FedEx strengthens its business, but costs continue to weigh on margins

FedEx delivered a strong set of results, confirming the recovery in both revenue and earnings following Q3. However, rising costs continue to weigh on the profitability of its core business. A breakout above resistance at 317 USD could pave the way for FDX shares to advance towards 340 USD and 380 USD.

FedEx Corporation (NYSE: FDX) delivered stronger-than-expected Q4 2026 financial results. Revenue increased to 25.0 billion USD, while non-GAAP EPS reached 6.31 USD. Compared with Q3, the company expanded its business volumes, increased earnings per share, and improved its adjusted operating margin from 6.7% to 8.4%.

The primary weakness remained the profitability of the Federal Express segment. Its adjusted operating margin stood at 8.9%, compared with 9.0% a year earlier, as higher labour, third-party transportation, and fuel costs partially offset the benefits of higher pricing and increased delivery volumes.

Q4 was the final quarter in which the FedEx Freight business was included in the company's consolidated results. Following the separation of this business into an independent company, FedEx will become more dependent on the profitability of its core delivery network, while comparisons with prior reporting periods will become less meaningful.

For the 2026 calendar year, FedEx expects revenue to grow by 11%, with non-GAAP EPS in the range of 16.90–18.10 USD.

The market reaction to the results was mixed. FedEx shares fell to as low as 306 USD, approximately 3.5% below the previous closing price. Investors were concerned by the weaker profitability of the Federal Express segment, rising costs, and uncertainty surrounding the company's performance following the separation of FedEx Freight. However, buyers returned to the market during the second half of the trading session. The shares recovered to close at 316.83 USD. This price action suggests that investors factored in the strong revenue, better-than-expected earnings, and the company's positive outlook, although concerns about profitability continue to limit demand for the stock.

This article examines FedEx Corporation, outlines the sources of its revenue, reviews the company's performance over recent quarters, and discusses expectations for the 2026 financial year. It also provides a technical analysis of FDX shares, forming the basis for the forecast for FedEx stock in the 2026 calendar year.

About FedEx Corporation

FedEx Corporation is an American logistics company founded in 1971 by Frederick Smith. The company provides global express delivery, freight transportation, logistics, and e-commerce services. In 1978, it went public through an IPO on the NYSE, where its stock trades under the ticker FDX.

FedEx holds a leading position in the global logistics and delivery market, though its market share varies by region and delivery segment. Major competitors include Amazon Logistics, DHL, and United Parcel Service, Inc. (NYSE: UPS).

FedEx Corporation’s business model

FedEx’s business model is centred around providing logistics and transportation services, primarily express delivery and freight transportation. The company generates revenue from various business segments, each catering to different client categories: individuals, small and medium-sized enterprises, and large corporations. The main sources of the company’s income are as follows:

- FedEx Express: one of the key segments responsible for the fast delivery of parcels and documents worldwide. Revenue is generated through tariffs based on weight, distance, and delivery speed.

- FedEx Ground: ground delivery of freight and parcels, which is typically slower but more cost-effective than air transportation. This segment is popular among small and medium-sized enterprises, as well as in the e-commerce sector.

- FedEx Freight: this segment transports freight across the US and international routes, with a focus on large and heavy cargo.

- FedEx Services: provides logistics and business solutions, including supply chain management, IT services, and e-commerce support for corporations.

- FedEx Office: offers retail and business services, including document printing, mailbox rentals, and package handling and shipping at service points.

The company reports on two segments – FedEx Express and FedEx Freight – with other divisions categorised under ‘Other Income’.

