Netflix stock forecast: shares could begin recovering after testing support at 60 USD

Netflix reported revenue growth in Q2 2026, but without the one-off income related to Warner Bros., its results were weaker than in Q1. The forecast for NFLX stock suggests a rebound from 60 USD and a rise towards 108 USD.

Netflix, Inc. (NASDAQ: NFLX) maintained double-digit growth in Q2 2026. Revenue increased by 13% year-on-year to 12.56 billion USD, operating profit rose by 11% to 4.19 billion USD, and net profit increased by 9% to 3.40 billion USD. Growth was driven by an expanding subscriber base, higher subscription prices, and continued expansion of the company's advertising business.

Unlike Q1, the second-quarter results were not boosted by the one-off income related to Warner Bros. As a result, Q2 provided a clearer picture of Netflix's underlying business performance. At the same time, the operating margin declined by 0.7 percentage points to 33.4%, while free cash flow decreased by 33% to 1.53 billion USD, primarily due to higher tax payments.

Netflix maintained its full-year 2026 operating margin guidance at 31.5% and continues to expect approximately 12.5 billion USD in free cash flow. Advertising revenue is projected to reach approximately 3 billion USD for the full year, confirming that advertising is gradually becoming an additional driver of the company's growth.

Investors reacted negatively to the earnings release. Following the publication of the results, Netflix shares fell by 8.6% in after-hours trading. The market's focus was less on the Q2 results than on the weaker guidance for the following quarter. Expected revenue and earnings per share came in slightly below analysts' forecasts. Additional pressure came from slowing growth and Netflix's decision to publish viewing-time data less frequently. The decline in the stock price was driven primarily by elevated investor expectations and concerns about the company's future growth trajectory.

This article examines Netflix, Inc., reviews the company's quarterly financial results, provides a fundamental analysis of its business, analyses the performance of NFLX stock through technical analysis, and presents a forecast for Netflix stock for 2026.

About Netflix, Inc.

Netflix, Inc. was founded on 29 August 1997 by Reed Hastings and Mark Randolph. The company initially delivered DVDs on a subscription basis. Clients could order a film through the website and receive it by post. In 2007, Netflix launched a streaming service, allowing users to watch movies and TV shows online.

The transition to live streaming was pivotal in the company’s history. Netflix began actively expanding its content library to include licensed films, series and original projects. By July 2024, Netflix had 277 million subscribers worldwide, making it the largest streaming platform.

Netflix, Inc.’s key financial flows

Netflix’s revenue mainly comes from streaming services, advertising, and other sources. The main components are outlined below:

- Subscription fees: Netflix’s primary revenue stream, derived from ad-supported and ad-free subscriptions.

- Advertising revenue: payments from companies for placing advertisements.

- Content licensing and distribution: revenue is generated from providing paid licences for Netflix’s original and purchased content to other platforms and TV channels. This segment also includes income from partnerships with telecommunication providers, cable companies, and other distributors that offer Netflix as part of their packages.

- Other revenue streams: sales of merchandise related to Netflix series and films (e.g. toys, apparel, and collectables). The company has also started investing in the gaming industry by offering mobile games based on its intellectual property, creating additional opportunities for revenue growth.

Most of Netflix’s revenue derives from streaming subscriptions, while advertising, licensing, and other business segments offer additional potential for income growth.

Netflix, Inc. Q2 2024 financial results

Netflix released its Q2 2024 report on 18 July. Below is a comparison of its results with the same period in 2023:

- Revenue: 9.56 billion USD (+17%)

- Net income: 2.15 billion USD (+44%)

- Earnings per share: 4.88 USD (+48%)

- Operating profit: 2.60 billion USD (+44%)

- Operating margin: 27.2% (+490 basis points)

- Total subscribers: 277.65 million (+16%)

Although the company’s subscriber numbers continue to increase quarter over quarter, this growth is gradually slowing. The increase in memberships in Q4 2023 surpassed previous figures by 13.13 million, followed by 9.32 million in Q1 2024 and 8.05 million in Q2 2024. Netflix is facing challenges in identifying new catalysts for subscriber growth. The company is now attracting new subscribers by addressing password sharing and reducing the cost of ad-supported subscription plans. Market participants are sensitive to these statistics; a look at the stock behaviour when Netflix reported a loss of 200 thousand subscribers in Q1 2022 reflects this, dragging the share price down by over 30% and continuing its decline.

