Is buying NVIDIA near its historic high a good investment? NVDA Stock Forecast for 2026

The AI boom continues to drive NVIDIA’s performance: the company reported revenue of 68.13 billion USD and a gross margin of 75.2% for Q4 2026. With strong cash flow and active share buybacks, the stock maintains long-term potential. However, a short-term correction to 150 USD remains possible.

NVIDIA Corporation reported record performance in Q4 2026, driven by the AI infrastructure boom, with revenue reaching 68.13 billion USD, a 73% increase compared to last year. Adjusted earnings per share came in at 1.62 USD, exceeding analyst expectations.

The key growth driver was the data centre segment, which posted revenue of 62.31 billion USD. The non-GAAP gross margin was 75.2%, indicating that the business is generating significant profits and maintaining very high profitability, even with large sales volumes.

Management is betting on the global push to build what are known as AI factories, with demand shifting towards inference – the mass usage of pre-trained models. This means demand will increase not only for GPUs but also for network solutions and data centre infrastructure.

The outlook for the next quarter is set at 78 billion USD in revenue, significantly exceeding market expectations.

This article examines NVIDIA Corporation, detailing its revenue sources, quarterly performance, and expectations for the next quarter. It also provides a stock forecast for NVIDIA for the 2026 calendar year.

About NVIDIA Corporation

NVIDIA Corporation is a US tech company established in 1993 by Jensen Huang, Chris Malachowsky, and Curtis Priem. Jensen Huang has remained the company’s CEO since its foundation. NVIDIA specialises in producing GPUs, chips for AI, data centres, and autopilot systems. The company plays a key role in developing gaming, professional visualisation, and AI computing. NVIDIA also held a prominent place in the cryptocurrency mining industry as its graphics cards were widely used for mining Bitcoin, Ethereum, and other digital assets. The company went public on 22 January 1999 on the NASDAQ under the NVDA ticker symbol.

NVIDIA Corporation’s main revenue streams

NVIDIA is primarily known for its GPUs, but it has recently expanded into the AI segment, dominating the market with high-performance chips used for AI technology development. The company reports revenues from this segment under the Data Center section. NVIDIA’s business model focuses on several key areas:

- GPUs: this includes the Gaming and Professional Visualization segments. The company supplies the gaming industry with GPUs for gaming PCs, consoles, and other devices, ensuring high-performance gaming experiences. Professional Visualization includes GPU sales for professionals involved in 3D graphics, CAD, animation, video editing, and other tasks that require high computing power.

- Data Center: this is one of NVIDIA’s fastest-growing segments. The company develops GPUs and other hardware solutions for data centres, which are used in AI infrastructure, deep learning technologies, cloud computing, and big data processing.

- Automotive segment: NVIDIA is actively developing products for the automotive sector, including self-driving platforms and advanced driver-assistance systems (ADAS).

- OEM and Others: this category includes earnings from technology licensing, sales of other chips and solutions to OEM manufacturers, such as laptop and other electronic device producers.

NVIDIA diversifies its operations, covering various segments, including gaming, data centres, and automotive components. The company publishes statistics on the Gaming, Data Center, Professional Visualization, and Automotive segments in its quarterly reports, while other indicators are included in the Other Revenues section.

NVIDIA Corporation Q2 2025 financial results

On 28 August 2024, NVIDIA released its earnings report for Q2 2025 of the financial year ended on 28 July 2024. Below are the key figures compared to the corresponding period of last year:

- Revenue: 30.04 billion USD (+122%)

- Net income: 16.95 billion USD (+152%)

- Earnings per share: 0.68 USD (+152%)

- Operating profit: 19.94 billion USD (+156%)

- Gross margin: 75.1% (+500 basis points)

Revenue by segment:

- Data Center: 26.27 billion USD (+154%)

- Gaming: 2.88 billion USD (+16%)

- Professional Visualization: 454 million USD (+20%)

- Automotive: 346 million USD (+37%)

In the first half of 2024, NVIDIA returned 15.40 billion USD to shareholders through share repurchases and dividends. As of the end of Q2 2024, the company had 7.50 billion USD remaining for stock buybacks. On 26 August 2024, the Board of Directors approved an additional 50.00 billion USD for share repurchases, with no expiration date.

