McDonald's after strong results: holding above 320 USD with potential growth towards 375 USD

McDonald's ended 2025 with results that exceeded expectations, delivering solid growth in revenue and profit. With margins remaining stable and the company maintaining its dividend policy, the shares retain upside potential towards 375 USD.

McDonald's Corporation (NYSE: MCD) released its Q4 2025 results, reporting a confident beat of analysts’ expectations for both revenue and earnings. Quarterly revenue rose by 10% to 7.01 billion USD, exceeding the market forecast of 6.81 billion USD. Adjusted earnings per share reached 3.12 USD, compared with the expected 3.05 USD, supported by a 6% increase in global comparable sales. In the US, comparable sales growth was even stronger at 7%, driven by successful marketing campaigns and a continued focus on menu affordability.

Despite the strong figures, the company warned of a possible slowdown in sales growth in the first quarter of 2026 due to adverse weather conditions in January and a high base effect from the previous year. As part of its long-term outlook, McDonald's plans to open approximately 2,600 new restaurants in 2026 and expects an operating margin in the range of 45–47%.

Overall, the report confirmed the resilience of McDonald's business model.

This article examines McDonald's Corporation, provides an analysis of McDonald's Corporation (MCD) quarterly results, and presents a technical analysis of McDonald's Corporation shares, forming the basis for a forecast for MCD stock in 2026. It also outlines the company’s business model, assesses the risks of investing in McDonald's Corporation, and presents expert forecasts for McDonald's Corporation shares for 2026.

About McDonald's Corporation

McDonald's Corporation is the world's largest fast-food restaurant chain, founded in 1940 by brothers Richard and Maurice McDonald (McDonald Brothers) in San Bernardino, California. In 1955, Ray Kroc (Raymond Kroc) joined the company and transformed it into an international franchise. The company went public on 21 April 1965, listing on the New York Stock Exchange (NYSE: MCD).

McDonald's specialises in selling burgers, fries, beverages, and other fast-food products. The company is expanding its digital services and loyalty programs while adapting its menu to local markets.

McDonald's also owns one of the largest property portfolios in the world. A significant portion of its profits comes from leasing premises to its franchisees, making it not only a restaurant business but also a major player in commercial real estate.

McDonald's Corporation key financial flows

McDonald's business model is unique, combining elements of the traditional restaurant industry with franchising and real estate management. The company's main revenue streams fall into four key categories:

- Franchising: most of McDonald's restaurants operate under the franchise model, where the company grants its partners the right to use its brand, recipes, quality standards, and other corporate guidelines. Revenue in this segment comes from an initial franchisee fee paid by partners to open a McDonald's restaurant, as well as an ongoing percentage of sales.

- Company-operated restaurants: revenue in this business comes directly from product and service sales, with the company covering all operational expenses for these locations.

- Real estate income: McDonald's owns numerous properties for operating restaurants. As the landowner or leaseholder, it earns income from leasing or subleasing the land to its franchisees. In some cases, McDonald's only owns the land, while partners build and own the buildings. This strategy enables the company to generate stable, long-term income independent of the success of specific restaurants.

- Supply chain and logistics: McDonald's often controls its franchisees' entire supply and procurement chain, generating additional income through markups on products and ingredients.

This diversified business model allows the company to sustain long-term growth and reduce reliance on a single revenue stream. In its quarterly earnings reports, McDonald's provides separate financial data for franchised and company-operated restaurants, while income from other segments is under Other Revenues.

McDonald's Corporation Q3 2024 earnings results

McDonald's released its financial results for Q3 2024 on 29 October. Below is a comparison with the same period in 2023:

- Revenue: 6.87 billion USD (+3%)

- Net income: 2.25 billion USD (–3%)

- Earnings per share: 3.13 USD (–1%)

- Operating income: 3.18 billion USD (–1%)

- Revenues from franchised restaurants: 4.09 billion USD (+1%)

- Franchised restaurant occupancy expenses: 646 million USD (+3%)

- Revenues from company-owned restaurants: 2.65 billion USD (+4%)

- Company-owned restaurant expenses: 2.24 billion USD (+5%)

- Other revenues: 124 million USD (+39%)

In its commentary on the report, McDonald's management highlighted cautious consumer spending and inflationary pressures, which impacted sales and led to flat performance overall. In the US, a modest increase was recorded, with comparable sales rising by 0.3%, driven by effective promotions and menu enhancements. However, international markets saw a decline, reflecting changes in consumer preferences.