Netflix’s management plans to stop publishing subscriber statistics from 2025 onwards to mitigate these challenges and focus investors’ attention on revenue per user, total revenue, and operating margin.

Amid slowing membership growth, the company is exploring new growth drivers, with advertising viewed as a potential source. Netflix’s management has noted that advertising is becoming increasingly significant to the company’s operations. However, building this business from scratch will take time, meaning it is unlikely to become the primary driver of revenue growth in 2024 and 2025.

Netflix forecasts 14% year-on-year revenue growth in Q3 2024, although a lower increase in paying users is expected compared to the same period in 2023. At the same time, no changes are anticipated for the global average revenue per user.

Based on the 2024 results, revenue is projected to rise by 14−15%, compared with the earlier forecast of 13−15%, while the operating margin is expected to reach 26%, up from the earlier estimate of 25%. The company’s goal remains to increase operating profit.

Netflix, Inc. Q3 2024 financial results

Netflix released its Q3 2024 report on 17 October. Below is a comparison of its data with the corresponding period in 2023:

- Revenue: 9.82 billion USD (+15%)

- Net income: 2.36 billion USD (+41%)

- Earnings per share: 5.40 USD (+20%)

- Operating profit: 2.94 billion USD (+25%)

- Operating margin: 29.6% (+720 basis points)

- Total subscribers: 282.7 million (+14%)

Co-CEO Theodore Sarandos noted that content production is recovering after last year’s strikes in Hollywood, with series rebounding more rapidly than films. The company’s advertising business showed significant growth, with the number of subscribers to ad-supported plans increasing by 35% from the previous quarter. More than half of new users in regions with ad services chose this package option. However, the company emphasised that effective ad monetisation will take time, and this segment will not become a primary revenue stream in the near term.

In Q4 2024, Netflix projected earnings per share of 4.20 USD, with revenue of 10.12 billion USD, representing annual revenue growth of 15%. The total number of subscribers was forecast to increase by 8.2 million to approximately 290.9 million.

The company anticipated that its advertising revenue would double in 2025, driven by a 150% increase in advertising commitments secured during 2024. Despite the upbeat forecast, Netflix noted that advertising was not expected to become a primary revenue driver in the near term. This guidance highlighted the company’s ongoing efforts to strengthen its position in the streaming market and diversify its revenue streams.

Netflix, Inc. Q4 2024 financial results

Netflix released a strong Q4 2024 report on 21 January. Below is a comparison of its results with the corresponding period in 2023:

- Revenue: 10.24 billion USD (+16%)

- Net income: 1.87 billion USD (+99%)

- Earnings per share: 4.27 USD (+102%)

- Operating profit: 2.27 billion USD (+51%)

- Operating margin: 22.2% (+530 basis points)

- Total subscribers: 301.6 million (+15%)

In its commentary on the Q4 2024 results, Netflix’s management expressed satisfaction with the company’s strong financial performance and strategic progress. They highlighted a 16% year-on-year increase in revenue and a 102% rise in EPS, both of which exceeded market expectations. The quarter also saw a significant increase in subscriber numbers, reaching 301.6 million, driven by compelling content, including major releases such as the Jake Paul vs Michael Tyson fight and NFL games.

Management emphasised the importance of continued investment in original content, which has helped boost user engagement and reduce subscriber churn. Additionally, plans were announced to expand Netflix’s proprietary advertising platform to twelve countries, aiming to improve margins and monetisation by reducing reliance on intermediaries. Netflix’s management reiterated its confidence in the company’s strategic direction, highlighting that investment in content and the development of advertising technologies are key drivers of growth and long-term success.

For 2025, Netflix provided guidance indicating continued optimism. The company raised its full-year revenue forecast to approximately 44.00 billion USD – a 0.50 billion USD increase from previous estimates. The operating margin was projected at 29%, one percentage point above earlier expectations. Management also referred to plans for further investment and expansion across gaming, advertising, and live streaming, aiming to enhance the platform’s appeal to subscribers.