FedEx Corporation Q1 2025 financial results

On 19 September 2024, FedEx reported disappointing Q1 2025 results for the quarter ended 31 August 2024. Below are the key figures compared to last year’s corresponding period:

- Revenue: 21.60 billion USD (–0.5%)

- Net income: 890 million USD (–26.0%)

- Earnings per share: 3.60 USD (–21.0%)

- Operating margin: 5.20% (–190 basis points)

Revenue by segment:

- FedEx Express: 18.30 billion USD (–1.0%)

- FedEx Freight: 2.32 billion USD (–2.0%)

- Other and eliminations: 945 million USD (+9.0%)

The fundamental analysis of FedEx’s report indicated stagnant revenue despite increased expenses. Transportation costs rose by 5% to 5.27 billion USD, and business optimisation costs increased by 22% to 128 million USD. As a result, net income declined from 1.16 billion to 0.89 billion USD. Analysts’ forecasts were not met: revenue was expected to be 360 million USD higher (21.96 billion USD), and earnings per share were projected at 4.86 USD, above the actual 3.60 USD. Following the report’s release, FedEx stock plunged by over 15%.

If the logistics company shows no revenue growth, this may indicate a slowdown in the US economy. Additional pressure came from a 0.50% interest rate cut by the Federal Reserve, which may suggest the peak of economic growth.

FedEx’s outlook for the fiscal year 2025 was cautious, with revenue expected to rise moderately and the EPS forecast lowered from 18.25–20.25 USD to 17.90–18.90 USD.

FedEx CEO Rajesh Subramaniam noted that the weak results were due to reduced demand for express deliveries, higher operating costs, and a downturn in industrial production. Despite cautious optimism about the second half of 2024, the company maintained a moderate outlook due to economic uncertainty.

FedEx Corporation Q2 2025 financial results

On 19 December 2024, FedEx reported its Q2 2025 financial results, which once again disappointed investors. Below are the main highlights:

- Revenue: 22.00 billion USD (–1.0%)

- Net income: 0.99 billion USD (–1.9%)

- Earnings per share: 4.05 USD (+1.5%)

- Operating margin: 5.60% (+10 basis points)

Revenue by segment:

- FedEx Express: 18.84 billion USD (+0.3%)

- FedEx Freight: 2.18 billion USD (–11.2%)

- Other and eliminations: 949 million USD (+0.9%)

FedEx’s management, commenting on the 1% revenue decline, attributed it to a challenging economic environment, particularly the weakness in the US industrial economy and the expiration of its air freight contract with the US Postal Service (USPS), which ended on 29 September 2024 and had previously generated approximately 2 billion USD in annual revenue. However, there were also positive developments, including a 9% increase in international export parcel volume and cost-saving benefits from the DRIVE program, which resulted in savings of 540 million USD in the last quarter.

The company also highlighted the completion of a one billion USD share buyback. It announced plans to spin off FedEx Freight into a separate publicly traded company within the next 18 months to increase stockholder value.

For Q3 of fiscal year 2025, management expects positive effects from increased DRIVE savings and higher revenue due to the Cyber Week event dedicated to cybersecurity, digital technology, and the IT industry. However, these benefits may be offset by the loss of the USPS contract.

The fiscal 2025 outlook expects revenue to remain approximately the same as last year. The EPS forecast has been adjusted to a range between 19.00 USD and 20.00 USD, down from 20.00 USD to 21.00 USD.

FedEx Corporation Q3 2025 financial results

On 20 March 2025, FedEx reported its Q3 2025 results, which again fell short of investor expectations. Below are the key figures:

- Revenue: 22.20 billion USD (+0.9%)

- Net income: 1.09 billion USD (+12.3%)

- Earnings per share: 4.51 USD (+16.8%)

- Operating margin: 6.70% (+40 basis points)

Revenue by segment:

- FedEx Express: 19.81 billion USD (+2.7%)

- FedEx Freight: 2.08 billion USD (+27.2%)

- Other and eliminations: 890 million USD (+3.3%)

In his commentary on the report, Rajesh Subramaniam noted revenue growth in Q3 compared to the same period last year, marking the first such increase in fiscal year 2025. He stated that FedEx improved profitability despite a particularly challenging operating environment, which included a busy festive season and severe weather conditions. Management also emphasised the success of the DRIVE program, which helped save 600 million USD in costs during the quarter, contributing to a 12% rise in adjusted operating income, which increased to 1.8 billion USD from the previous year.

