JPMorgan Chase & Co. Q2 2026 financial results

On 14 July 2026, JPMorgan Chase & Co. published its results for Q2 of the 2026 calendar year, which ended on 30 June. The key figures are presented below, compared with the corresponding period in 2025:

Revenue: 58.0 billion USD (+27%)

Net Income: 21.2 billion USD (+41%)

Earnings Per Share (EPS): 7.70 USD (+47%)

Net Interest Income: 25.6 billion USD (+10%)

Consumer & Community Banking Revenue: 20.3 billion USD (+8%)

Commercial & Investment Bank Revenue: 24.9 billion USD (+27%)

Asset & Wealth Management Revenue: 6.9 billion USD (+19%)

Corporate Revenue: 6.0 billion USD (+293%)

Assets Under Management: 5.1 trillion USD (+18%)

Client Assets: 7.7 trillion USD (+18%)

JPMorgan Chase & Co. delivered an even stronger performance in Q2 2026 than in the previous quarter. However, part of the improvement was driven by one-off factors. During the quarter, the bank recognised 4.6 billion USD in net income from transactions involving Visa shares, as well as approximately 1.0 billion USD in gains from certain equity investments. Excluding these significant items, net income amounted to 16.9 billion USD, while EPS was 6.14 USD.

By business segment, the Commercial & Investment Bank was the primary growth driver, with revenue increasing by 27% and net profit rising by 46%. Consumer & Community Banking also maintained growth, while Asset & Wealth Management continued to expand on the back of client asset inflows.

Credit quality remained stable. Credit costs totalled 2.5 billion USD, unchanged from Q1, while the credit card net charge-off rate declined to 3.34% from 3.46% in the previous quarter.

The bank continued to return capital to shareholders. During the quarter, it paid dividends totalling 4.0 billion USD, or 1.50 USD per share, and repurchased 6.2 billion USD in shares. The CET1 capital ratio remained robust at 14.1%, while tangible book value per share increased to 133.01 USD.

The outlook for 2026 became slightly more optimistic for net interest income but more cautious regarding expenses. JPMorgan raised its forecast for net interest income, excluding Markets, to 105.5 billion USD, while simultaneously increasing its expense guidance to 107.5 billion USD. This suggests that the bank expects business activity to remain strong, although higher costs are likely to continue weighing on efficiency.

Analysis of key valuation multiples for JPMorgan Chase & Co.

The table below presents JPMorgan Chase & Co.'s key valuation multiples as of the end of Q2 2026, calculated using a share price of 342 USD.

| Multiple | What it indicates | Value | Comment |

|---|---|---|---|

| P/E (TTM) | Price-to-earnings (P/E) ratio (trailing 12 months) | 14.65 | ⬤ Moderate valuation for JPMorgan |

| P/B | Price-to-book (P/B) ratio | 2.57 | ⬤ High valuation relative to book value |

| P/TBV | Price-to-tangible book value (P/TBV) ratio | 3.02 | ⬤ The premium to tangible book value remains high |

| Forward P/E | Forward price-to-earnings (forward P/E) ratio | 14.42 | ⬤ The market expects strong earnings and assigns little discount |

| ROE | Return on Equity (ROE) | 24% | ⬤ Strong return on equity |

| ROTCE | Return on Tangible Common Equity (ROTCE) | 23% | ⬤ Business quality and capital efficiency remain very strong |

| CET1 ratio | Common Equity Tier 1 (CET1) capital ratio | 14.1% | ⬤ Strong capital buffer |

| Tier 1 Capital Ratio | Tier 1 capital ratio | 15.1% | ⬤ Robust balance sheet |

| NIM / Net yield excluding Markets | Yield on interest-earning assets, excluding Markets activities | 3.65% | ⬤ This is a strong level for a large bank |

| Efficiency Ratio / Overhead Ratio | Cost-to-income ratio (efficiency ratio) | 47% | ⬤ Costs remain well controlled |

| NPL Ratio | Non-performing loans (NPL) ratio | 0.74% | ⬤ Strong credit quality |

| Coverage Ratio | Loan loss reserve coverage ratio | 232% | ⬤ Comfortable coverage of non-performing loans |

| Payout Ratio | Dividend payout ratio | 25.7% | ⬤ Dividend payments do not place pressure on capital |

Following Q2 2026, JPMorgan remains a very strong bank in terms of business quality, profitability, and balance sheet strength. ROE and ROTCE remain at high levels, capitalisation is robust, costs are well controlled, and credit quality remains stable.