Netflix, Inc. Q1 2025 financial results

On 17 April, Netflix released its Q1 2025 report, demonstrating strong financial performance once again. Below is a comparison of its data with the corresponding period in 2024:

- Revenue: 10.54 billion USD (+13%)

- Net income: 2.89 billion USD (+24%)

- Earnings per share: 6.61 USD (+25%)

- Operating income: 3.34 billion USD (+27%)

- Operating margin: 31.7% (+360 basis points)

Netflix demonstrated impressive resilience amid economic challenges, including concerns about US trade policy. The company reported a 13% year-on-year revenue increase to 10.5 billion USD and a rise in net income to 2.9 billion USD. CEO Greg Peters noted that Netflix has historically been a stable company, even during economic downturns, with no significant changes in customer behaviour.

A notable development was Netflix’s strategic shift towards advertising. The ad-supported plan accounted for 55% of new subscriptions in regions where it is available, highlighting the successful development of new revenue streams. The company plans to double its advertising revenues in 2025 through its proprietary ad platform.

For Q2 2025, Netflix projected revenue of 11.04 billion USD, reflecting steady growth driven by increases in both subscriptions and advertising revenue. The company maintained its annual revenue forecast within the 43.5 to 44.5 billion USD range and raised its operating margin target to 29% (up from 28%). These projections emphasise Netflix’s confidence in its strategy and its ability to navigate economic challenges.

In its Q1 2025 earnings commentary, Netflix set an ambitious target to reach a market capitalisation of 1 trillion USD by 2030. Ted Sarandos confirmed that this is not an official forecast or financial guidance. To achieve this target, Netflix planned to double its 2024 revenue of 39 billion USD by 2030, with a primary focus on expanding its advertising segment. The company expected to generate 9 billion USD from global advertising sales by leveraging the growing popularity of its ad-supported subscription tier. Additionally, Netflix invested in its advertising technology platform, launched on 1 April 2025, which is designed to enhance its advertising capabilities and drive further revenue growth.

Netflix’s long-term growth strategy, including the goal of reaching a market capitalisation of 1 trillion USD by 2030, demonstrates its commitment to innovation and considered development.

Netflix, Inc. Q2 2025 financial results

On 17 July, Netflix released its Q2 2025 results, once again exceeding expectations. Below are the key figures compared with the same period in 2024:

- Revenue: 11.08 billion USD (+16%)

- Net income: 3.13 billion USD (+46%)

- Earnings per share: 7.19 USD (+47%)

- Operating income: 3.77 billion USD (+45%)

- Operating margin: 34.1% (+690 basis points)

Netflix delivered strong Q2 2025 results, with revenue rising 16% year-on-year to approximately 11.08 billion USD and a sharp increase in net income and earnings per share of 46−47% to 3.13 billion USD (7.19 USD per share), beating analyst expectations.

Advertising has become a new growth driver for Netflix. The company is actively developing its proprietary advertising platform, Ads Suite, which includes targeting, programmatic buying, and interactive formats. Netflix has confirmed that it expects to double advertising revenue in 2025, a segment that could significantly diversify its income streams. Content has remained a core strength. Although the company no longer discloses subscriber numbers, it reported high user engagement: the third season of Squid Game reached 122 million views, with releases such as Stranger Things and other flagship titles scheduled for the second half of the year. This helped support growth in viewing time and subscriber retention. Additionally, the implementation of AI has contributed to margin expansion. Management expected the full-year operating margin to be around 30%. The use of AI in content production and personalised recommendations has allowed the company to reduce costs and increase engagement.

For Q3 2025, management forecasted revenue of 11.53 billion USD, above the consensus estimate of 11.31 billion USD. Content expenses were forecast to rise in Q3 and particularly in Q4, including costs associated with sports streaming. However, the company still projected margin growth both quarter-on-quarter and year-on-year.

Investor reaction to the Q2 2025 report was mixed. At first glance, the results were strong, with revenue and earnings per share exceeding expectations, and management raising the full-year forecast. However, despite this, shares fell by 5% the day after the report’s release, as a substantial part of the earnings growth was attributed not to operational improvements but to a favourable currency effect – a weakening US dollar.