FedEx’s management expressed cautious optimism regarding its Q4 fiscal year 2025 outlook. The company is expected to continue pursuing its revenue quality strategy and increase cost savings from the DRIVE program. Specifically, it projects closing Q4 FY2025 with annual cost savings exceeding 2.2 billion USD, in line with its target for the full fiscal year 2025.

However, management also anticipates ongoing challenges in the FedEx Freight segment, though these are expected to ease somewhat compared to previous quarters. Revenue in the FedEx Express segment is forecast to remain nearly unchanged, while the FedEx Freight segment is expected to experience a decline in revenue compared to the prior year.

FedEx revised its full fiscal year 2025 forecast downward, now expecting EPS to range from 18.00 USD to 18.60 USD, down from 19.00-20.00 USD. This revision reflects ongoing economic challenges and uncertainty regarding global trade policies under the Donald Trump administration.

FedEx Corporation Q4 2025 financial results

On 24 June 2025, FedEx released its Q4 2025 results, which this time exceeded investor expectations. Key performance indicators are as follows:

- Revenue: 22.21 billion USD (+1%)

- Net profit: 1.46 billion USD (+9%)

- Earnings per share (EPS): 6.07 USD (+12%)

- Operating margin: 9.1% (+160 basis points)

Revenue by Segment:

- FedEx Express: 18.98 billion USD (+1%)

- FedEx Freight: 2.30 billion USD (−4%)

- Other and eliminations: 946 million USD (+2%)

FedEx delivered a solid performance in Q4 FY2025, with adjusted EPS of 6.07 USD on revenue of 22.2 billion USD – both metrics exceeding expectations, despite only modest year-on-year revenue growth.

Instead of issuing full-year guidance, FedEx provided a limited outlook for Q1 FY2026, forecasting revenue growth between 0% and 2% and adjusted EPS in the range of 3.40–4.00 USD. This forecast was below analyst expectations.

There are, however, encouraging signals. The company has already achieved 2.20 billion USD in cost savings through the DRIVE program and expects a further 1.00 billion USD in FY2026, supported by both DRIVE and the Network 2.0 initiative. According to CEO Raj Subramaniam, around 200 million USD of these savings will be realised in the first quarter, with the main impact expected mid-year.

FedEx also continues to return capital generously to shareholders. The annual dividend was increased by 5% to 5.80 USD, and 2.10 billion USD remains under its share buyback program. Cash flow remains strong, with a conversion rate of nearly 90% over the past year.

A potential weakness is management’s decision not to provide full-year guidance, which underlines the ongoing external uncertainty – particularly concerning trade tariffs between the US, China, and Europe. Additional pressure comes from reduced freight volumes from Asia to the US, the expiration of the USPS contract, and continued weakness in the B2B segment. However, FedEx is actively shifting its focus to higher-margin, oversized shipments. It has signed a new rural delivery agreement with Amazon, which may help offset some of the pressure on revenue.

The Q4 FY2025 report demonstrated the company’s resilience in an unstable global environment, with effective cost control adding to investor confidence. In addition, shareholders continue to receive generous payouts. However, the cautious outlook and global risks offer little room for short-term optimism.

For long-term investors, the key question remains whether FedEx can successfully translate its structural reforms and network improvements into profit growth by mid-FY2026. If so, the current share price may represent an attractive entry point.

FedEx Corporation Q1 2026 financial results

On 18 September 2025, FedEx published its Q1 2026 results for the quarter ended 31 August 2025. The key figures are as follows:

- Revenue: 22.24 billion USD (+3% year-on-year)

- Net profit: 0.91 billion USD (+2% year-on-year)

- Earnings per share: 3.83 USD (+6% year-on-year)

- Operating margin: 5.8% (+20 basis points)

Revenue by segment:

- FedEx Express: 19.12 billion USD (+4% year-on-year)

- FedEx Freight: 2.26 billion USD (–3% year-on-year)

- Other and eliminations: 871 million USD (+60% year-on-year)

FedEx delivered Q1 2026 results that exceeded expectations. Revenue reached 22.2 billion USD (+3% year-on-year), adjusted EPS was 3.83 USD (+6% year-on-year), and the non-GAAP operating margin expanded to 5.8% (+20 bps). Consensus had forecast around 21.66 billion USD in revenue and 3.68 USD in EPS.