For its Q4 2024 outlook, management did not provide specific numerical forecasts but expressed a prudent stance regarding the future economic environment. They noted that they anticipated ongoing challenges related to consumer spending and potential adverse effects from currency fluctuations, particularly in emerging markets. Despite these challenges, McDonald's leadership remained optimistic about its long-term strategic initiatives, focusing on restoring consumer confidence following a recent E. coli incident in the US that affected the brand's reputation, and enhancing marketing efforts to attract customers.

McDonald's Corporation Q4 2024 earnings results

On 10 February, McDonald's released its Q4 2024 report, indicating that revenue remained unchanged compared to the same period in 2023. Below are the key financial metrics:

- Revenue: 6.39 billion USD (unchanged)

- Net income: 2.02 billion USD (–1%)

- Earnings per share: 2.8 USD (unchanged)

- Operating income: 2.86 billion USD (+2%)

- Revenues from franchised restaurants: 3.96 billion USD (+2%)

- Franchised restaurant occupancy expenses: 635 million USD (unchanged)

- Revenues from company-owned restaurants: 2.31 billion USD (–7%)

- Company-owned restaurant expenses: 1.98 billion USD (–5%)

- Other revenue: 120 million USD (+88%)

According to CEO Chris Kempczinski, McDonald's faced external challenges in Q4 2024, including a decline in consumer spending and an incident involving bacterial contamination in its products, which negatively affected overall performance. He noted that while the results were generally strong, they fell short of expectations in certain international markets and in customer traffic patterns.

For 2025, the company remained optimistic about profit growth, with management forecasting that the operating margin will rise to a mid-to-high range, surpassing the adjusted margin of 46.3% achieved in 2024. In 2025, McDonald's planned to focus on expanding affordable menu options to attract price-conscious consumers, as well as on its global digital transformation, which has already become a key driver of revenue growth.

Despite flat revenue and net income in Q4 2024, investors responded positively to McDonald's optimistic outlook for 2025, leading to a 4.7% increase in its share price following the report's release.

McDonald's Corporation Q1 2025 earnings results

On 1 May, McDonald's released its earnings report for Q1 2025, which ended on 31 March. Below are its key financial indicators:

- Revenue: 5.96 billion USD (–3%)

- Net income: 1.87 billion USD (–3%)

- Earnings per share: 2.60 USD (–2%)

- Operating income: 2.64 billion USD (–3%)

- Revenues from franchised restaurants: 3.66 billion USD (–2%)

- Franchised restaurant occupancy expenses: 620 million USD (–1%)

- Revenues from company-owned restaurants: 2.31 billion USD (–7%)

- Company-owned restaurant expenses: 2.13 billion USD (–9%)

- Other revenues: 162 million USD (+78%)

In Q1 2025, McDonald's faced significant challenges, leading to a 3.6% drop in comparable sales in the US, the steepest fall since 2020. This decline was driven by a fall in restaurant traffic as low- and middle-income consumers tightened their budgets amid inflation and economic uncertainty. CEO Chris Kempczinski noted that while high-income customers remain loyal, most consumers have become more cautious.

Global markets also experienced a decline, with global comparable sales down by 1%, missing analysts’ expectations of 0.95% growth. The downturn was attributed to lower consumer spending caused by inflation, tariff uncertainty, and broader economic challenges, particularly evident in the US and Europe. However, some franchising markets, such as the Middle East and Japan, saw demand rebound following earlier boycotts.

From an operational perspective, McDonald's faced pressure due to rising costs. Wage increases, especially in California, and higher raw material prices negatively impacted profitability. Additionally, challenges arose in maintaining the brand’s affordable image: price increases disrupted the usual value programs, prompting customers to reconsider their preferences.