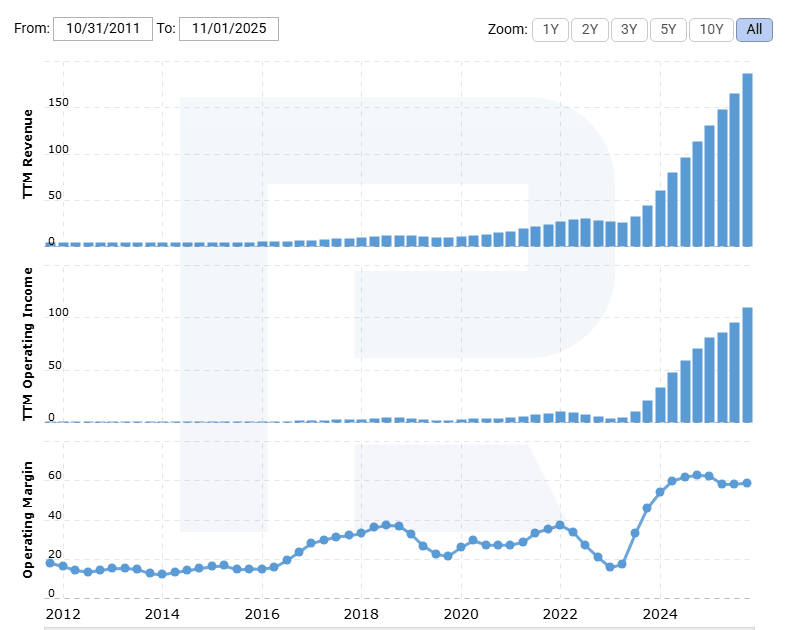

Although the Q2 fiscal 2025 results surpassed analyst forecasts, NVIDIA shares fell immediately after the release. Investors were not particularly impressed by the revenue and profit growth, as financial indicators had surged from 200% to 700% in the previous quarter. Maintaining such rapid growth over the long term is clearly unrealistic, but investor expectations remain elevated.

A fundamental analysis of NVIDIA’s report showed that revenue increased across all segments. The Data Center segment, which focuses on AI technologies, remained the leader. The company’s operating margin chart below illustrates the extent to which AI has influenced NVIDIA’s performance.

OpenAI announced ChatGPT on 30 November 2022, and by Q1 2023, NVIDIA reported an increase in its operating margin. It then grew at a rapid pace, even surpassing the levels seen during the cryptocurrency mining boom. In fact, this suggests that the company has been raising product prices without a decline in demand, allowing it to generate more than 50 cents in profit for every dollar invested.

NVIDIA Corporation Q3 2025 financial results

On 20 November 2024, NVIDIA released its earnings report for Q3 2025 of the financial year ended on 27 October 2024. Below are the key figures compared with the corresponding period of last year:

- Revenue: 35.08 billion USD (+94%)

- Net income: 19.31 billion USD (+109%)

- Earnings per share: 0.78 USD (+111%)

- Operating profit: 21.86 billion USD (+110%)

- Gross margin: 74.6% (+60 basis points)

Revenue by segment:

- Data Center: 30.77 billion USD (+112%)

- Gaming: 3.27 billion USD (+15%)

- Professional Visualization: 486 million USD (+17%)

- Automotive: 449 million USD (+72%)

Jensen Huang commented on the report, saying that “The age of artificial intelligence is in full steam, driving a global shift to NVIDIA computing,” emphasising the strong demand for the Hopper and Blackwell microarchitecture products, which drove record results in the last quarter.

For Q4 of the 2025 financial year, NVIDIA forecasted revenue of 37.50 billion USD (with a potential deviation of 2%) and a non-GAAP gross margin of 73.5%, reflecting confidence in continued growth despite supply restraints, particularly with the ramp-up of Blackwell production.