At the same time, the stock continues to trade at a significant premium to book value. A P/B ratio above 2.5 and a P/TBV ratio of around 3.0 indicate that the market has already priced JPMorgan's high-quality franchise into the share price. Although the P/E ratio appears moderate, it should be interpreted with caution, as one-off gains from Visa and certain equity investments supported the second-quarter results.

Overall, JPMorgan shares can currently be viewed as a high-quality investment for investors who prioritise business resilience and consistent financial performance over the potential for rapid gains driven by a low valuation.

Analyst forecasts for JPMorgan Chase & Co.’s stock for 2026

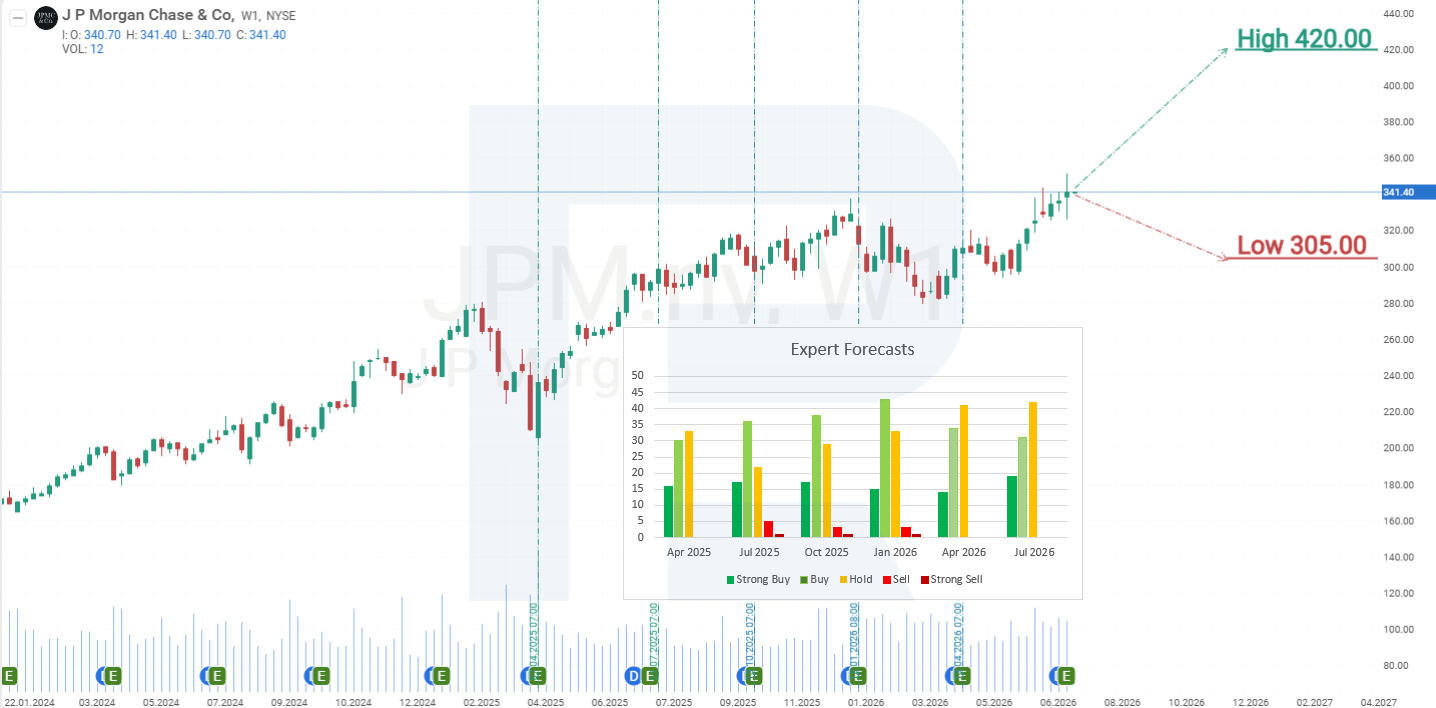

- Barchart: of 25 analysts, 11 rate JPMorgan Chase & Co. shares as Strong Buy, 2 as Moderate Buy, and 12 as Hold. The highest price target is 420 USD, while the lowest is 305 USD.

- MarketBeat: of 28 analysts, 16 rate JPMorgan Chase & Co. shares as Buy, while 12 rate them as Hold. The highest price target is 420 USD, while the lowest is 305 USD.

- TipRanks: of 15 analysts, 9 rate JPMorgan Chase & Co. shares as Buy, while 6 rate them as Hold. The highest price target is 420 USD, while the lowest is 305 USD.

- Stock Analysis: of 24 analysts, 8 rate JPMorgan Chase & Co. shares as Strong Buy, 4 as Buy, and 12 as Hold. The highest price target is 420 USD, while the lowest is 305 USD.