Moreover, ahead of the report, shares had already risen significantly and were trading at a high premium – approximately 44 to 47 times forward earnings – nearly double the average level over the past three years. This meant the market had already priced in very high expectations. Consequently, following the report, some investors chose to take profits while shares were trading near their historical peak.

Netflix, Inc. Q3 2025 financial results

Netflix released its Q3 2025 results on 21 October. The key figures compared with the same period in 2024 are as follows:

- Revenue: 11.51 billion USD (+17%)

- Net profit: 2.55 billion USD (+8%)

- Earnings per share: 5.87 USD (+9%)

- Operating profit: 3.25 billion USD (+12%)

- Operating margin: 28.2% (–140 bps)

- Free cash flow: 2.66 billion USD (+21%)

Netflix delivered strong revenue growth in Q3 2025 – up 16% year-on-year – in line with the company’s forecasts. However, profit came in slightly below expectations due to one-off expenses of 619 million USD related to a tax dispute in Brazil. The company recognised these costs within cost of revenue, thereby reducing the operating margin by more than five percentage points. Without this factor, the margin would have exceeded the projected 31.5% level. Earnings per share were 5.87 USD – higher than a year earlier (5.40 USD) but approximately 1 USD below Netflix’s internal forecast due to the tax-related charge.

Despite this, the company’s core business indicators remained very strong. Netflix reported record advertising sales and a substantial increase in long-term contracts with US advertisers. Platform viewing share rose to its highest level since late 2022 in both the US and the UK. The company highlighted strong audience interest in content – with KPop Demon Hunters leading the way among films – while live streaming continued to expand, including popular broadcasts of sporting events such as the Canelo vs Crawford fight. Management reported that the advertising business continues to grow rapidly and, according to external estimates, could more than double in 2025.

For Q4 2025, Netflix expected revenue of about 11.96 billion USD, up 17% year-on-year. The operating margin was forecast at around 23.9%, two percentage points higher than in the same quarter of the previous year. For the full year 2025, the company anticipated revenue of approximately 45.1 billion USD, a 16% increase from 2024. The forecast for operating margin was slightly lowered to around 29%, down from the earlier projection of 30%, due to the one-off tax-related costs in Brazil.

Netflix, Inc. Q4 2025 financial results

Netflix released its Q4 2025 results on 20 January 2026. Below are the key figures compared with the same period in 2024:

- Revenue: 12.05 billion USD (+18%)

- Net income: 2.42 billion USD (+29%)

- Earnings per share (EPS): 0.56 USD (+31%)

- Operating income: 2.95 billion USD (+30%)

- Operating margin: 24.5% (+220 bps)

- Free cash flow: 1.87 billion USD (+35%)

For Q4 2025, Netflix delivered strong results, surpassing market expectations for both revenue and earnings per share. Revenue reached 12.05 billion USD, exceeding the analyst consensus estimate of 11.97 billion USD. This was driven by subscriber base growth, which rose by 25 million new subscribers, bringing the total subscriber count to 325 million. This boosted subscription revenue, which continued to grow due to increased demand for content. Net income amounted to 2.42 billion USD, reflecting a 29% year-on-year increase. As a result, earnings per share (EPS) stood at 0.56 USD, also exceeding market expectations of around 0.55 USD.

The sharp decline in earnings per share compared with the previous quarter (from 5.87 to 0.56 USD) was due to a technical factor – on 10 November 2025, Netflix underwent a 10-for-1 stock split. This meant that for each share held by an investor on the record date (10 November 2025), they received nine additional shares, resulting in a tenfold increase in the total number of shares. Consequently, EPS decreased, as the same amount of profit was now spread over a larger number of shares, even though the company’s net income had increased.

The primary driver of Netflix’s growth in the reporting quarter was the increase in paid subscriptions, alongside a sharp rise in advertising revenue. According to the company, advertising revenue grew by more than 2.5 times year-on-year, reinforcing Netflix’s strategy of diversifying its revenue streams.

Management also issued positive guidance for Q1 2026, forecasting revenue of approximately 12.16 billion USD, representing year-on-year growth of around 15%. Earnings per share were projected at 0.76 USD, which was likewise viewed positively by the market. Netflix expects its operating margin in the next quarter to reach 32.1%, confirming continued strong profitability. Compared with the same quarter a year earlier, this improvement suggests that Netflix continues to manage costs effectively despite rising content investment.