Moreover, the partnership with Krispy Kreme proved disappointing. A nationwide launch of a major doughnut offering in McDonald's restaurants was suspended due to weaker-than-expected demand. Both companies revised their partnership strategy.

Despite the challenges, McDonald's continued to prioritise long-term growth. In 2025, the company planned to open approximately 2,200 new restaurants worldwide, including about 1,000 in China, increasing the number of outlets by 4%. Capital expenditure was projected between 3.0 and 3.2 billion USD, mainly aimed at opening new locations and advancing technology.

McDonald's Corporation Q2 2025 earnings results

On 6 August, McDonald's released its Q2 2025 results for the period ended 30 June. The key financial metrics are as follows:

- Revenue: 6.84 billion USD (+5%)

- Net income: 2.25 billion USD (+11%)

- Earnings per share: 3.19 USD (+12%)

- Operating income: 3.23 billion USD (+11%)

- Revenues from franchised restaurants: 4.21 billion USD (+7%)

- Franchised restaurant occupancy expenses: 654 million USD (+4%)

- Revenues from company-owned restaurants: 2.46 billion USD (0%)

- Company-owned restaurant expenses: 2.08 billion USD (0%)

- Other revenues: 172 million USD (+93%)

McDonald's published its Q2 2025 results, which surpassed market expectations. The company recorded a 3.8% increase in global comparable sales, supported by all key segments, including the US, Europe, and franchised markets. Consolidated revenue rose 5% to 6.84 billion USD, while adjusted earnings per share reached 3.19 USD, up 12% year-on-year and exceeding the market consensus of around 3.14–3.15 USD. Net income increased by 11% to 2.25 billion USD, with system-wide sales up 8%. The main growth drivers were value-focused programs such as the ‘Meal Deal’ and affordable snacks, the launch of new menu items, and active expansion of digital services and the loyalty program, which generated approximately 9 billion USD across the McDonald's system.

The company stated that it expected stronger financial performance in the second half of 2025, projected an operating margin in the range of 40–45%, and maintained its plan to open around 2,200 new restaurants, a significant portion of which will be in the US and China. Management emphasised that the strategy would focus on expanding market presence, driving digital transformation, and maintaining price affordability for consumers amid continued pressure on household incomes.

McDonald's Corporation Q3 2025 earnings results

On 5 November, McDonald's released its Q3 2025 results for the quarter ended 30 September. The key financial highlights are as follows:

- Revenue: 7.08 billion USD (+3%)

- Net income (non-GAAP): 2.31 billion USD (–1%)

- Earnings per share (non-GAAP): 3.22 USD (0%)

- Operating income: 3.36 billion USD (+5%)

- Revenue from franchised restaurants: 4.36 billion USD (+7%)

- Franchised restaurant occupancy expenses: 666 million USD (+3%)

- Revenue from company-owned restaurants: 2.56 billion USD (–3%)

- Company-owned restaurant expenses: 2.17 billion USD (–3%)

- Other revenue: 151 million USD (+22%)

McDonald's Q3 2025 report proved as steady as the company’s business itself. Revenue rose 3% to 7.08 billion USD, while earnings per share remained unchanged at 3.22 USD. Comparable sales increased by 3.6%, slightly exceeding expectations, though overall revenue and profit came in just below analyst forecasts.

Management adopted a cautious outlook: McDonald's expects pressure on consumers, particularly in the US and Europe, to persist at least through 2026. The company is relying on value-priced combo meals, the return of Snack Wraps, and the expansion of its loyalty programs to retain customers amid constrained household incomes.

A growing number of younger consumers are choosing McDonald's over more expensive cafés, helping sustain traffic, though the average spend per visit among this group is lower. At the same time, inflation continues to weigh on lower-income households, prompting many to scale back spending and cook more at home. To retain customers, McDonald's is offering more discounts and promotions, sharing part of the cost burden with franchisees. This supports revenue but limits profit growth.

Overall, the report reflected a resilient but no longer high-growth business. McDonald's continues to generate solid earnings even in a challenging inflationary environment and remains effective at attracting a younger, price-sensitive audience. However, profit growth potential remains constrained by the need to constantly balance margin protection with aggressive pricing initiatives aimed at sustaining customer demand.