JPMorgan Chase & Co. stock price forecast for 2026

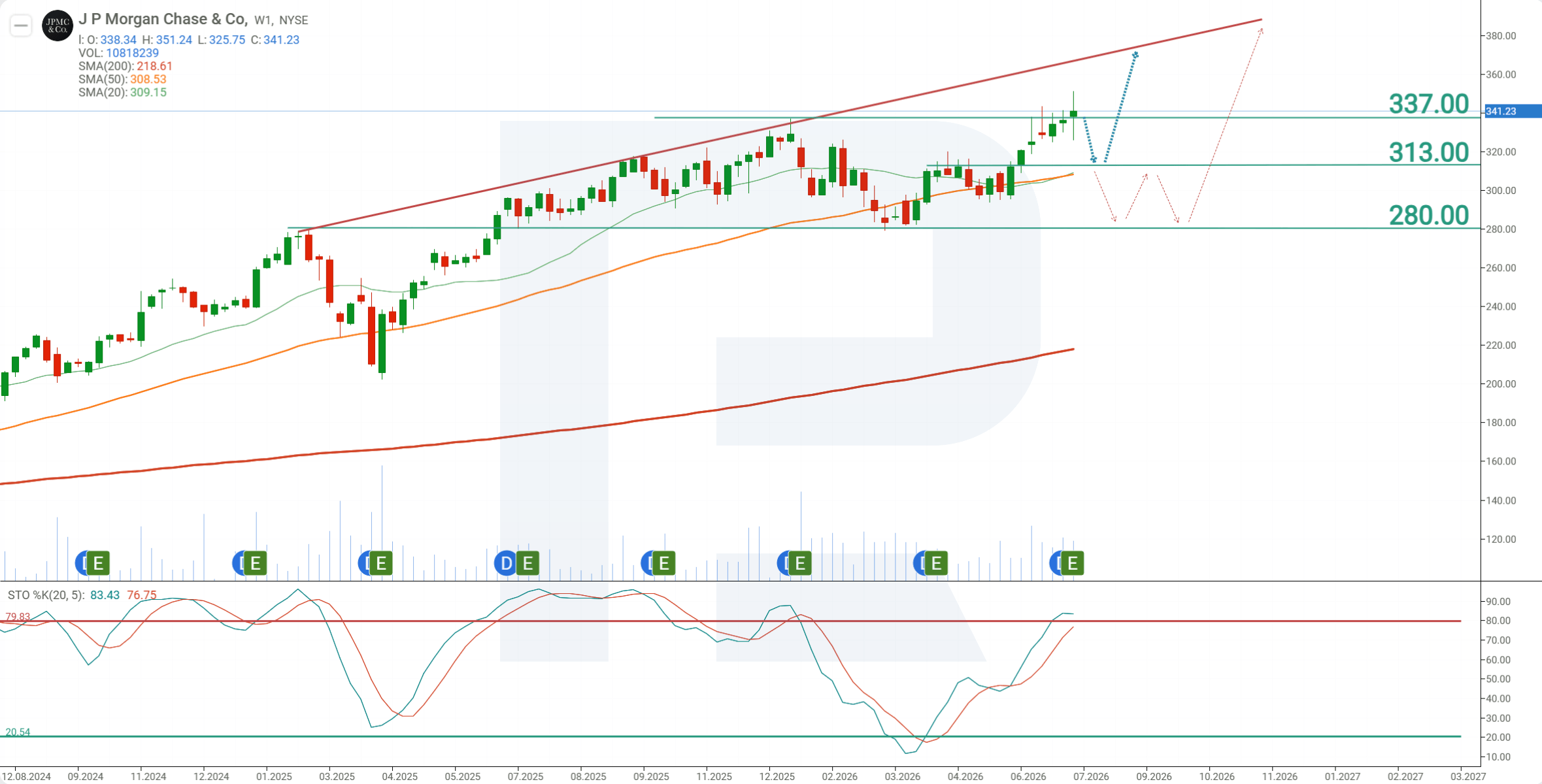

On the weekly chart, JPMorgan shares remain in an uptrend, with JPM trading above the 200-period Moving Average. However, the Stochastic indicator is in overbought territory, signalling the potential for a corrective decline before the next upward move. Based on the current price action in JPMorgan Chase & Co. shares, the following scenarios outline the potential movement of JPM in 2026:

The base-case forecast for JPM shares envisages a test of support at 313 USD, followed by a rebound and an advance towards resistance at 370 USD.

The alternative forecast for JPM stock assumes a deeper correction. In this scenario, the price could decline towards support at 280 USD. A rebound from this level would signal the end of the correction and the resumption of the upward move, with the next target at 380 USD.

Risks of investing in JPMorgan Chase & Co. stock

Investment risks for JPMorgan Chase’s shares include the following factors:

- Resurgence of inflation: if inflation begins to rise again, the Federal Reserve may be forced to delay interest rate cuts or, worse, raise rates further. This could lead to a wave of loan delinquencies, requiring higher provisions for credit losses and resulting in increased write-offs under this line of expense.

#. Rising deposit interest rates: if policy rates increase, the bank will also need to raise deposit rates to stay competitive or risk customer attrition. The resulting rise in interest payments on deposits would negatively impact the bank’s profitability.

- Decline in stock indices: as investment banking currently generates the strongest revenue growth, a fall in stock indices could adversely affect JPMorgan Chase’s investment operations. This could also impact the credit sector, as stocks are often used as collateral for loans.

- Trade War: The tariffs imposed by the Trump administration could negatively impact JPMorgan's revenue. Increases in tariffs typically lead to higher business costs, reduced consumer demand, and a slowdown in economic activity. This, in turn, lowers demand for banking services as companies become more cautious, reducing their activity in the capital markets and scaling back mergers and acquisitions, which diminishes JPMorgan’s fee income. Furthermore, if trade tensions persist, the bank’s global clients may scale back investment plans, freeze export flows, and reduce overall activity, which would negatively impact all areas of the bank’s operations – from hedging and foreign exchange to traditional lending.

Risks associated with inflation, interest rates, and trade wars pose significant threats to JPMorgan Chase’s earnings. These factors should be carefully considered when assessing the investment appeal of the bank’s shares.

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex bears no responsibility for trading results based on trading recommendations described in these analytical reviews.