Among the negative factors in the quarter were trade barriers and tariffs: the removal of the de minimis regime (duty-free import of low-value goods) reduced quarterly revenue by 150 million USD and, according to FedEx, could cost up to around 1 billion USD for the full year. International export volumes fell 3%, while rising wages and transport costs, the expiry of the USPS contract, and a one-off tax expense of 16 million USD further weighed on performance. The FedEx Freight segment also posted weaker operating results.

On the positive side, the domestic US market remained resilient, with average daily parcel volume rising 4% and revenue per parcel increasing 2%. The effects of the ongoing cost-saving program (target: 1 billion USD) supported margins. The company also repurchased 0.5 billion USD worth of shares and ended the quarter with 6.2 billion USD in cash. Additionally, it announced an average tariff increase of 5.9% effective from 5 January 2026 and confirmed the planned spin-off of FedEx Freight into a standalone public company by June 2026.

Management forecasts FY2026 revenue growth of 4–6% and adjusted EPS in the range of 17.20–19.00 USD. Planned targets include capital expenditure of approximately 4.5 billion USD, an effective tax rate of around 25%, and delivery of 1 billion USD in structural cost savings. No quarterly guidance was issued for Q2, but the company expects a moderately strong peak season, characterised by a slight increase in average daily peak volumes and growth in total peak traffic, implying a sequential improvement in Q2 compared to Q1, while risks from international trade remain.

FedEx Corporation Q2 2026 financial results

On 18 December 2025, FedEx presented its Q2 2026 results for the quarter ended 30 November 2025. Below are the key figures:

- Revenue: 22.47 billion USD (+3%)

- Net profit: 1.14 billion USD (+15%)

- Earnings per share: 4.82 USD (+19%)

- Operating margin: 6.9% (+60 basis points)

Revenue by Segment:

- FedEx Express: 20.43 billion USD (+8%)

- FedEx Freight: 2.14 billion USD (–2%)

- Other and eliminations: 897 million USD (–5%)

In Q2 2026 of the fiscal year (ended 30 November 2025), FedEx delivered strong non-GAAP results: revenue amounted to 23.5 billion USD (+7% y/y), net profit – 1.14 billion USD (+15% y/y), earnings per share – 4.82 USD (+19% y/y), and the operating margin rose to 6.9% from 6.3% a year earlier. The company exceeded analysts’ expectations: the market expected EPS of around 4.12 USD and revenue of 22.8 billion USD.

The main growth came from FedEx Express, where both volumes and tariffs increased – average daily parcel volume rose by 5%, and revenue per delivery also improved. As a result, the segment’s operating profit grew significantly, and the margin rose to 7.6% versus 5.6% a year earlier.

The weak spot in the quarter was FedEx Freight, where revenue slightly declined and the margin dropped to 4.2% (compared with 14.3% a year ago) due to one-off expenses related to spin-off preparation (around 152 million USD). Without these costs, the Freight results would have looked stronger.

Management upgraded the full-year 2026 fiscal forecast. The company expected revenue to grow by 5–6% and earnings per share of 17.80–19.00 USD. FedEx also reaffirmed its cost reduction plan of 1 billion USD and capital expenditure of 4.5 billion USD.

FedEx Corporation Q3 2026 financial results

On 19 March 2026, FedEx released its Q3 2026 financial results for the quarter ended 28 February 2026. The key figures are as follows:

- Revenue: 24.00 billion USD (+8%)

- Net income: 1.26 billion USD (+15%)

- Earnings per share: 5.25 USD (+16%)

- Operating margin: 6.7% (–10 basis points)

Revenue by Segment:

- FedEx Express: 21.15 billion USD (+10%)

- FedEx Freight: 1.99 billion USD (–5%)

- Other and eliminations: 855 million USD (–4%)

For Q3 2026, FedEx once again delivered a strong non-GAAP performance. Revenue increased 8% year-on-year, net income rose 16%, and adjusted operating profit reached 1.62 billion USD, up from 1.51 billion USD a year earlier. Although adjusted operating margin edged down slightly to 6.7% from 6.8%, the market responded positively, as FedEx significantly exceeded analyst expectations: consensus estimates were around 23.5 billion USD in revenue and 4.14–4.15 USD in EPS.