McDonald's Corporation Q4 2025 earnings results

On 11 February, McDonald's released its Q4 2025 results for the quarter ended 31 December. The key financial figures are presented below:

- Revenue:7.01 billion USD (+10%)

- Net income (non-GAAP):2.23 billion USD (+9%)

- Earnings per share (non-GAAP):3.12 USD (+10%)

- Operating income:3.16 billion USD (+10%)

- Revenues from franchised restaurants:4.31 billion USD (+9%)

- Franchised restaurant occupancy expenses:678 million USD (+7%)

- Revenues from company-owned restaurants:2.54 billion USD (+10%)

- Company-owned restaurant expenses:2.16 billion USD (+9%)

- Other revenues:162 million USD (+35%)

In Q4 2025, McDonald's delivered results above market expectations. Global comparable sales increased by 5.7%, while analysts had expected approximately 3.7–3.9%. Comparable sales in the US rose by 6.8% versus expectations of around 4.9%; in the International Operated Markets segment, growth reached 5.2%; and in the International Developmental Licensed Markets segment, 4.5%. The company also exceeded forecasts on the financial side: revenue reached 7.01 billion USD compared with expectations of 6.84 billion USD, while adjusted earnings per share came in at 3.12 USD versus the forecast of 3.05 USD.

McDonald's also improved its profitability metrics. Operating income increased by 10% to 3.16 billion USD, while net income rose by 7% to 2.16 billion USD. Operating margin stood at approximately 45%. The report included one-off pre-tax charges of 80 million USD related to restructuring under the Accelerating the Organization program. Excluding these items, operating income growth would have been higher, at approximately 13%. This indicates that underlying operating performance was stronger than headline figures suggest, with the higher-margin franchised business making the primary contribution.

The company did not provide specific numerical guidance for 2026. However, in 2026, the corporation aims to open 2,600 new restaurants (with net unit growth expected at approximately 2,100 restaurants after closures) and maintain an operating margin of 45–47%. Investors also received an important signal: the quarterly dividend was increased by 5% to 1.86 USD per share. The payment is scheduled for 17 March 2026 for shareholders of record as of 3 March. This suggests that management remains confident in the sustainability of cash flows, even in the absence of formal financial guidance.

Among the risks is McDonald's debt burden. As of the end of 2025, long-term debt totalled approximately 39.97 billion USD, while interest expenses in Q4 amounted to 410 million USD. The company also carries significant lease liabilities and reports negative shareholders’ equity, which is typical for businesses with substantial shareholder distributions but increases sensitivity to interest rates. In 2025, 5.115 billion USD was allocated to dividends and a further 2.06 billion USD to share buybacks. It is therefore important to compare these distributions with free cash flow and debt dynamics to assess the sustainability of the current level of capital returns.

Analysis of key valuation multiples for McDonald's Corporation

Below are McDonald's key valuation multiples based on Q4 of the 2026 financial year, calculated using a share price of 327 USD.

| Multiple | What it indicates | Value | Commentary |

|---|---|---|---|

| P/E (TTM) | The price of 1 USD of earnings over the past 12 months | 27.3 | ⬤ The valuation is in line with the historical average range (25–30), while earnings (EPS of 11.95 USD) increased by 5%. |

| P/S (TTM) | The price of 1 USD of annual revenue | 8.7 | ⬤ A high level for the retail sector, but typical for McDonald's due to the high-margin franchising model. |

| EV/Sales (TTM) | Enterprise value to revenue, including debt | 10.2 | ⬤ Reflects the company’s substantial debt burden, which is incorporated into enterprise value. |

| P/FCF (TTM) | The price of 1 USD of free cash flow | 32.5 | ⬤ Cash flow remains stable despite ongoing investment. |

| FCF Yield (TTM) | Free cash-flow yield for shareholders | 3.1% | ⬤ Free cash flow yield exceeds that of many technology giants. |

| EV/EBITDA (TTM) | Enterprise value to EBITDA | 18.8 | ⬤ The metric is moderate for an industry leader. |