Regarding its longer-term guidance, Netflix expects full-year 2026 revenue of 50.7–51.7 billion USD, providing a constructive signal for investors. Moreover, the company projects that advertising revenue will double to 3 billion USD this year, representing a meaningful contribution to future financial performance. This indicates that Netflix continues to expand its advertising model and increasingly views it as a key revenue pillar amid the maturation of the paid subscription market.

Netflix, Inc. Q1 2026 financial results

On 16 April, Netflix reported its Q1 2026 results. The key figures compared with the same period in 2025 are as follows:

- Revenue: 12.25 billion USD (+16%)

- Net income: 5.28 billion USD (+83%)

- Earnings per share (EPS): 1.23 USD (+86%)

- Operating income: 3.96 billion USD (+18%)

- Operating margin: 32.3% (+60 basis points)

- Free cash flow: 5.09 billion USD (+91%)

In Q1 2026, Netflix reported strong financial results, exceeding market expectations for both revenue and earnings. Revenue increased to 12.25 billion USD, while operating profit rose to 3.96 billion USD. Growth was driven by an expanding subscriber base, higher subscription prices, and increased advertising revenue. The company also noted that revenue came in slightly above its own guidance.

However, the sharp increase in net profit and earnings per share was also supported by a one-off item. Netflix stated that diluted EPS of 1.23 USD benefited from a 2.8 billion USD termination fee related to the Warner Bros. transaction. The same factor also contributed to a significant increase in free cash flow, which reached 5.09 billion USD compared with 2.66 billion USD a year earlier. As a result, while the quarter was fundamentally strong, overall profitability was further boosted by this one-off gain.

Netflix also highlighted the continued expansion of its advertising business. The ad-supported subscription plan accounted for more than 60% of all new sign-ups in the markets where it was available, while the number of advertisers exceeded 4,000, representing a 70% year-on-year increase. The company continued to expect advertising revenue of approximately 3 billion USD in 2026, roughly double the level recorded in 2025.

For Q2 2026, Netflix expected revenue of 12.57 billion USD, an operating margin of 32.6%, and earnings per share of 0.78 USD. The company left its full-year 2026 guidance unchanged, continuing to forecast revenue of 50.7–51.7 billion USD and an operating margin of 31.5%. At the same time, free cash flow guidance was raised to 12.5 billion USD from the previous 11 billion USD, primarily due to the same one-off payment related to Warner Bros.

Netflix, Inc. Q2 2026 financial results

On 16 July 2026, Netflix published its financial results for Q2 2026. The key figures are presented below, alongside the corresponding figures for 2025:

- Revenue: 12.56 billion USD (+13%)

- Net profit: 3.40 billion USD (+9%)

- Earnings per share: 0.80 USD (+11%)

- Operating profit: 4.19 billion USD (+11%)

- Operating margin: 33.4% (–70 bps)

- Free cash flow: 1.53 billion USD (–33%)

In Q2 2026, Netflix continued to deliver solid growth across its key financial metrics. Revenue increased to 12.56 billion USD, driven by an expanding subscriber base, higher subscription prices, and continued growth in the advertising business. Double-digit revenue growth was recorded across all regions, while operating profit and earnings per share were slightly above the company's guidance.

However, the results appeared less robust than those of the previous quarter. In Q1, net profit and earnings per share received significant support from a one-off gain of 2.8 billion USD related to compensation for the cancelled Warner Bros. transaction. As this one-off gain was absent in Q2, the results provided a clearer picture of Netflix's underlying business performance.

The operating margin declined from 34.1% to 33.4%, as content amortisation expenses grew faster than revenue. Netflix had previously indicated that much of this increase in content costs would occur during the first half of the year.

Free cash flow declined to 1.53 billion USD from 2.27 billion USD a year earlier. The main reason was higher tax payments, partly related to the compensation received from Warner Bros. in the previous quarter. As a result, the one-off gain boosted both profit and free cash flow in Q1 but led to additional tax payments in Q2.

The advertising business continued to expand and remained one of Netflix's key drivers of future growth. The company continues to expect approximately 3 billion USD in advertising revenue in 2026, roughly double the level of last year. Netflix also expects additional demand from advertisers to be supported by sports broadcasting rights, including NFL games, MLB events, WWE programming, and the FIFA Women's World Cup.