NVIDIA Corporation Q4 2025 financial results

On 26 February 2024, NVIDIA published its earnings report for Q4 2025 of the financial year ended on 26 January 2025. Below are the key figures compared with the corresponding period of last year:

- Revenue: 39.33 billion USD (+78%)

- Net income: 22.09 billion USD (+80%)

- Earnings per share: 0.89 USD (+82%)

- Operating profit: 24.03 billion USD (+77%)

- Gross margin: 73.0% (+300 basis points)

Revenue by segment:

- Data Center: 35.58 billion USD (+93%)

- Gaming: 2.54 billion USD (–11%)

- Professional Visualization: 511 million USD (+10%)

- Automotive: 570 million USD (+103%)

Jensen Huang commented on the Q4 fiscal 2025 earnings report, saying that “artificial intelligence has been developing at an incredible pace, as agentic AI and physical AI are creating the basis for the next AI wave, which will revolutionise the largest industries”, underscoring the company’s key role in the AI boom, which led to record revenues of 39.30 billion USD. He highlighted the strong results of the Data Center segment, which reached 35.60 billion USD, thanks to demand for the Hopper and Blackwell microarchitecture solutions.

For Q1 fiscal 2026, NVIDIA had projected revenue of 43.00 billion USD (with a possible variance of 2%) and a non-GAAP gross margin of 71.0%, indicating the company’s revenue remained robust. However, the decline in gross margin raised concerns among investors.

NVIDIA Corporation Q1 2026 financial results

On 28 May 2025, NVIDIA released its report for Q1 2026 of the financial year ended on 27 April 2025. Below are the key figures compared with the corresponding period last year:

- Revenue: 44.06 billion USD (+69%)

- Net income: 18.78 billion USD (+26%)

- Earnings per share: 0.76 USD (+27%)

- Operating profit: 21.63 billion USD (+28%)

- Gross margin: 60.5% (–1,790 basis points)

Revenue by segment:

- Data Center: 39.11 billion USD (+73%)

- Gaming: 3.76 billion USD (+42%)

- Professional Visualization: 509 million USD (+20%)

- Automotive: 567 million USD (+72%)

NVIDIA’s Q1 fiscal 2026 report reinforced the company’s leading position in the global AI race despite serious geopolitical and regulatory obstacles. It was a record-breaking quarter, with revenue reaching 44.06 billion USD, up 69% year-on-year. Growth was primarily driven by continued high demand for accelerated computing and AI infrastructure. The Data Center segment, which includes sales of high-performance GPUs to large cloud providers and corporate clients, generated 39.1 billion USD, up 73% from the previous year.

However, the quarter also saw serious challenges. One of the key negative factors was the US government’s restrictions on the export of advanced AI chips to China. Jensen Huang commented on this situation during a conference call, noting that despite persistent strong demand from China, the company was unable to meet it due to regulatory constraints. As a result, NVIDIA wrote off inventory worth 4.5 billion USD, primarily related to H20 chips intended for the Chinese market, and estimated lost revenue for the quarter at approximately 2.5 billion USD. For Q2 fiscal 2026, the company had projected a revenue loss of 8 billion USD due to the restrictions.

Huang also expressed concerns about the broader fallout from these trade restrictions, warning that the ban on advanced AI technology exports could have inadvertently accelerated the development of China’s domestic semiconductor industry, which might ultimately have undermined US global technological leadership. Huang also emphasised that revenue from China accounted for a smaller part of NVIDIA’s total sales at the time, with losses offset mainly by growing demand in North America, Europe, and newly emerging markets, including the Middle East.

For Q2 fiscal 2026, NVIDIA had expected revenue of approximately 45 billion USD. This forecast reflected the active rollout of the new Blackwell chip architecture, which, according to Huang, was already experiencing unprecedented demand from hyperscalers, government AI development programs, and major corporate clients. The company anticipated that strong demand for hardware solutions and AI software products would persist through the end of the fiscal year.

However, despite continued technological leadership and robust demand for AI solutions, NVIDIA faced signs of a slowdown in its key Data Center segment. Although revenue rose 73% year-on-year, the segment fell short of market expectations, which constrained the stock’s growth following the report’s release. This may have indicated the start of a normalisation phase after the rapid acceleration driven by the AI boom.

