Oracle – strong quarter and technical analysis signal potential share price growth

Oracle exceeded expectations for revenue and profit in Q3 of the 2026 financial year. Technical analysis of ORCL indicates the stock is likely to continue rising.

Oracle Corporation (NYSE: ORCL) delivered a strong financial performance in Q3 of the 2026 financial year. Revenue rose 22% year-on-year to 17.19 billion USD, while non-GAAP EPS reached 1.79 USD, with both metrics surpassing market expectations. The company highlighted that this was the first quarter in more than 15 years in which both organic revenue growth and non-GAAP EPS exceeded 20% in USD, marking a significant inflexion point in Oracle’s growth trajectory.

The primary growth driver was again the cloud business. Total cloud revenue increased to 8.91 billion USD (+44% y/y), with Oracle Cloud Infrastructure up 84% to 4.89 billion USD and the SaaS segment rising to 4.03 billion USD (+13% y/y). Future contract growth was also notable. Remaining Performance Obligations (RPO) reached 553 billion USD, up 325% year-on-year, underscoring very strong demand for Oracle’s AI infrastructure.

For Q4 2026, Oracle expects revenue growth of 19–21% in USD and non-GAAP EPS of 1.96–2.00 USD. The full-year 2026 revenue target of approximately 67 billion USD has been maintained, while the forecast for 2027 has been raised to 90 billion USD, a key positive takeaway from the report.

This article examines Oracle Corporation, outlining its business model, providing a fundamental analysis of Oracle’s Q3 2026 report, and presenting a technical analysis of ORCL shares based on their current price dynamics. These insights form the basis for the ORCL stock forecast for 2026.

About Oracle Corporation

Oracle Corporation is an American technology company founded in 1977 by Larry Ellison, Bob Miner, and Ed Oates under the original name Software Development Laboratories. Initially, the headquarters were in Austin, Texas. After rebranding to Oracle in 1982, the company specialised in software development and cloud technologies, including database management systems (DBMS), enterprise software, cloud solutions, and infrastructure. The company is renowned for its flagship product, Oracle Database, and is also actively expanding its cloud services (Oracle Cloud), competing with AWS, Google Cloud, and Microsoft Azure.

Oracle went public on 12 March 1986 on the NASDAQ under the ticker symbol ORCL, becoming one of the first technology companies to list on the public market. Today, Oracle is one of the most prominent players in the enterprise technology industry, focusing on business digitalisation and cloud innovations.

Oracle Corporation’s primary sources of revenue

Oracle’s primary sources of revenue are derived from the following business segments:

- Cloud Services and License: this is the largest revenue source, accounting for approximately 86% of total revenue. Oracle provides licences for its software products, such as Java, Oracle Applications, Oracle Database, Oracle Middleware, and others. This segment also includes cloud computing via the Oracle Cloud platform, encompassing IaaS (Infrastructure as a Service), PaaS (Platform as a Service), and SaaS (Software as a Service) models.

- Hardware: approximately 5% of revenue comes from the sale of hardware, including servers, storage systems, and specialised equipment. Production is outsourced to contract partners, with revenue further supplemented by software related to the hardware.

- Services: approximately 9% of revenue is generated from technical support and consulting services. This includes user support for Oracle software, updates, training, and assistance with solution integration. This segment is crucial for customer retention and ensuring stable financial inflows.

Oracle Corporation Q3 2025 financial results

On 10 March, Oracle Corporation released its Q3 2025 financial results for the quarter ended 28 February 2025. Below are the key figures:

- Revenue: 14.13 billion USD (+6%)

- Net profit: 4.23 billion USD (+6%)

- Earnings per share: 1.47 USD (+4%)

- Operating margin: 44.00% (unchanged)

Revenue by segment:

- Cloud services and licence support: 11.00 billion USD (+10%)

- Cloud revenue (IaaS plus SaaS): 6.20 billion USD (+23%)

- Cloud licence and on-premises licence: 1.12 billion USD (–10%)

- Hardware: 703.00 million USD (–7%)

- Services: 1.29 billion USD (–1%)

Oracle’s results for Q3 2025 present a mixed picture, reflecting both achievements and challenges.