For Q3 2026, Netflix expects revenue of 12.86 billion USD, representing year-on-year growth of approximately 12%, earnings per share of 0.82 USD, and an operating margin of 33.2%, up from 28.2% a year earlier. Full-year 2026 revenue guidance was narrowed from 50.7–51.7 billion USD to 51.0–51.4 billion USD, although the midpoint remained virtually unchanged. Operating margin guidance was also maintained at 31.5%.

Netflix, Inc. key valuation multiples analysis

The table below presents Netflix's key valuation multiples as of the end of Q2 2026, calculated using a stock price of 69 USD.

| Multiple | What it indicates | Value | Comment |

|---|---|---|---|

| P/E (TTM) | Price paid for 1 USD of earnings over the past 12 months | 21.03 | ⬤ Valuation based on earnings has become more reasonable, although TTM earnings were supported by a one-off gain in Q1 2026 |

| P/S (TTM) | Price paid for 1 USD of annual revenue | 5.93 | ⬤ Valuation based on revenue remains high |

| EV/Sales (TTM) | Enterprise value to sales, accounting for debt | 6.04 | ⬤ Despite having virtually no debt, the valuation remains elevated, as investors are pricing in several more years of growth |

| P/FCF (TTM) | Price paid for 1 USD of free cash flow | 25.74 | ⬤ Valuation based on cash flow remains elevated but appears less demanding |

| FCF Yield (TTM) | Free cash flow yield to shareholders | 3.89% | ⬤ Free cash flow yield remains moderate |

| EV/EBITDA (TTM) | Enterprise value to operating profit before depreciation and amortisation | 9.12 | ⬤ Valuation based on EBITDA is moderate, although this metric is less meaningful for Netflix than EBIT |

| EV/EBIT (TTM) | Enterprise value to operating profit | 20.35 | ⬤ Valuation relative to operating profit remains high |

| P/B | Price to book value | 9.52 | ⬤ The premium to book value remains high, although this metric is of limited importance for Netflix |

| Forward P/E | Forward price-to-earnings (P/E) ratio | 19.50 | ⬤ Valuation based on forward earnings appears reasonable, provided earnings growth is sustained |

| Net Debt/EBITDA | Debt burden relative to EBITDA | 0.16 | ⬤ Leverage remains very low |

| Interest Coverage (TTM) | Ability to cover interest expenses with operating profit | 16.94 | ⬤ Interest expense is covered with a comfortable margin |

Based on its valuation multiples, Netflix appears significantly more reasonably valued at a share price of 69 USD than at higher price levels. However, the stock cannot yet be considered inexpensive across all metrics. Its key strengths include very low leverage, strong interest coverage, high operating margins, and robust free cash flow. Its main weaknesses are the elevated valuation based on revenue, EV/Sales, EV/EBIT, and P/B.

For investors with a cautious approach, Netflix remains a high-quality company trading at a premium valuation. The stock could become an attractive investment if the company maintains double-digit revenue growth, an operating margin above 30%, and strong free cash flow.