Nevertheless, the company continued to demonstrate exceptional financial performance and remained at the forefront of technological innovation. Losses related to export restrictions on China were severe but were offset mainly by global demand and the rollout of the next-generation Blackwell architecture. NVIDIA’s strategy to diversify its client base and actively expand into regions with rising AI initiatives forms a strong foundation for sustainable growth in fiscal 2026 and beyond.

NVIDIA Corporation Q2 2026 financial results

On 27 August 2025, NVIDIA released its Q2 2026 financial results for the quarter ended 27 July 2025. Key figures compared with the same period last year are as follows:

- Revenue: 46.74 billion USD (+56%)

- Net income: 26.42 billion USD (+59%)

- Earnings per share (non-GAAP): 1.05 USD (+56%)

- Operating profit: 30.16 billion USD (+30%)

- Gross margin: 72.7% (–300 bps)

Revenue by segment:

- Data Center: 41.09 billion USD (+56%)

- Gaming: 4.28 billion USD (+48%)

- Professional Visualization: 601 million USD (+32%)

- Automotive: 586 million USD (+69%)

- OEM & Other: 173 million USD (+97%)

NVIDIA reported strong results for Q2 2026. Revenue reached 46.7 billion USD (+6% q/q, +56% y/y). The main driver was the data centre segment, which posted 41.1 billion USD (+5% q/q, +56% y/y), with growth supported by Blackwell chip shipments (the Blackwell Data Center subsegment rose 17% sequentially). Gross margin was 72.4% GAAP and 72.7% non-GAAP. Adjusted earnings per share (non-GAAP EPS) came in at 1.05 USD. However, this included a one-time positive effect from the release of a previously established 180 million USD reserve related to H20 chip deliveries to China. Excluding this one-off, EPS would have been 1.04 USD. Gaming revenue increased to 4.3 billion USD, Professional Visualization reached 601 million USD, and Automotive was 586 million USD.

The company emphasised that there were no H20 chip sales to China during the quarter, and forecasts for the next period also exclude these sales. The board approved an increase in the share repurchase program by a further 60 billion USD. The dividend was set at 0.01 USD per share, with a record date of 11 September 2025 and a payment date of 2 October 2025.

The outlook for Q3 2026 projected revenue of approximately 54.0 billion USD (±2%), a non-GAAP gross margin of around 73.5% (±50 bps), non-GAAP operating expenses of roughly 4.2 billion USD, other income around 500 million USD, and an effective tax rate of roughly 16.5% (±1 pp). The company expected to close the financial year with a non-GAAP margin of around 73.5%. It is important to note that this forecast did not factor in potential H20 chip sales to China. For investors, this meant that management’s base-case scenario was built solely on current global demand and the acceleration of new Blackwell chip shipments, without assuming a recovery in the Chinese market.

NVIDIA Corporation Q3 2026 financial results

On 19 November 2025, NVIDIA published its Q3 2026 results for the financial year ended on 26 October 2025. The key figures, compared with the same period in the previous year, are as follows:

- Revenue: 57.01 billion USD (+62%)

- Net income (non-GAAP): 31.76 billion USD (+59%)

- Earnings per share (non-GAAP): 1.30 USD (+60%)

- Operating profit (non-GAAP): 37.75 billion USD (+62%)

- Gross margin (non-GAAP): 73.6% (–140 bps)

Revenue by segment:

- Data Center: 51.22 billion USD (+66%)

- Gaming: 4.27 billion USD (+30%)

- Professional Visualization: 760 million USD (+56%)

- Automotive: 592 million USD (+32%)

- OEM & Other: 174 million USD (+79%)

NVIDIA’s Q3 FY2026 results came in ahead of market expectations. Revenue reached approximately 57 billion USD, and non-GAAP EPS was 1.30 USD – both exceeding analyst forecasts. The company once again delivered strong growth in both revenue and profit.

The primary source of income remains the Data Centre segment, which generated 51.2 billion USD, up 66% year-on-year and accounting for nearly 90% of total revenue. Other segments, including Gaming, continue to grow at a slower pace and make up a smaller share of the total.

