Meta – stock forecast and key levels for 2026

Following a strong Q4 2025 earnings report, Meta shares have maintained their upward trend despite a corrective pullback. The technical setup points to further upside potential, provided key support levels hold and a moderately positive outlook for 2026 materialises.

Meta Platforms, Inc. (NASDAQ: META) reported strong results for Q4 2025. Revenue reached 59.9 billion USD (+24% year-on-year), reflecting sustained growth and exceeding analysts’ consensus estimates. The company also reported earnings per share of 8.88 USD, significantly surpassing market expectations (around 8.2 USD). Net income increased by 9% compared with Q4 2024, rising to 22.8 billion USD, largely driven by robust advertising monetisation. Meta highlighted that advertising revenue growth was supported by AI-driven product improvements, more precise targeting, and the expansion of its advertising audience across platforms such as Facebook, Instagram, and Reels.

For Q1 2026, the company expects revenue in the 53.5–56.5 billion USD range, reflecting seasonal moderation while maintaining a positive growth trajectory. Management also outlined plans for substantial investment in infrastructure and AI development, which will lead to higher expenses but, in its view, will strengthen the company’s long-term competitive position.

This article reviews Meta Platforms’ business model and revenue structure, presents its recent quarterly results, and provides a fundamental analysis of META. It also outlines expert forecasts for Meta shares in 2026 and examines recent Meta share price performance, forming the basis for the Meta Platforms stock forecast for 2026.

About Meta Platforms, Inc.

Meta Platforms, formerly known as Facebook, was founded in 2004 by Mark Zuckerberg and his Harvard classmates Eduardo Saverin, Andrew McCollum, Dustin Moskovitz, and Chris Hughes. It was initially a social network for Harvard students, but soon expanded to become one of the world’s largest communication platforms. Meta’s core operations include developing social networks such as Facebook, Instagram, and WhatsApp, as well as advancing virtual and augmented reality technologies through its Reality Labs division. The company focuses significantly on developing the metaverse, as reflected in its 2021 rebranding. Meta went public on 18 May 2012, and its IPO ranked among the most prominent tech IPOs in history.

Meta Platforms, Inc.’s main financial flows

Meta Platforms’ revenue mainly comes from the following sources:

- Advertising: this segment accounts for approximately 98.5% of the company’s total revenue. Meta generates advertising revenue through its platforms (Facebook, Instagram, Messenger, and WhatsApp), allowing advertisers to target audiences based on various criteria, including demographic data, user interests, and behaviour.

- Reality Labs: this division generates a smaller portion of the company’s revenue through hardware sales under the Meta Quest (previously Oculus VR) brand and related software products, including content.

- Other revenue: this comprises fees for using Meta’s payment systems (for example, on Marketplace platforms or apps), paid subscriptions for special features or products, and income from other services. While these sources are less significant than advertising, they still contribute to the company’s financial performance.

Thus, Meta Platforms’ primary source of revenue is advertising on its social platforms, followed by income from virtual reality sales and services and additional proceeds from other sources.

Meta Platforms, Inc. Q2 2024 results

Meta announced solid financial Q2 2024 results. Below are the figures compared with the same period in 2023:

- Revenue: 39.74 billion USD (+22%)

- Net income: 13.46 billion USD (+73%)

- Earnings per share: 5.16 USD (+73%)

- Operating margin: 38% (+900 basis points)

- Advertising revenue: 38.20 billion USD (+21%)

- Revenue from Reality Labs: 353 million USD (+27%)

- Loss from Reality Labs: 4.50 billion USD (+21%)

- Number of daily active users: 3.27 billion (+7%)

- Costs and expenses: 24.22 billion USD (+7%)

Advertising remains the primary revenue stream, contributing 96% of the company’s total revenue. The Reality Labs division, which specialises in developing virtual and augmented reality (VR and AR) technologies, has so far only generated losses. By the end of Q2 2024 results, Reality Labs’ loss reached 4.50 billion USD, a 21% increase.

Meta Platforms, Inc. Q3 2024 results

On 30 October, Meta released its Q3 2023 report. Below are the key figures compared with the same period in 2023:

- Revenue: 40.58 billion USD (+19%)

- Net income: 15.68 billion USD (+35%)

- Earnings per share: 6.03 USD (+37%)

- Operating margin: 43% (+300 basis points)

- Advertising revenue: 39.88 billion USD (+18%)

- Reality Labs revenue: 270 million USD (+28%)

- Reality Labs loss: 4.40 billion USD (+20%)

- Number of daily active users: 3.279 billion (+5%)

- Costs and expenses: 23.24 billion USD (+14%)

CEO Mark Zuckerberg explained that revenue growth was driven by advancements in artificial intelligence (AI), which are actively integrated into the company’s applications and business processes. He highlighted Meta AI’s notable success, the rollout of the Llama AI model, and the development of AI-powered smart glasses.