The primary driver of the quarter was once again Federal Express. Growth was supported by improved yield in US domestic and International Priority services, as well as higher domestic parcel volumes in the US, resulting in an overall domestic package yield increase of 5%.

FedEx Freight remained the weakest part of the quarter. Segment revenue declined by 5%, GAAP operating profit fell to almost break-even at just 8 million USD, compared with 261 million USD a year earlier, and the margin dropped to 0.4% from 12.5%. The segment remains under pressure due to weak demand, lower shipment volumes, and rising labour costs.

Management upgraded its outlook for the full 2026 financial year. FedEx now expects revenue growth of 6.0–6.5%, up from the previous 5–6% range; adjusted EPS of 19.30–20.10 USD, compared with 17.80–19.00 USD previously; ongoing cost reductions of more than 1 billion USD; and capital expenditure not exceeding 4.1 billion USD, reduced from the prior 4.5 billion USD guidance.

Overall, the report appears strong. FedEx’s core business is currently demonstrating solid growth in both volume and pricing, while the main drag remains the temporary weakness in Freight and costs related to its planned spin-off.

FedEx Corporation Q4 2026 financial results

On 23 June, FedEx Corporation released its Q4 2026 financial results for the quarter ended 31 May. Below are the key figures:

- Revenue: 25.01 billion USD (+13%)

- Net income (non-GAAP): 1.53 billion USD (+5%)

- Earnings per share (non-GAAP): 6.31 USD (+4%)

- Operating margin (non-GAAP): 8.4% (–70 basis points)

Revenue by segment:

- FedEx Express: 21.57 billion USD (+14%)

- FedEx Freight: 2.41 billion USD (+5%)

- Other and eliminations: 1.03 billion USD (+9%)

FedEx delivered strong financial results in Q4 2026, particularly in terms of revenue and earnings, although profitability was weaker. Revenue increased to 25.0 billion USD, exceeding market expectations of approximately 24.0 billion USD, while adjusted earnings per share reached 6.31 USD, compared with consensus estimates of around 5.96 USD.

Revenue increased to 25.0 billion USD, exceeding market expectations of approximately 24.0 billion USD, while adjusted earnings per share reached 6.31 USD, compared with consensus estimates of around 5.96 USD.

Compared with Q3, the company also showed a notable improvement. In the previous quarter, revenue totalled 24.0 billion USD, non-GAAP EPS was 5.25 USD, and the adjusted operating margin stood at 6.7%. In Q4, business volumes increased, earnings per share improved, and the adjusted operating margin recovered to 8.4%. This confirms that higher delivery rates, increased parcel volumes, and the company's cost-reduction program continue to support FedEx's results.

The Federal Express segment's profitability remained the main weakness in the report. The GAAP operating margin declined to 7.7%, compared with 8.4% a year earlier, while the adjusted operating margin was broadly unchanged at 8.9%, compared with 9.0%. Following the separation of FedEx Freight, the company's operations are now almost entirely focused on its delivery business. As a result, investors are paying particularly close attention to whether FedEx can continue to improve the profitability of this core segment.

The report also marked the final set of results before the full transition to the new business structure. On 1 June, FedEx completed the separation of FedEx Freight into an independent publicly listed company. In Q4, the Freight results were still included in the consolidated financial statements, meaning future results will be less comparable with previous quarters. At the same time, the separation is expected to simplify the business structure and allow management to focus on improving the efficiency of the core delivery network.

Due to the change in the company's financial year-end, FedEx provided guidance for the 2026 calendar year. The company expects revenue growth of 11% and adjusted earnings per share in the range of 16.90–18.10 USD. Capital expenditure is expected to total 3.9 billion USD, with the primary focus on network modernisation, automation, and operational efficiency.