Management issued a strong outlook for Q4 FY2026, forecasting revenue of around 65 billion USD and a gross margin of approximately 75% – also above analyst expectations. According to management, NVIDIA has already secured confirmed orders for its new Blackwell and Rubin chips worth around 500 billion USD through the end of 2026, with demand for AI hardware continuing to exceed supply.

Management also emphasised that the current growth does not appear to be a bubble: clients continue to invest heavily in infrastructure, while production capacity remains a limiting factor. However, analysts caution that growth rates may eventually slow due to power-supply constraints and market saturation. For now, based on the Q3 results and guidance for the next quarter, demand for NVIDIA’s products remains extremely strong.

NVIDIA Corporation Q4 2026 financial results

On 19 November 2025, NVIDIA released its Q3 2026 results for the quarter ended 26 October 2025. Below are the key figures compared to the same period last year:

- Revenue: 68.13 billion USD (+73%)

- Net income (non-GAAP): 39.55 billion USD (+79%)

- Earnings per share (non-GAAP): 1.62 USD (+82%)

- Operating profit (non-GAAP): 46.11 billion USD (+81%)

- Gross margin (non-GAAP): 75.2% (+220 basis points)

Revenue by segment:

- Data Center: 62.31 billion USD (+75%)

- Gaming: 3.73 billion USD (+47%)

- Professional Visualization: 1.32 billion USD (+159%)

- Automotive: 604 million USD (+6%)

- OEM & Other: 161 million USD (+28%)

NVIDIA reported a very strong Q4 2026 result, surpassing market expectations, although investors typically expect even more acceleration from a company of this calibre. Revenue reached 68.13 billion USD (+73% YoY and +20% QoQ), with adjusted earnings per share (EPS) coming in at 1.62 USD, exceeding the consensus estimate of 1.53 USD.

The primary growth driver for the quarter, as in previous periods, was the data centre segment. Revenue in this area reached 62.31 billion USD (+75% YoY and +22% QoQ), driven by both computing and networking.

In terms of profitability, the quarter was exceptionally strong: gross margin increased to 75.0% (GAAP) and 75.2% (non-GAAP), while net income under GAAP totalled 43.0 billion USD, with GAAP EPS of 1.76 USD. In the 2026 financial year, NVIDIA returned 41.1 billion USD to shareholders through buybacks and dividends, while maintaining a significant buyback program balance of 58.5 billion USD.

The outlook for the next quarter is also strong. For Q1 2027, the company forecasts revenue of approximately 78.0 billion USD, significantly exceeding analyst expectations (the average estimate being around 72.6 billion USD). NVIDIA specifically noted that the forecast excludes revenue from Data Centre compute in China. The company also mentioned that it had received licences to ship small volumes of H200 to China. However, this does not alter the overall picture, as growth is driven by global demand outside China.

Analysis of insider Activity in NVIDIA Corporation shares

The analysis of insider activity in NVIDIA shares for 2025 and early 2026 provides key insights into the company’s management strategy. Over the past 12 months, NVIDIA insiders have employed one of the most aggressive profit-taking strategies in the tech sector. Share sales in 2025, exceeding 1.5 billion USD, resulted from the implementation of long-term 10b5-1 plans. This indicates that the company’s management views the period from 2025 to 2026 as a “liquidity window,” during which the sale of large share packages is unlikely to impact stock prices negatively. The sales by Huang Jen Sun and Stevens Mark at peak market capitalisation levels (above 4 trillion USD) suggest an effort to reduce the risk of capital concentration in a single asset by converting paper gains into real money.

The sales are categorised into several types of transactions. First, automatic sales related to tax payments (Tax/RSU) are a technical necessity and do not send a negative signal. For instance, regular sales by Kress Colette (CFO) and Donald F. Robertson for tax payments account for only a small percentage of the total volume. These transactions are not expected to have a significant long-term impact on the market. However, discretionary sales, such as those through Stevens Mark’s trusts for hundreds of millions of dollars in 2025, represent a conscious exit from the asset. Tax-related sales account for only around 15–20% of total sales, confirming that most transactions involve the voluntary liquidation of positions. This suggests that management considers the current stock price fair, or even ahead of its time.