CFO Susan Li shared the company’s forecast, expecting Q4 2024 revenue to range between 45.00 billion and 48.00 billion USD. She also revised the company’s total expense forecast for 2024, lowering it to the 96.00–98.00 billion USD range, down from the previous estimate of 96.00–99.00 billion USD. Li emphasised that the operating losses of the Reality Labs division, which focuses on virtual and augmented reality (VR and AR), would significantly increase year-on-year due to ongoing development and investments aimed at scaling the ecosystem. Additionally, Li mentioned that Meta expects substantial capital expenditure growth in 2025, including increased spending on infrastructure.

Both Zuckerberg and Li also noted the growing number of legal and regulatory challenges, particularly in the European Union and the US, which could significantly affect Meta’s business and financial results.

Overall, Meta’s management expressed optimism about the company’s current performance, driven by progress in AI technologies and strategic investments. However, they also pointed out that external factors could influence future results.

Meta Platforms, Inc. Q4 2024 earnings results

On 29 January 2025, Meta published its earnings report for Q4 2024. Below are the key figures compared with the same period in 2023:

- Revenue: 48.38 billion USD (+21%)

- Net income: 20.83 billion USD (+49%)

- Earnings per share: 8.02 USD (+50%)

- Operating margin: 48% (+700 basis points)

- Advertising revenue: 46.78 billion USD (+20%)

- Reality Labs revenue: 1.08 billion USD (+1%)

- Reality Labs loss: 4.96 billion USD (+6%)

- Number of daily active users: 3.35 billion (+5%)

- Costs and expenses: 25.02 billion USD (+5%)

In his comments on the report, Zuckerberg highlighted advancements in Artificial Intelligence (AI) and expressed optimism about scaling these technologies in 2025, including the introduction of personalised AI assistants. He emphasised the company’s commitment to building an “extensive computing infrastructure,” which implies significant investments in AI. His vision includes creating AI that can write and deploy code, unlocking new opportunities for business and the market.

Zuckerberg also pointed to progress in the development of computerised smart glasses, suggesting that 2025 could be a key year for understanding the market potential of AI-powered glasses.

Regarding DeepSeek, he acknowledged the “groundbreaking” developments that Meta is still trying to comprehend, with plans to integrate some of these innovations into its products. Despite DeepSeek’s achievements, Zuckerberg stated that “it is too early to form a definitive opinion” on how these developments may impact Meta’s infrastructure and capital investment plans. He emphasised that the company’s commitment to large-scale AI infrastructure investment will remain unchanged, viewing it as a long-term strategic advantage.

Zuckerberg noted that DeepSeek is a new competitor in this market. At the same time, the decline in demand for computing resources (GPUs) is by no means certain, as running AI models still requires substantial computing power, especially given the scale of Meta’s operations.

Meta Platforms, Inc. Q1 2025 earnings results

On 30 April, Meta published its Q1 2025 report for the period ended 31 March. Key figures compared with the same period in 2024 are as follows:

- Revenue: 42.31 billion USD (+16%)

- Net income: 16.64 billion USD (+35%)

- Earnings per share: 6.43 USD (+37%)

- Operating margin: 41% (+300 basis points)

- Advertising revenue: 41.39 billion USD (+16%)

- Reality Labs revenue: 0.41 billion USD (-9%)

- Reality Labs loss: 4.21 billion USD (+16%)

- Family daily active people (DAP): 3.43 billion (+6%)

- Costs and expenses: 24.76 billion USD (+9%)

Meta made a confident start to 2025, delivering strong results that surpassed analysts’ expectations. Revenue rose by 16%, while earnings per share increased by 35%, significantly exceeding market forecasts. Advertising remains the primary growth driver, with ad revenue rising by 16.2% due to higher prices and an increase in impressions. Meanwhile, the user base for Meta’s products continues to expand, with daily active users reaching 3.43 billion, up 6% year-on-year.

The company also placed a major focus on artificial intelligence. Meta raised its capital expenditure forecast for 2025 to a 64–72 billion USD range (up from a previous estimate of 60-65 billion USD), allocating investment towards developing data centres and acquiring infrastructure to support its AI initiatives.