| EV/EBIT (TTM) | Enterprise value to operating profit | 22.1 | ⬤ Confirms efficient management of operating expenses. |

| P/B | Price to book value | - | ⬤ Negative shareholders’ equity (due to share buybacks) makes this multiple uninformative for analytical purposes. |

| Forward P/E | Forward price-to-earnings (P/E) ratio | 25.1 | ⬤ The forecast EPS for 2026 (~13.00 USD) implies multiple compression, making the current price appear justified. |

| Net Debt/EBITDA | Debt load relative to EBITDA | 2.8 | ⬤ Leverage is noticeable; however, for a stable business with predictable cash flows, this level is generally considered manageable. |

| Interest Coverage (TTM) | Operating profit to interest expense ratio | 10.1 | ⬤ Operating income covers interest expense more than ten times over, supporting financial resilience. |

Valuation multiples analysis for MCD – conclusion

The key valuation multiples (P/E of 27.3 and EV/EBITDA of 18.8) suggest that the market values the company fairly. Unlike the technology sector, where expectations often inflate multiples, McDonald's delivers organic revenue growth of 4% and net income growth of 4%, supported by strong comparable sales performance.

A critical consideration remains negative shareholders’ equity, resulting from an aggressive capital return strategy through buybacks (approximately 2 billion USD of shares repurchased during the year). Although leverage is elevated, it is fully supported by the company’s ability to generate cash and its strong interest coverage.

Based on the 2025 results, MCD shares represent a balanced investment case. The company continues to pass inflationary pressures on to consumers while preserving margins. A relatively low free cash flow yield (3.1%) may limit the potential for sharp upside in the share price; however, the stability of shareholder distributions makes the stock attractive for conservative portfolios.

Expert forecasts for McDonald's Corporation shares in 2025

- Barchart: 18 out of 36 analysts assigned a Strong Buy rating to McDonald's shares, 1 assigned a Moderate Buy rating, 16 assigned a Hold rating, and 1 assigned a Strong Sell rating. The upper price target is 380 USD, and the lower bound is 260 USD.

- MarketBeat: 16 out of 31 specialists assigned a Buy rating, 13 assigned a Hold rating, and 2 assigned a Sell rating. The upper price target is 380 USD, and the lower bound is 250 USD.

- TipRanks: 16 out of 26 professionals assigned a Buy rating, and 10 assigned a Hold rating. The upper price target is 380 USD, and the lower bound is 305 USD.

- Stock Analysis: 7 out of 26 experts assigned a Strong Buy rating to McDonald's shares, 7 assigned a Buy rating, 11 assigned a Hold rating, and 1 assigned a Strong Sell rating. The upper price target is 380 USD, and the lower bound is 260 USD.