Overall revenue of 14.10 billion USD fell short of the 14.40 billion USD forecast by analysts, indicating difficulties in meeting market expectations. Adjusted earnings per share amounted to 1.47 USD, below the expected 1.49 USD, indicating a decline in profitability. Furthermore, while revenue from Cloud services and licence support grew by 10%, it did not reach the anticipated 11.20 billion USD, indicating challenges with the full-scale monetisation of the cloud market.

On a positive note, the company entered strategic partnerships with OpenAI, Meta Platforms (NASDAQ: META), and NVIDIA (NASDAQ: NVDA), which, according to CEO Safra Catz, is expected to drive a 15% revenue increase in the 2026 financial year starting in June of this year. In addition, Oracle plans to double its data centre capacity over the year to meet the growing demand for cloud services. Oracle has also invested in the Stargate project, which aims to develop cloud and network infrastructure for scalable computing and AI applications. For Oracle’s shareholders, the good news was the announcement of a 25% increase in quarterly dividends, raising them to 0.50 USD per share.

Oracle Corporation Q4 2025 financial results

On 11 June, Oracle Corporation released its Q4 2025 results for the quarter ended 31 May. Its key highlights are provided below:

- Revenue: 15.90 billion USD (+11%)

- Net income: 3.42 billion USD (+9%)

- Earnings per share: 1.70 USD (+4%)

- Operating margin: 44.00% (–300 basis points)

Revenue by segment:

- Cloud services and license support: 11.70 billion USD (+14%)

- Cloud Revenue (IaaS plus SaaS): 6.70 billion USD (+27%)

- Cloud license and on-premises license: 2.01 billion USD (+9%)

- Hardware: 850.00 million USD (–2%)

- Services: 1.35 billion USD (–2%)

Oracle Corporation’s Q4 fiscal 2025 report demonstrated the company’s accelerating shift towards a cloud-centric business model. Total revenue rose by 11% year-on-year to 15.9 billion USD, with adjusted EPS reaching 1.70 USD, beating analysts’ expectations. Oracle Cloud Infrastructure (OCI) revenue growth of 52% to 3 billion USD was particularly notable, making this segment the company’s key growth driver.

Management emphasised the strength of Remaining Performance Obligations (RPO), which rose by 41% to 138 billion USD. CFO Safra Catz noted that this figure could more than double in fiscal 2026, providing strong visibility into future revenues. According to the company’s guidance, the cloud segment is expected to accelerate significantly next year, with total cloud revenue projected to rise by over 40% and OCI revenue by more than 70%.

Chairman of the Board and Chief Technology Officer Larry Ellison announced an aggressive expansion of Oracle’s global data centre network, including hundreds of new deployments across its Multi-Cloud and Cloud@Customer platforms. These initiatives, backed by a 25 billion USD investment program, strengthened Oracle’s position in the competitive landscape against major providers such as Amazon Web Services, Microsoft Azure, and Google Cloud. Additionally, the company is actively involved in generative AI initiatives, including providing infrastructure support for AI startups and potential involvement in projects such as the spin-off of TikTok in the US.

The company’s shares gained 14% following the report, which reflected growing investor confidence. Oracle is successfully transitioning from a traditional licensing model to one based on recurring cloud revenues. Nevertheless, investors should consider the company’s high debt burden and relatively elevated valuation multiples compared to competitors.

For fiscal 2026, the company forecasted revenue of at least 67 billion USD, which corresponds to annual growth of 16-17%. Alongside RPO growth and sustained demand for OCI, this forecast created the foundation for continued positive momentum. Thus, Oracle consolidated its status as a serious player in the enterprise cloud infrastructure market, and its strategic investments appeared capable of delivering long-term returns for shareholders.