For Q2 2025, Meta expected revenue in the range of 42.5–45.5 billion USD, which was in line with analysts’ expectations. However, management highlighted potential short-term risks, including a decline in advertising activity from Asian companies and broader economic uncertainty.

For investors, Meta remains one of the most promising companies in the technology sector. Its strong operational base, growing user base and significant investments in AI make the stock an attractive option for those seeking exposure to innovation and long-term growth.

Meta Platforms, Inc. Q2 2025 earnings results

On 30 July, Meta released its results for Q2 2025, which ended 30 June. Below are the key figures compared with the same period in 2024:

- Revenue: 47.52 billion USD (+22%)

- Net income: 18.34 billion USD (+36%)

- Earnings per share: 7.14 USD (+38%)

- Operating margin: 43% (+500 basis points)

- Advertising revenue: 46.56 billion USD (+16%)

- Revenue from Reality Labs: 0.37 billion USD (+5%)

- Loss from Reality Labs: 4.53 billion USD (–1%)

- Family daily active people (DAP): 3.48 billion (+6%)

- Costs and expenses: 27.07 billion USD (+12%)

Meta Platforms reported revenue of 47.52 billion USD in Q2 2025, up 22% year-on-year, while adjusted earnings per share came in at 7.14 USD – 38% higher than the same period last year and well above analyst expectations of 5.85–5.89 USD. Operating profit rose to 20.44 billion USD, with an operating margin of approximately 43%, up five percentage points from 38% a year earlier.

Meta issued revenue guidance for Q3 2025 in the 47.5–50.5 billion USD range, anticipating a slowdown in growth in Q4 due to a high base of comparison. At the same time, it raised its full-year capital expenditure forecast to 66–72 billion USD, hinting at even higher investment in 2026 to support the expansion of its AI infrastructure and the hiring of specialised talent.

Meta Platforms, Inc. Q3 2025 results

On 29 October 2025, Meta published its financial report for Q3 2025, which ended on 30 September. The key figures, compared with the same period in 2024, are as follows:

- Revenue: 51.24 billion USD (+26%)

- Net income: 2.71 billion USD (–83%)

- Earnings per share: 1.05 USD (–83%)

- Operating margin: 40% (–300 basis points)

- Advertising revenue: 50.08 billion USD (+26%)

- Reality Labs revenue: 0.47 billion USD (+74%)

- Reality Labs loss: 4.43 billion USD (0%)

- Family daily active people (DAP): 3.54 billion (+8%)

- Costs and expenses: 30.71 billion USD (+32%)

Meta reported Q3 2025 results with record revenue of 51.2 billion USD (+26% year-on-year), exceeding market expectations. Operating profit increased by 18%, while the operating margin remained high at 40%. GAAP net income declined due to a one-off tax charge of nearly 16 billion USD. Excluding this effect, the underlying net income would have amounted to 18.6 billion USD, with EPS of 7.25 USD. Therefore, the decline in profit was a technical effect linked to changes in tax legislation, while operationally, Meta delivered one of the strongest quarters in its history.

Meta’s core business – Family of Apps – delivered excellent performance, with revenue and advertising income rising by 26%. Ad impressions increased by 14%, while the average price per ad rose by 10%. Daily active users across the company’s apps reached 3.54 billion (+8%), setting a new record. AI-driven recommendations, including Reels and content algorithms, continue to boost user engagement, particularly in video formats.

The Reality Labs division (AR/VR and AI devices) also increased revenue by 74% to 470 million USD, but remains loss-making. The segment continues to be funded by profits from the advertising business.

Meta raised its full-year expense guidance to 116–118 billion USD and capital expenditure to 70–72 billion USD, which has become the primary source of investor concern. The company is investing aggressively in AI infrastructure and data centres, making the business more capital-intensive.

Management provided a relatively confident outlook for Q4 2025, implying continued strong business momentum. The company expects revenue in the 56–59 billion USD range, representing year-on-year growth of 18–22%. Such a pace suggests ongoing recovery in the advertising market and resilient demand from both large brands and small businesses.

At the same time, Reality Labs is expected to report a slight revenue decline in Q4 compared with Q3. This is explained by the fact that Quest headset sales peaked in Q3 due to channel stocking and new model launches. Meta anticipates that Q4 sales will stabilise but will not act as a key growth driver.