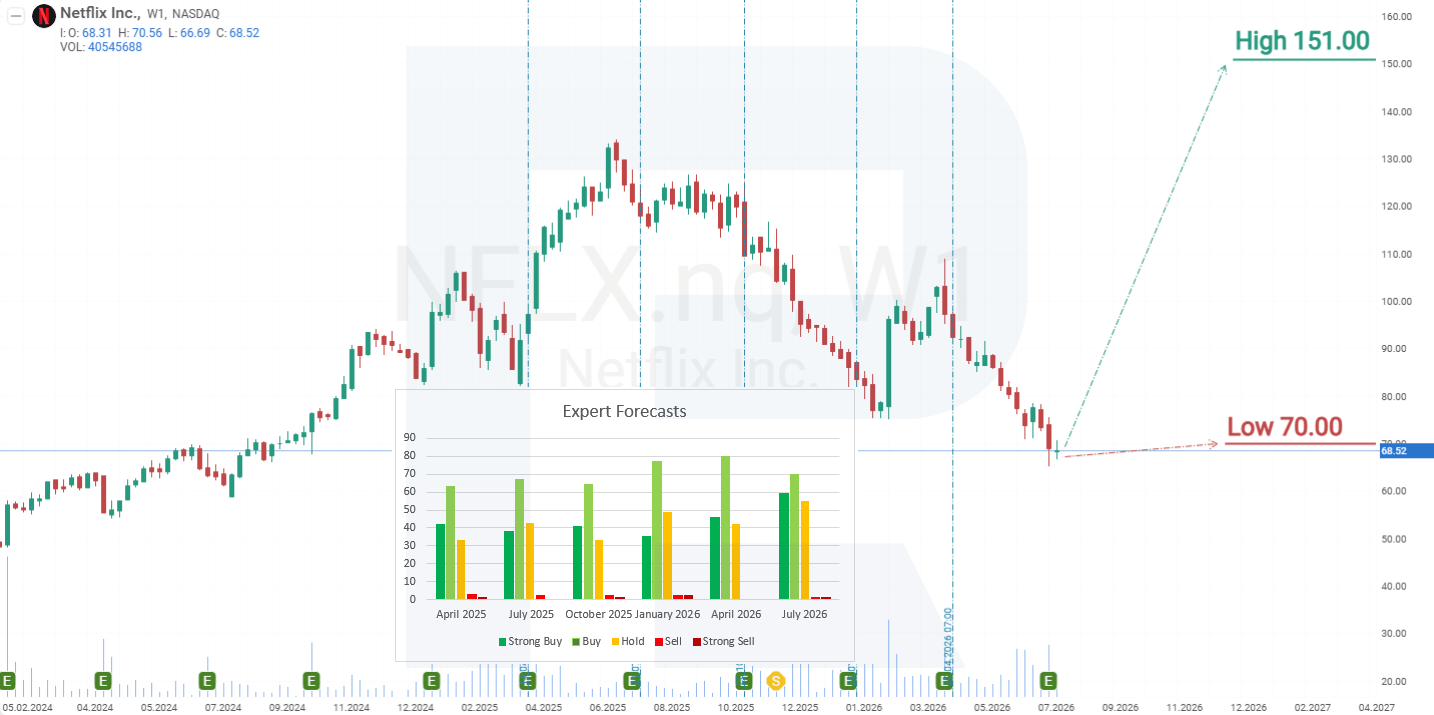

Expert forecasts for Netflix, Inc. stock for 2026

- Barchart: 30 of 49 analysts rate Netflix shares as Strong Buy, 4 as Buy, 14 as Hold, and 1 as Strong Sell. The highest price target is 135 USD, while the lowest is 70 USD.

- MarketBeat: 37 of 55 analysts rate Netflix shares as Buy, 17 as Hold and 1 as Sell. The highest price target is 151 USD, while the lowest is 70 USD.

- TipRanks: 22 of 31 analysts rate Netflix shares as Buy, while 9 rate them as Hold. The highest price target is 135 USD, while the lowest is 70 USD.

- Stock Analysis: 29 of 51 analysts rate Netflix shares as Strong Buy, 7 as Buy, and 15 as Hold. The highest price target is 135 USD, while the lowest is 70 USD.