Oracle Corporation Q1 2026 financial results

On 9 September, Oracle Corporation released its Q1 2026 results for the quarter ended 31 August. The key figures are as follows:

- Revenue: 14.93 billion USD (+12% year-on-year)

- Net income (non-GAAP): 4.28 billion USD (+8% year-on-year)

- Earnings per share (non-GAAP): 1.47 USD (+6% year-on-year)

- Operating margin: 42.00% (–100 bps)

Revenue by segment:

- Cloud: 7.19 billion USD (+28%)

- Software: 5.72 billion USD (–1%)

- Hardware: 670 million USD (+2%)

- Services: 1.35 billion USD (+7%)

Oracle maintained the guidance issued following its Q4 FY2025 report and delivered strong results in Q1 FY2026. Growth was driven primarily by cloud operations, particularly Oracle Cloud Infrastructure (OCI). Although revenue came in slightly below analyst forecasts, the report was received positively by the market, primarily due to the sharp increase in the contract backlog, which underpins future revenues. Total revenue stood at 14.93 billion USD, up 12% year-on-year but down 6% compared with the prior quarter. Non-GAAP operating profit rose to 6.24 billion USD, while net income reached 4.28 billion USD. GAAP EPS was 1.01 USD (down 2%), while non-GAAP EPS came in at 1.47 USD (+6%). Although just below expectations, a major positive was the surge in Remaining Performance Obligations (RPO) to 455 billion USD, up 359% from the previous year.

The revenue mix shifted further towards cloud. The cloud segment contributed 7.19 billion USD (+28% year-on-year), now accounting for nearly half of total revenue. Software revenue declined to 5.72 billion USD, while Hardware rose to 670 million USD and Services to 1.35 billion USD.

Capital returns to shareholders remain limited. In the quarter, Oracle repurchased about 0.4 million shares worth 93 million USD and declared its regular quarterly dividend of 0.50 USD per share, payable in October. Despite robust operating cash flow over the past twelve months (21.5 billion USD), the company is currently spending more than it generates: free cash flow over the same period was –5.88 billion USD. This reflects record investment in data centres, as Oracle rapidly expands capacity for cloud and AI workloads. In FY 2026, the company plans to spend approximately 35 billion USD on building out such infrastructure.

Management expects the cloud business to accelerate. In Q2 FY2026, Oracle forecasts total revenue growth of 12–14% in constant currency and EPS in the 1.61–1.65 USD range. Cloud revenue is projected to rise by more than 30%. The company raised guidance for OCI separately with an expected 77% year-on-year growth to 18 billion USD, with a long-term target of 144 billion USD by FY2030. Oracle also reported large-scale collaborations with major cloud providers (Microsoft Azure, AWS and Google Cloud) and the construction of 71 joint data centres, 37 of which are already in the launch phase. Database revenue in the multi-cloud environment increased more than fifteenfold year-on-year. Among Oracle’s key partners are OpenAI, xAI, Meta, NVIDIA and AMD, all of which are actively using OCI for AI workloads.

Oracle Corporation Q2 2026 financial results

On 10 December, Oracle Corporation released its Q2 2026 results for the quarter ended 30 November. The key figures are as follows:

- Revenue: 16.06 billion USD (+14%)

- Net income (non-GAAP): 6.60 billion USD (+57%)

- Earnings per share (non-GAAP): 2.26 USD (+54%)

- Operating margin: 41.85% (–151 bps)

Revenue by segment:

- Cloud: 7.98 billion USD (+34%)

- Software: 5.88 billion USD (–3%)

- Hardware: 0.78 million USD (+7%)

- Services: 1.43 billion USD (+7%)

Oracle’s report for Q2 of the 2026 financial year proved mixed: earnings exceeded expectations, while revenue and guidance were slightly disappointing. Revenue increased by 14% year on year to 16.1 billion USD, coming in just below the market forecast (around 16.2 billion USD). Non-GAAP earnings per share amounted to 2.26 USD, significantly above expectations (~1.64 USD), largely due to one-off income from the sale of a stake in Ampere, which added 2.7 billion USD. Non-GAAP operating profit rose to 6.7 billion USD (+10% y/y), while net income increased to 6.6 billion USD (+57% y/y).