Meta Platforms, Inc. Q4 2025 results

On 28 January, Meta released its Q4 2025 results for the period ended 31 December. Below are the key figures compared with the same period in 2024:

- Revenue: 59.89 billion USD (+24%)

- Net income: 22.76 billion USD (+9%)

- Earnings per share: 8.88 USD (+11%)

- Operating margin: 41% (–700 basis points)

- Advertising revenue: 58.14 billion USD (+24%)

- Reality Labs revenue: 0.96 billion USD (+%)

- Reality Labs loss: 6.21 billion USD (–12%)

- Family daily active people (DAP): 3.58 billion (+7%)

- Costs and expenses: 35.15 billion USD (+40%)

Meta Platforms’ Q4 2025 report exceeded analysts’ expectations. Revenue reached 59.89 billion USD, up 24% year-on-year. One of the key drivers of such strong growth was enhanced monetisation through the expansion and improvement of advertising products. In particular, Reels and Instagram continued to strengthen their market positions, leading to higher engagement metrics and, consequently, increased advertising revenue.

The integration of AI into advertising algorithms improved targeting precision, boosting returns on ad spend and enabling the company to generate more revenue per advertising dollar, thereby supporting further profitability growth. Earnings per share came in at 8.88 USD, significantly above the expected 8.2 USD, while net income rose 9% year-on-year to 22.8 billion USD.

Management’s guidance for Q1 2026 is for revenue in the range of 53.5–56.5 billion USD. Total expenses for 2026 are projected to be 162–169 billion USD. The main drivers of cost growth will be higher infrastructure spending, including cloud services and depreciation, as well as increased employee compensation, particularly to support priority areas such as artificial intelligence. Despite rising infrastructure investment, operating income is forecast to exceed 2025 levels.

The company has also begun implementing changes to its less personalised advertisements offering, in line with agreements reached with the European Commission, while continuing to monitor potential legal risks in the EU and the US that could materially affect its business and financial results.

Analysis of key valuation multiples for Meta Platforms, Inc.

Below are the key valuation multiples for Meta based on Q4 2025 results, calculated using a share price of 690 USD.

| Multiple | What it indicates | Value | Commentary |

|---|---|---|---|

| P/E (TTM) | Price paid for 1 USD of earnings over the past 12 months | 29.4 | ⬤ Given its dominance in the digital advertising market and strong margins, the valuation appears reasonable, although not cheap. |

| P/S (TTM) | Price paid for 1 USD of annual revenue | 8.7 | ⬤ Historically, a range of 5–6 has been considered typical for a mature technology company. |

| EV/Sales (TTM) | Enterprise value to sales, accounting for debt | 8.7 | ⬤ Overvalued on a revenue basis. Given Meta’s scale, sustaining growth rates that justify such a multiple may prove challenging. |

| P/FCF (TTM) | Price paid for 1 USD of free cash flow | 37.9 | ⬤ A high ratio, indicating that investors are paying a substantial premium for free cash flow. |

| FCF Yield (TTM) | Free cash flow yield to shareholders | 2.49% | ⬤ Low yield. US risk-free government bonds yield around 4%, making Meta shares relatively less attractive from the yield perspective. |

| EV/EBITDA (TTM) | Enterprise value to operating profit before depreciation and amortisation | 17.2 | ⬤ Acceptable. The metric is above the broader market average, but for high-quality big tech companies with strong margins, such a premium can be justified. |

| EV/EBIT (TTM) | Enterprise value to operating profit | 21 | ⬤ Within a reasonable range for highly valued companies, although close to the upper bound for more mature businesses. |

| P/B | Price to book value | 8 | ⬤ A very elevated ratio, reflecting high market expectations for the company. |

| Net Debt/EBITDA | Debt burden relative to EBITDA | 0.22 | ⬤ A very low ratio, indicating a strong financial position and low debt burden. |

| Interest Coverage (TTM) | Ability to cover interest expenses with operating profit | 71.4 | ⬤ Significantly above conventional thresholds, signalling an extremely low probability of debt-servicing issues. |

Meta valuation multiples analysis – conclusion

Meta is currently valued by the market primarily based on expectations surrounding AI rather than its current financial results. Investors are betting that artificial intelligence will improve advertising algorithms and create new revenue streams, justifying the high valuation.

For long-term investors, the company remains a benchmark for margin strength and business stability. However, the potential for substantial share price growth from current levels is already limited.