McDonald's Corporation stock price forecast for 2026

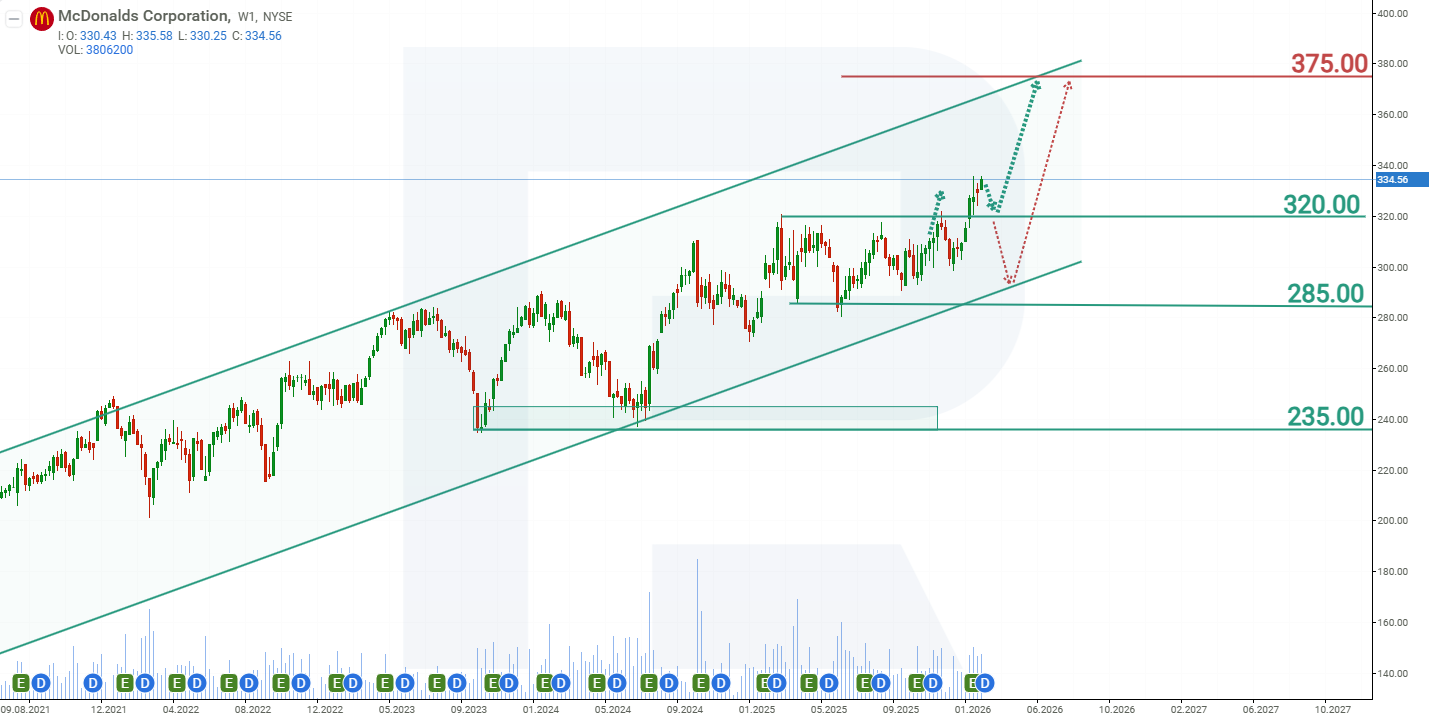

On the weekly chart, McDonald's shares are trading within an upward channel and are approaching their historical high of around 320 USD for the third time. Given the company’s strong financial position and proven ability to navigate challenging periods, there is a high likelihood that the price will break above its previous record this time. Based on the current performance of McDonald's Corporation shares, the potential price scenarios for 2025 are as follows:

The base-case forecast for McDonald's Corporation stock anticipates a breakout above resistance at 320 USD, followed by a further rise towards the upper boundary of the channel at 370 USD.

The alternative forecast for McDonald's Corporation shares envisions another pullback from resistance around 320 USD. In this case, MCD shares could decline towards the trendline near 285 USD. A rebound from this level would signal the end of the correction and the resumption of the uptrend, with the next upside target at the upper boundary of the channel around 370 USD.

Risks of investing in McDonald's Corporation stock

When investing in McDonald's Corporation stock, it is essential to consider the risks the company may face in 2025. Below are the key risks:

- Food safety issues: the discovery of E. coli in McDonald's products in October 2024 resulted in a 0.3% decrease in revenue in Q4, affecting consumer trust. Although the FDA confirmed no current food safety issues with McDonald's products, this incident highlighted the risks associated with foodborne illnesses, impacting both sales and the brand's reputation.

- Increased competition and shifting consumer preferences: with a growing number of competitors and a consumer shift towards healthier food options, McDonald's plans to expand its chicken menu, including the return of popular items like the Snack Wrap, to meet evolving consumer expectations.

- Operational challenges: while the introduction of the Snack Wrap to the menu aims to boost US sales, it could lead to operational issues due to longer preparation times, potentially affecting service speed and overall customer satisfaction.

- Economic factors: inflation continues to strain consumer spending. CEO Chris Kempczinski forecasts a challenging 2025 and notes that low-income customers will likely continue facing financial difficulties, which could reduce their dining-out expenditures.

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex bears no responsibility for trading results based on trading recommendations described in these analytical reviews.