The main growth driver was the cloud business, with total revenue from cloud services reaching 7.98 billion USD (+34% y/y), of which infrastructure posted growth of 66–68% y/y to 4.1 billion USD. Cloud applications generated 3.9 billion USD (+11% y/y). At the same time, remaining performance obligations (RPO) surged to 523 billion USD (+438% y/y), including new large agreements with Meta (NASDAQ: META), NVIDIA (NASDAQ: NVDA), and others, confirming strong demand for Oracle’s AI infrastructure.

Cash flows and guidance were the weaker points of the report. Over the past 12 months, operating cash flow totalled around 22.3 billion USD (+10% y/y). However, due to heavy investment in data centres (CapEx of 35.5 billion USD, including 12 billion USD in Q2), free cash flow turned negative at around –13 billion USD. Debt rose above 110 billion USD, raising concerns among investors.

The company continues to pay a stable quarterly dividend: the board of directors declared a dividend of 0.50 USD per share, with a record date of 9 January 2026 and a payment date of 23 January 2026. In the first six months of the 2026 financial year, Oracle returned approximately 2.85 billion USD to shareholders through dividends, meaning the company distributes a significant portion of its operating cash flow while simultaneously funding its substantial investment program in cloud and AI infrastructure. Share buybacks during this half-year were modest: according to available data, Oracle repurchased its own shares for approximately 95 million USD, far less than dividend payments and the volume of debt raised. In effect, the current focus of capital returns is on dividends rather than aggressive share buybacks.

The company left its full-year revenue guidance unchanged at 67 billion USD but provided cautious guidance for Q3: revenue growth of 16–18% in constant currency and earnings per share of 1.64–1.68 USD, which is below consensus expectations (1.72 USD). In addition, Oracle raised its annual capital expenditure plan to 50 billion USD (previously 35 billion USD), continuing to invest heavily in AI data centres. As a result, questions remain over the timing of a return to sustainably positive free cash flow.

Oracle Corporation Q3 2026 financial results

On 10 March, Oracle Corporation (NYSE: ORCL) released its Q3 2026 financial results for the quarter ended 28 February. Key figures are as follows:

- Revenue: 17.19 billion USD (+22%)

- Net income (non-GAAP): 5.22 billion USD (+23%)

- Earnings per share (non-GAAP): 1.79 USD (+21%)

- Operating margin: 42.92% (–192 bps)

Revenue by segment:

- Cloud: 8.91 billion USD (+44%)

- Software: 6.12 billion USD (+3%)

- Hardware: 0.71 billion USD (+2%)

- Services: 1.44 billion USD (+12%)

Oracle delivered a very strong Q3 2026 performance. Revenue reached 17.19 billion USD, up 22% year-on-year, exceeding market expectations. Adjusted EPS came in at 1.79 USD, also above consensus forecasts.

The cloud business remained the main growth driver. Total cloud revenue rose 44% to 8.91 billion USD, with Oracle Cloud Infrastructure up 84% to 4.89 billion USD and SaaS revenue increasing 13% to 4.03 billion USD. Database solutions also performed strongly, with multicloud revenue rising 531% year-on-year.

However, cash flow and debt remain areas of concern. Capital expenditures on data centres reached 48.3 billion USD, and free cash flow remained negative at –24.7 billion USD. Total debt at the end of February 2026 was 134.6 billion USD, higher than the previous quarter.

Oracle’s outlook for the coming quarters is robust. For Q4 2026, the company expects revenue growth of 19–21% in USD, in line with market expectations and exceeding consensus EPS, with adjusted EPS forecast at 1.96–2.00 USD. This underscores expectations for continued stable growth, particularly in the cloud and AI segments.

The company has maintained its full-year 2026 revenue target of 67 billion USD. Notably, the revenue forecast for FY 2027 has been raised to 90 billion USD, a key factor driving the positive market reaction. This increase reflects rising demand for Oracle’s solutions, including AI, and the ongoing shift of business to cloud technologies and associated services.

Oracle also plans continued investment in its data centres, which could increase capital expenditures to 50 billion USD in 2026. Despite this elevated CapEx, the company expects its financial position to remain solid and anticipates maintaining healthy profitability and cash flow, supported by strong demand for AI and cloud solutions.