For new buyers, entering a position at a share price of 690 USD carries increased risk, as any slowdown in growth or disappointment regarding the impact of AI could lead to multiple contraction towards more moderate levels, such as a P/E of 20–22. With financial performance unchanged, this could translate into a 20–30% decline in the share price.

Expert forecasts for Meta Platforms, Inc. stock for 2026

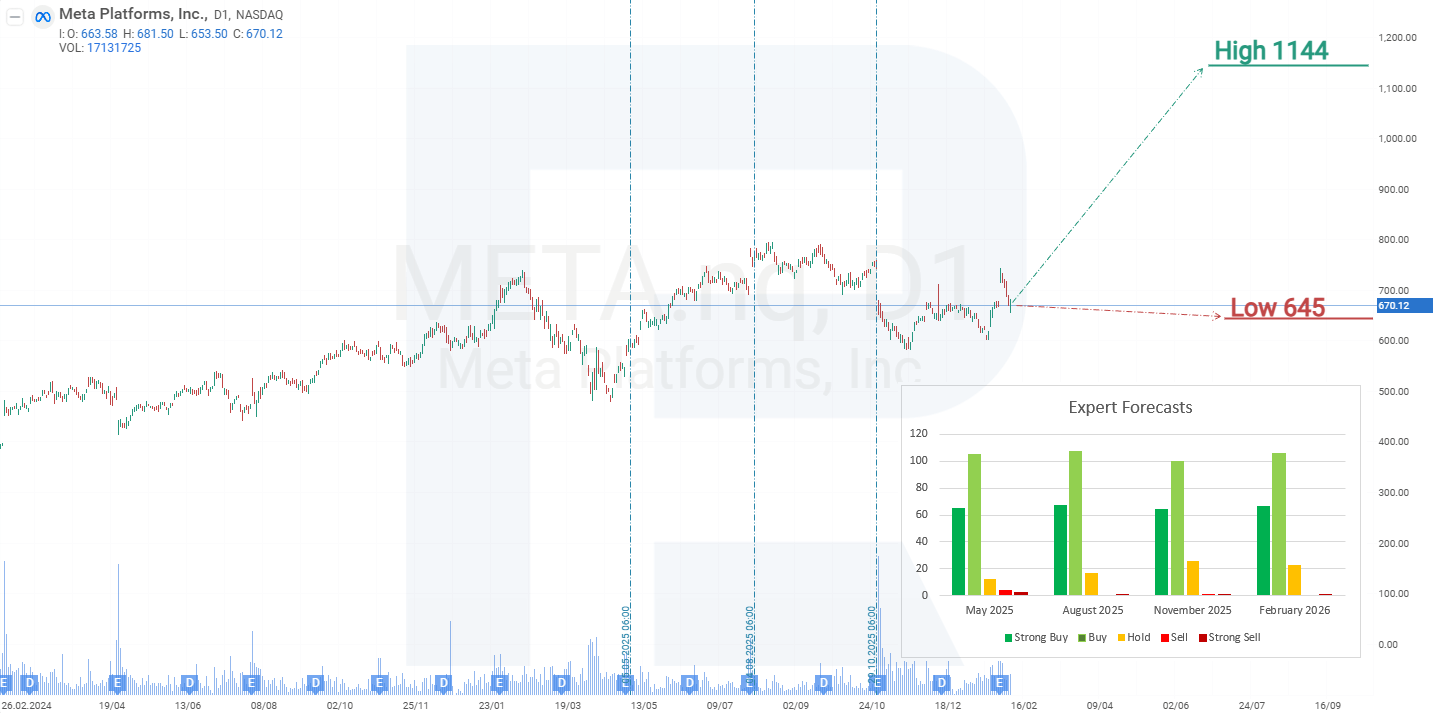

- Barchart: 46 out of 56 analysts rated Meta Platforms shares as Strong Buy, 3 as Buy, 7 as Hold, and 1 as Strong Sell. The upper price target is 1,144 USD, with the lower bound at 700 USD.

- MarketBeat: 46 out of 53 analysts assigned a Buy rating to the shares, and 7 recommended Hold. The upper price target is 1,140 USD, with the lower bound at 605 USD.

- TipRanks: 39 out of 44 analysts rated the shares as Buy, and 5 recommended Hold. The upper price target is 1,140 USD, with the lower bound at 700 USD.

- Stock Analysis: 20 out of 42 experts rated the shares as Strong Buy, 18 as Buy, and 4 as Hold. The upper price target is 1,144 USD, with the lower bound at 645 USD.