Overall, Q4 confirmed the improvement in FedEx's performance following a strong Q3. Revenue and earnings exceeded expectations, while the company's cost-reduction program continues to deliver results. However, the decline in margins showed that rising costs continue to limit the benefits of higher volumes and pricing. Following the separation of FedEx Freight, the key question for investors will be whether the restructured FedEx can improve the profitability of its core business and continue to increase free cash flow.

Expert forecasts for FedEx Corporation stock

- Barchart: 17 out of 27 analysts assigned a Strong Buy rating, 2 assigned a Moderate Buy rating, 7 rated the shares as Hold, and 1 assigned a Sell rating. The upper price target is 479 USD, and the lower bound is 160 USD.

- MarketBeat: 18 out of 29 analysts assigned a Buy rating, 9 recommended Hold, and 2 recommended Sell. The upper price target is 479 USD, and the lower bound is 155 USD.

- TipRanks: 13 out of 16 analysts assigned a Buy rating, 2 recommended Hold, and 1 recommended Sell. The upper price target is 460 USD, and the lower bound is 160 USD

- Stock Analysis: 15 out of 28 analysts assigned a Strong Buy rating, 3 assigned a Buy rating, 8 rated the shares as Hold, 1 assigned a Sell rating, and 1 assigned a Strong Sell rating. The upper price target is 442 USD, and the lower bound is 160 USD.