The absence of insider share purchases in 2025 and early 2026 is a significant indicator. The last notable purchase occurred at the end of 2020, suggesting that the company’s insiders do not see current prices, even after local corrections, as offering high-margin-of-safety investment opportunities. While this does not imply that the company is underperforming, it signals that the market has already priced in the potential for explosive growth.

In January and February 2026, insider sales activity decreased by 50% compared to the average levels of 2025. This slowdown in activity may indicate that the main asset liquidation plans have already been completed, or that insiders are awaiting a new catalyst, such as the Rubin architecture report, which could drive stock prices even higher, prompting them to hold on to their remaining shares.

Overall, insider behaviour in NVIDIA is moderately bearish in the short term but remains neutral in the long term. The fact that Huang Jen Sun continues to hold over 3% of the company offsets the impact of his 800 million USD in sales. However, the absence of purchases and the large-scale liquidation of director positions in 2025 suggest that NVIDIA’s phase of the easiest and fastest growth has come to an end. The company has entered the stage of a mature giant, where growth is likely to be steadier and more measured.

Analysis of key valuation multiples for NVIDIA Corporation

Below are the key valuation multiples for NVIDIA based on Q4 2026 financial results, calculated using a share price of 185 USD (for the calculation of multiples, key non-GAAP metrics have been used, adjusted for one-off acquisition costs, stock-based compensation, and tax recalculations).

| Multiple | What it indicates | Value | Commentary |

|---|---|---|---|

| P/E (TTM) | The price of 1 USD of earnings over the past 12 months | 49.4 | ⬤ For a company with over 100% profit growth, this is a moderate figure. |

| P/S (TTM) | The price of 1 USD of annual revenue | 30.5 | ⬤ Extremely high value. The market expects infinite dominance in AI. |

| EV/Sales (TTM) | Enterprise value to revenue, including debt | 30.3 | ⬤ Excessively high valuation relative to sales volume, even with the large cash reserves on hand. |

| P/FCF (TTM) | The price of 1 USD of free cash flow | 53.5 | ⬤ NVIDIA is generating cash at phenomenal rates. |

| FCF Yield (TTM) | Free cash flow yield for shareholders | 1.9% | ⬤ Low yield – but for a growth stock, this is an excellent result. |

| EV/EBITDA (TTM) | Enterprise value to EBITDA | 38.8 | ⬤ Excellent. Reflects immense operational efficiency. |

| EV/EBIT (TTM) | Enterprise value to operating profit | 41.2 | ⬤ Confirms that the primary profit comes from core operations, not one-off factors. |

| P/B | Price to book value | 58.2 | ⬤ Huge disparity between market price and book value of assets. Typical for chipmakers without their own factories. |

| Forward P/E | Forward price-to-earnings (P/E) ratio | 32.8 | ⬤ Based on forecasts for the 2027 financial year, the stock looks attractive. |

| Net Debt/EBITDA | Debt load relative to EBITDA | -0.25 | ⬤ Negative net debt. |

| Interest Coverage (TTM) | Operating profit to interest expense ratio | >100 | ⬤ Interest expenses are negligible compared to operating income. |

Analysis of NVIDIA’s valuation multiples – conclusion

From a financial standpoint, NVIDIA remains exceptionally strong. The company generates substantial profits, producing a cash flow of around 77 billion USD over the past twelve months, maintains a net cash position, and comfortably services all its debt – indicating a genuinely high-quality business.

However, the current market valuation is extremely high. Nearly all key multiples (P/S, EV/Sales, EV/EBIT, and P/FCF) are at levels typically seen only during rapid-growth phases. This means the share price is justified only if the company can sustain robust revenue and profit growth in the Data Centre segment for several more years.