Analysis of key valuation multiples for Oracle Corporation

Below are the key valuation multiples for Oracle Corporation based on Q3 2026 financial results, calculated using non-GAAP metrics at a share price of 155 USD.

| Multiple | What it indicates | Value | Comment |

|---|---|---|---|

| P/E (TTM) | Price paid for 1 USD of earnings over the past 12 months | 35.5 | ⬤ A high level for a mature, large-scale software business. |

| P/S (TTM) | Price paid for 1 USD of annual revenue | 9.0 | ⬤ Extremely expensive relative to revenue. |

| EV/Sales (TTM) | Enterprise value to sales, accounting for debt | 10.4 | ⬤ Considering the company’s substantial debt, the business is valued at more than 10x annual revenue, which represents a very aggressive valuation. |

| P/FCF (TTM) | Price paid for 1 USD of free cash flow | n/a | ⬤ Free cash flow has been negative in recent quarters due to record CapEx on data centres. |

| FCF Yield (TTM) | Free cash flow yield to shareholders | negative | ⬤ Oracle is burning cash to fund its AI infrastructure. At present, there is no tangible cash return for shareholders. |

| EV/EBITDA (TTM) | Enterprise value to operating profit before depreciation and amortisation | 24.2 | ⬤ A very high multiple for a business of this size and stage of development. |

| EV/EBIT (TTM) | Enterprise value to operating profit | 34.2 | ⬤ Slow and less profitable payback on AI projects leaves almost no margin of safety at this valuation level. |

| P/B | Price to book value | 14.7 | ⬤ Significant premium to book value, particularly against the backdrop of rising debt. |

| Forward price-to-earnings (P/E) ratio | 19.5 | ⬤The market expects significant profit growth, but the valuation remains high. | |

| Net Debt/EBITDA | Debt burden relative to EBITDA | 3.4 | ⬤ Debt already exceeds comfortable levels. |

| Interest Coverage (TTM) | Ability to cover interest expenses with operating profit | 4.7 | ⬤ Interest coverage remains reasonable for now but rising debt and borrowing costs erode the margin of safety. |

Valuation multiples analysis for Oracle Corporation – conclusion

Oracle currently appears strong operationally, but is expensive in terms of valuation and carries a heavy cash flow burden. Almost all valuation multiples are already in the high range. Moreover, the TTM profit picture is slightly inflated, as GAAP profit in Q2 2026 benefited from a one-time pre-tax gain of 2.7 billion USD from the sale of the Ampere stake, making the earnings-based valuation even more demanding in reality.

The main risk now is not reported earnings, but negative free cash flow. In recent quarters, Oracle has sharply increased CapEx on data centres and AI infrastructure, pushing trailing four-quarter FCF deeply into negative territory. This implies that the current share price is primarily driven by expectations of future returns from AI investments rather than current cash generation.

The balance sheet also raises concerns. A Net Debt/EBITDA ratio of 3.4 and interest coverage of 4.7 indicate that debt remains serviceable, but the margin of safety is already noticeably narrower. In other words, Oracle is currently a bet on whether its large-scale investments in AI and cloud infrastructure will quickly convert into profit and cash. If they do, the current valuation may hold; if not, the stock is likely to remain under pressure.