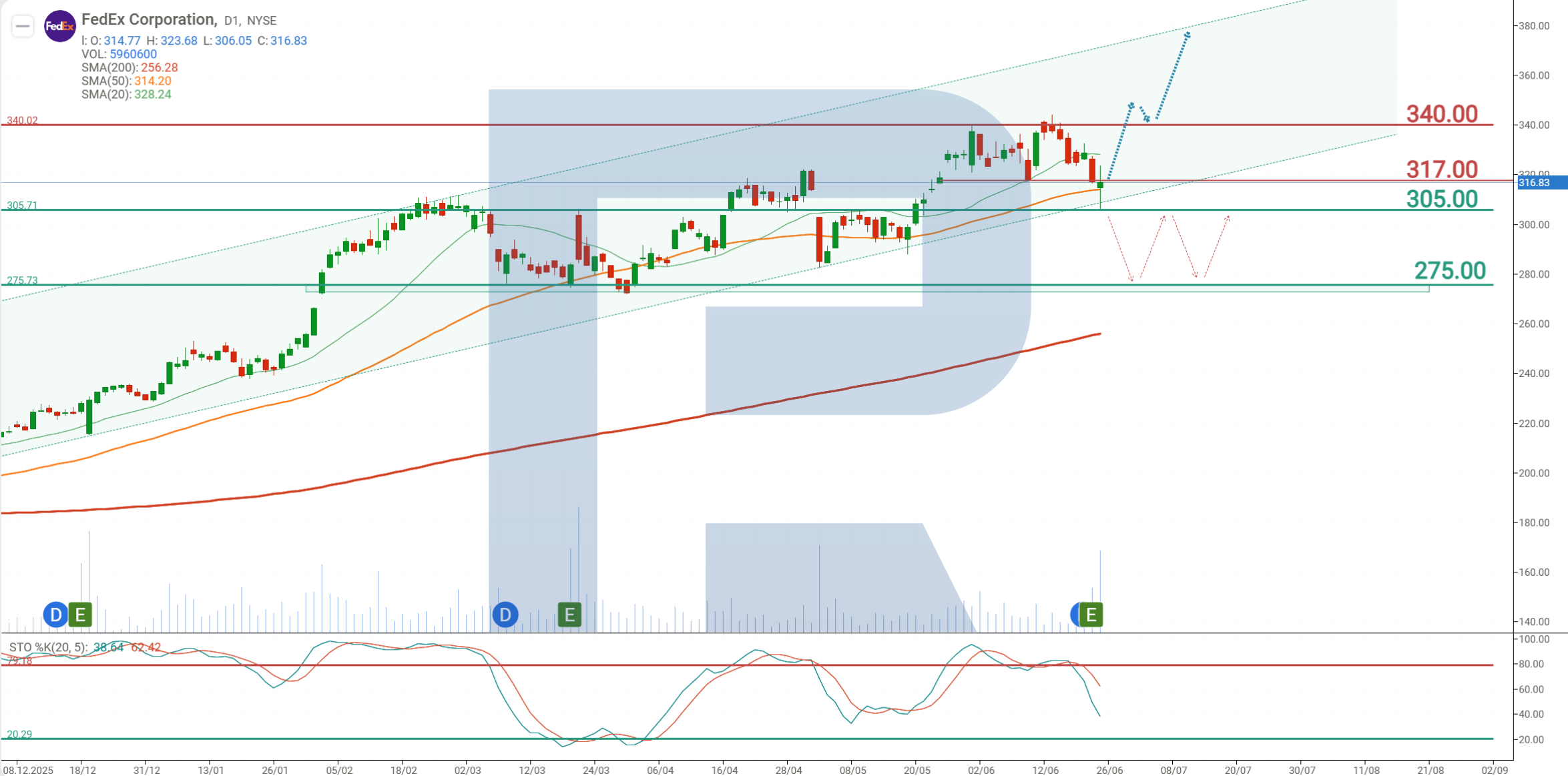

FedEx Corporation stock price forecast for 2026

On the daily chart, FedEx shares are trading above the 200-period moving average, indicating that the long-term uptrend remains intact. The Stochastic indicator is currently between the 20 and 80 levels, suggesting that the shares retain the potential for further gains following the 8% pullback from their all-time high. Based on the current price structure of FedEx shares, the potential scenarios for the second half of 2026 are as follows.

The primary forecast for FedEx shares assumes a breakout above resistance at 317 USD, followed by an advance towards 340 USD. The upward move is expected to unfold within the existing ascending channel. A breakout above resistance at 340 USD could act as a catalyst for a further advance towards the upper boundary of the channel near 380 USD.

The alternative forecast for FedEx stock assumes a break below support at 305 USD. In this scenario, FDX shares could decline towards 275 USD.

Risks of investing in FedEx Corp stock

When investing in FedEx shares, it is important to consider the risks the company may face. The key factors that could negatively affect FedEx's revenue are outlined below:

- Declining profitability in the core business: the Federal Express segment's margin came under pressure due to higher labour, third-party transportation, and fuel costs. Following the separation of FedEx Freight, the core delivery business will become the main driver of the company's financial performance. Any further deterioration in its profitability could weigh on earnings and the share price.

- Risks following the separation of FedEx Freight: on 1 June 2026, FedEx Freight became an independent publicly listed company. While FedEx now has a simpler business structure, it has also lost a separate profitable business and become more dependent on the parcel and express delivery market. Investors will also need time to assess the restructured company's performance without the Freight business, as comparisons with prior reporting periods will become less meaningful.

- Rising operating costs: FedEx's results remain sensitive to fuel prices, labour costs, and third-party transportation rates. The company partially passes these costs on to customers through higher prices and fuel surcharges. However, excessively rapid price increases could reduce shipping volumes or encourage customers to switch to competitors.

- Intense competition and economic sensitivity: FedEx competes with UPS, DHL, Amazon, and regional carriers. At the same time, demand for delivery services depends on consumer spending, industrial production, and global trade. An economic slowdown could reduce shipping volumes, particularly in the higher-margin corporate and international segments.

Overall, the key challenge for FedEx at this stage is improving its margins following the separation of FedEx Freight. Revenue and earnings exceeded expectations in Q4, but the decline in the profitability of the core business triggered a negative market reaction. For FedEx shares to sustain further gains, the company must demonstrate that its cost-reduction efforts and revised business structure are translating into higher earnings and stronger free cash flow.

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex bears no responsibility for trading results based on trading recommendations described in these analytical reviews.