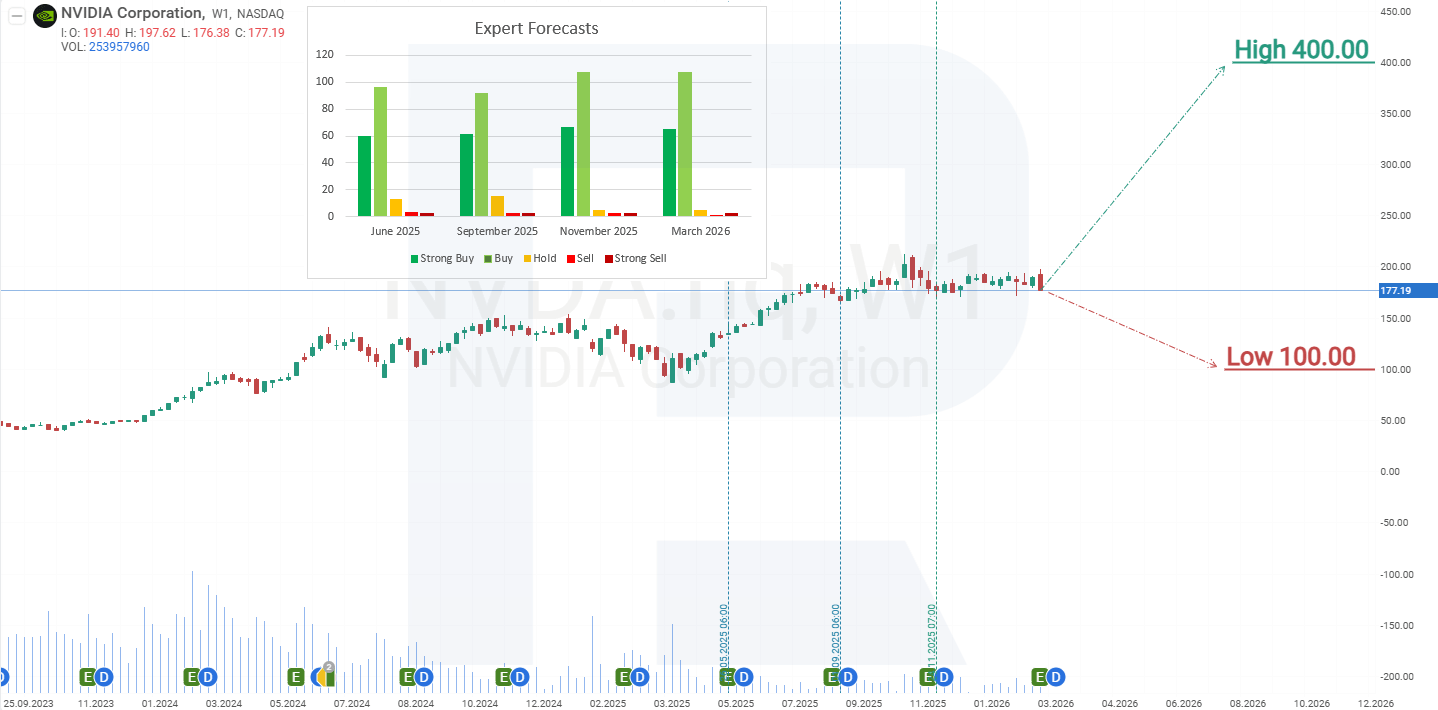

Expert forecasts for NVIDIA Corporation

stock

- Barchart: 45 out of 50 analysts rated NVIDIA shares as a Strong Buy, 3 as Buy, 1 as Hold, and 1 as Strong Sell. The upper price target is 352 USD, and the lower bound is 140 USD.

- MarketBeat: 51 out of 53 specialists assigned a Buy rating to the shares, and 2 gave a Hold recommendation. The upper price target is 400 USD, and the lower bound is 205 USD.

- TipRanks: 37 out of 39 analysts rated the shares as Buy, 1 as Hold, and 1 as Sell. The upper price target is 352 USD, and the lower bound is 220 USD.

- Stock Analysis: 20 out of 38 experts rated the shares as Strong Buy, 16 as Buy, 1 as Hold, and 1 as Strong Sell. The upper price target is 352 USD, and the lower bound is 100 USD.