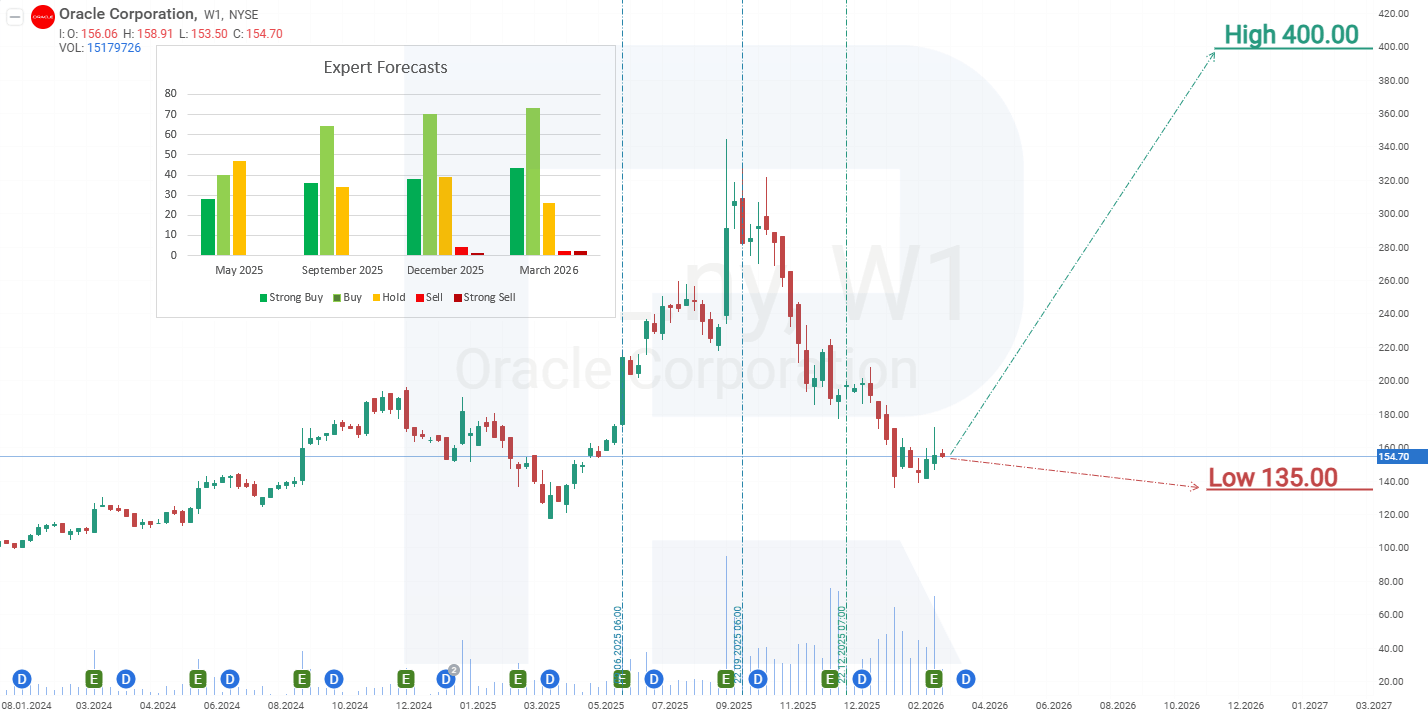

Expert forecasts for Oracle Corporation stock for 2025

- Barchart: 32 out of 42 analysts rated Oracle Corporation shares as a Strong Buy, 1 as a Buy, 8 as Hold, and 1 as a Strong Sell. The upper price target is 400 USD, and the lower bound is 155 USD.

- MarketBeat: 30 out of 40 analysts assigned a Buy rating to the shares, 9 recommended Hold, and 1 recommended Sell. The upper price target is 400 USD, and the lower bound is 135 USD.

- TipRanks: 27 out of 31 analysts rated the shares as Buy, 4 as Hold, and 1 as Sell. The upper price target is 400 USD, and the lower bound is 149 USD.

- Stock Analysis: 11 out of 34 experts rated the shares as a Strong Buy, 17 as Buy, 5 as Hold, and 1 as a Strong Sell. The upper price target is 400 USD, and the lower bound is 160 USD.