Meta Platforms, Inc. stock price forecast for 2026

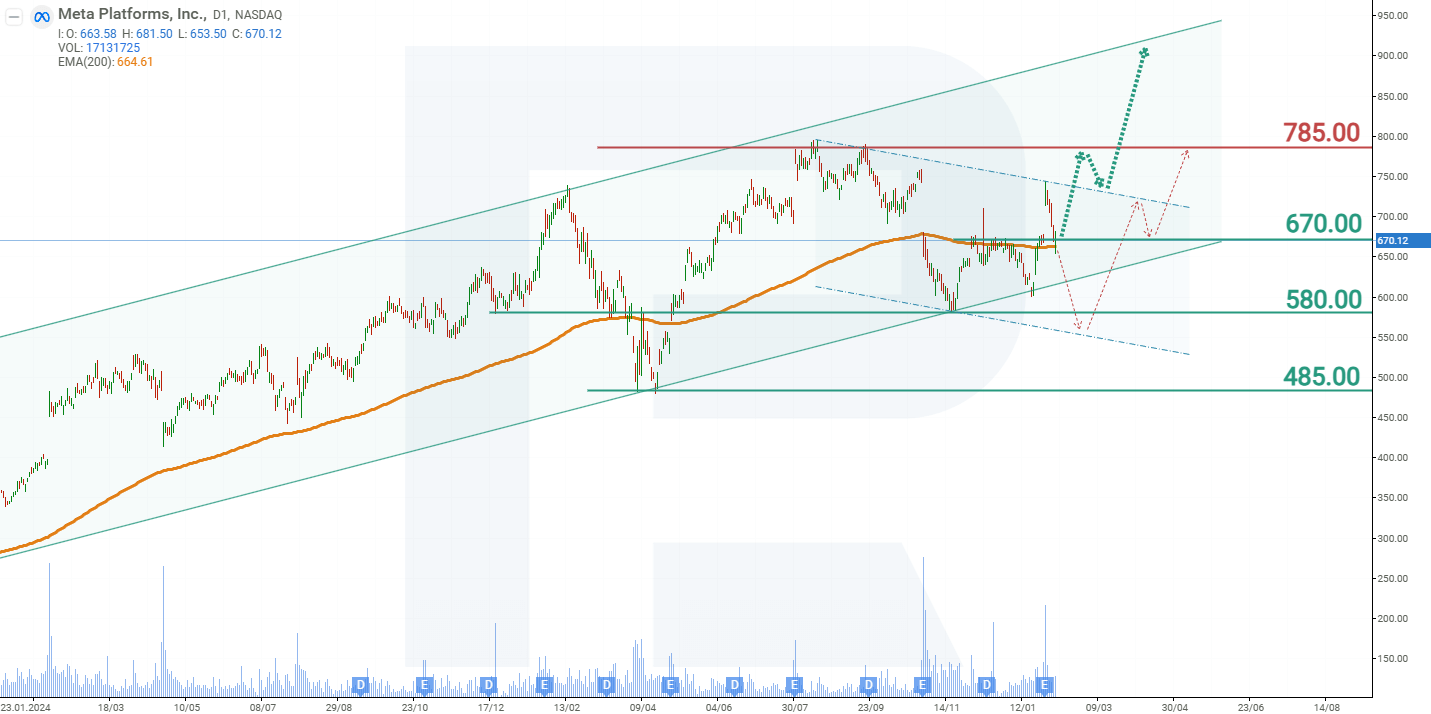

On the weekly chart, Meta Platforms shares are trading within an ascending channel. Following the publication of the Q4 2025 report, which exceeded expectations, the share price surged by 10%, creating a gap on the chart. In most cases, chart gaps are subsequently filled by price action, and this instance was no exception. The following day, quotations moved lower, and by 4 February the gap had been closed. However, despite the pullback in META shares, the overall trend remains upward. Based on the current price performance of Meta Platforms shares, the possible scenarios for 2026 are as follows.

The base-case forecast for Meta Platforms shares suggests a rebound from support at 670 USD, followed by a rise towards resistance at 785 USD. A breakout above this resistance would signal further upside towards the upper boundary of the channel near 900 USD.

The alternative forecast for Meta Platforms stock suggests a break below the 670 USD support level. In this scenario, META shares could decline towards 580 USD, from which a gradual recovery is expected. As the ascending trendline would be breached, further upside may be limited to resistance in the 785 USD area.

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex bears no responsibility for trading results based on trading recommendations described in these analytical reviews.