NVIDIA Corporation stock price forecast for 2025

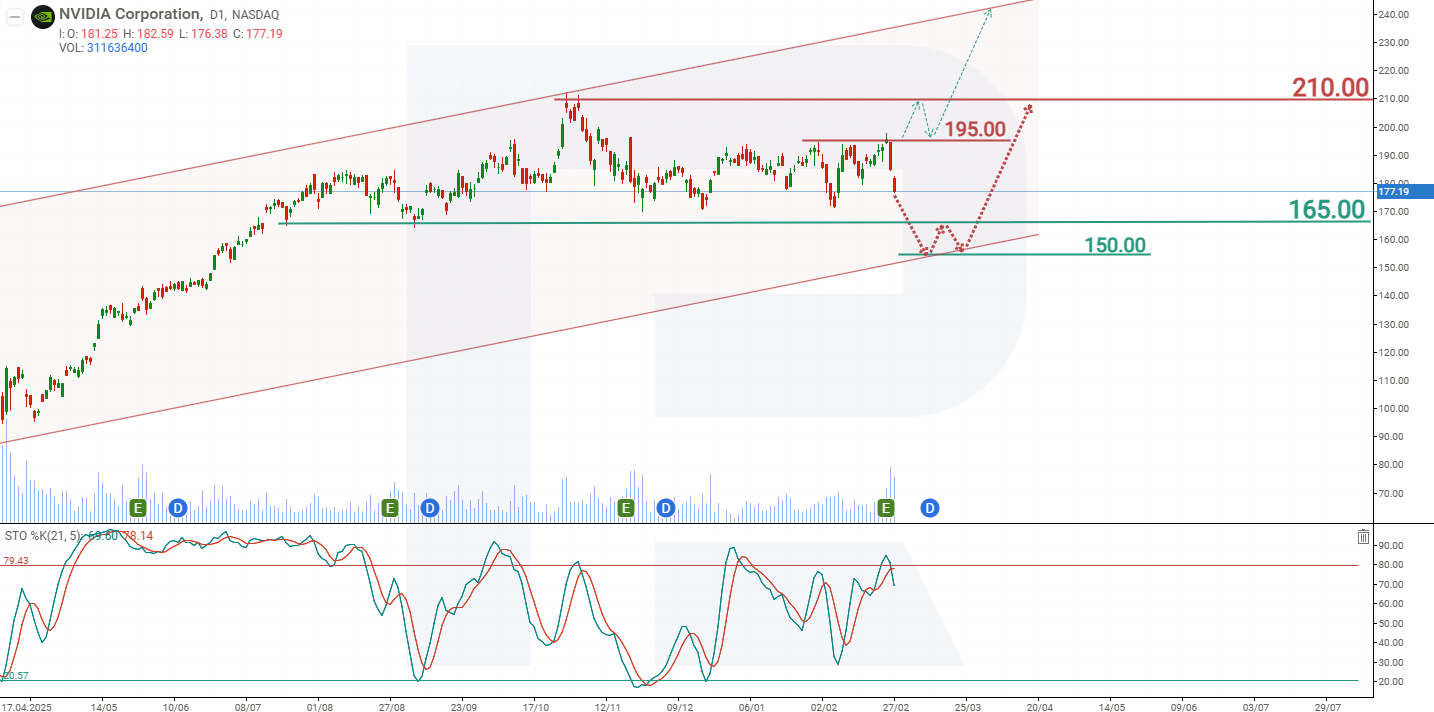

Since October 2025, NVDA’s share price has stalled, with even strong quarterly results failing to reverse this trend. The stock is trading near its historical high, and many market participants are awaiting a correction, despite the positive outlook from management. However, key support for the stock remains the buyback program and robust cash flow generation. The company is actively directing free cash flow toward buybacks, which helps limit the risk of a sharp decline. Based on the current performance of NVIDIA shares, the expected price movements for 2026 are as follows:

The primary forecast for NVIDIA shares suggests a decline within the correction, with support at 150 USD. A rebound from this level would signal the end of the correction and the resumption of price growth within the uptrend. The upward target for NVDA shares would be the resistance level at 240 USD.

The optimistic forecast for NVIDIA stock suggests a breakout above resistance at 195 USD. In this scenario, the stock could quickly reach the resistance level at 240 USD.

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex bears no responsibility for trading results based on trading recommendations described in these analytical reviews.