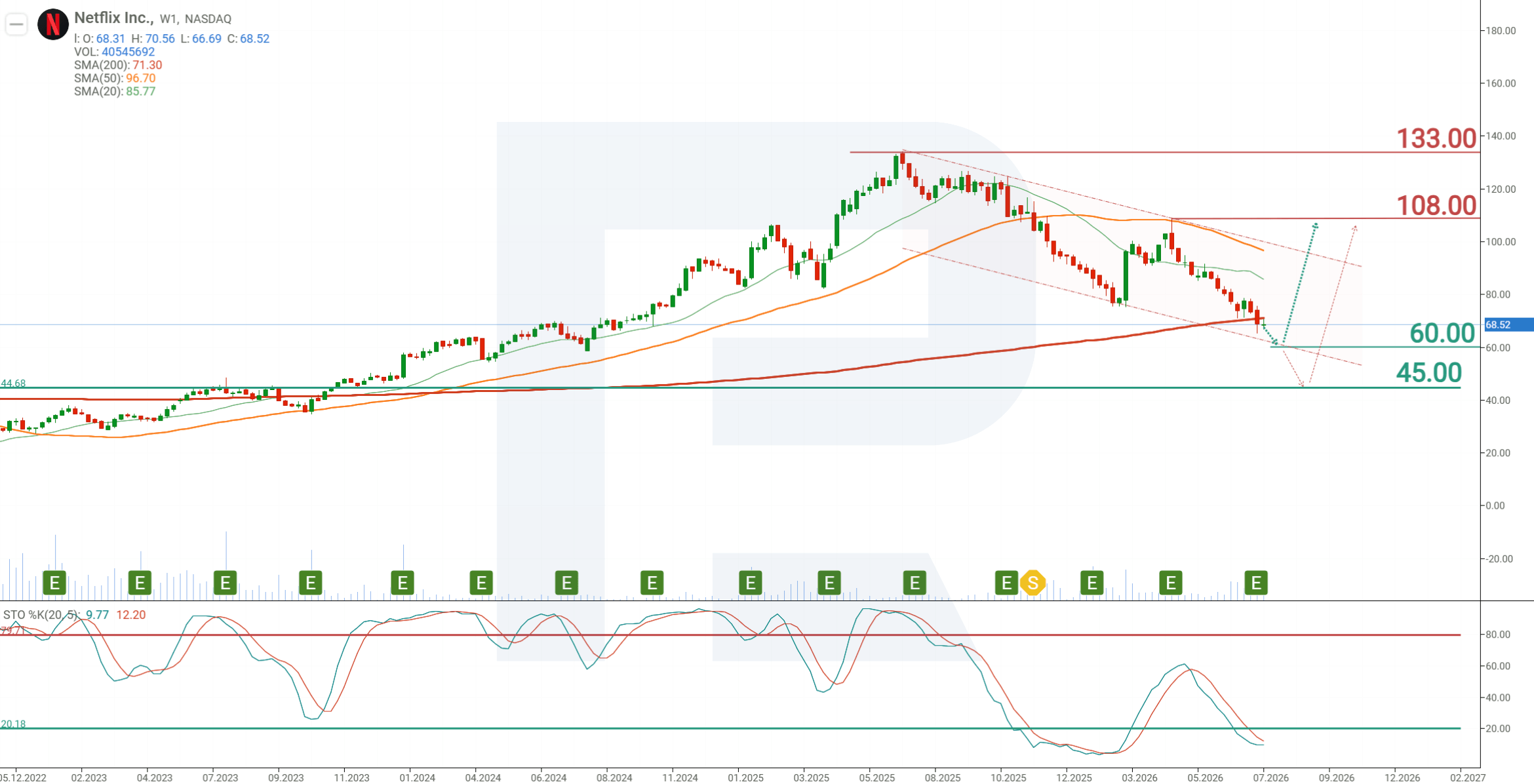

Netflix, Inc. stock price forecast for 2026

On the weekly chart, NFLX shares are trading near the 200-period Moving Average. Given that the previous trend was bullish, the current price action may signal a trend reversal, a transition into a period of consolidation, or a deep correction followed by a rebound from the Moving Average. Meanwhile, the Stochastic indicator is in oversold territory, signalling the potential for a rebound. Based on the current NFLX stock performance, the following scenarios outline the stock's potential movement in 2026.

The base-case forecast for NFLX shares projects a test of support at 60 USD, followed by a rebound and an advance towards resistance at 108 USD.

The alternative forecast for NFLX stock assumes a decline towards support at 45 USD. Buying interest may strengthen at this level, creating the conditions for a gradual recovery. If the stock rebounds from this support, NFLX shares could reach 108 USD by the end of the year.

Risks of investing in Netflix, Inc. stock

Investing in Netflix stock carries risks and potential challenges for the company. These include:

- Content costs: producing high-quality original content requires a significant investment. Inflated costs may impact the company’s profitability.

- Market saturation – subscriber numbers may slow down in countries with high penetration of streaming services.

- User reaction to ads: although users are currently tolerant of ads and subscribing to the ad-supported plan, a shift in user sentiment could significantly harm the company’s financial position.

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex bears no responsibility for trading results based on trading recommendations described in these analytical reviews.