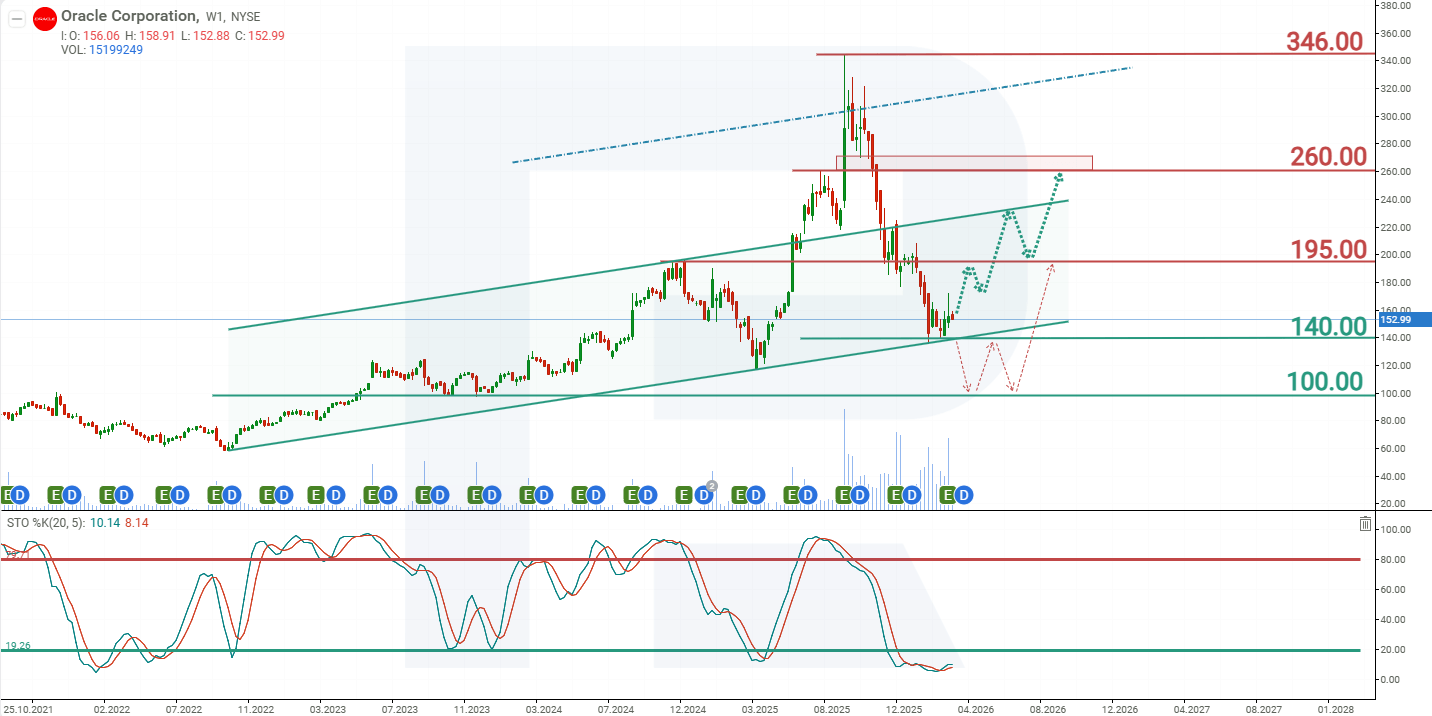

Oracle Corporation stock price forecast for 2026

From April to September 2025, ORCL shares surged 193%, surpassing all key resistance levels and reaching a record high of 346 USD. Given such a rapid rally, the likelihood of a correction increased, and it materialised soon after. Rising debt levels and negative free cash flow concerned investors, prompting sell-offs and a roughly 60% decline from the record high. Such a significant drop undermines confidence in the company. On the other hand, most investors who wished to exit ORCL shares have already done so, and few remain looking to profit from further declines, as evidenced by a Short Float of just 1.84%.

As of March 2026, the shares are trading at the trendline, which acts as support. An additional support factor is the Stochastic indicator, which remains in oversold territory. Based on the current performance of Oracle shares, the potential price scenarios for 2026 are as follows:

The primary forecast for Oracle Corporation shares anticipates a rise in ORCL towards resistance at 195 USD. A break above this level would signal further upside towards 260 USD. However, for this scenario to materialise, the company must achieve positive free cash flow.

The alternative forecast for Oracle stock assumes a test of support at 100 USD, where investor interest in the shares is expected to increase, potentially driving ORCL back towards resistance at 195 USD.

Risks of investing in Oracle Corporation stock

Investing in Oracle Corporation’s shares is associated with several risks that could negatively affect the company’s revenues and impact its investors. Below are the main risks:

#.Intense competition in cloud computing: Oracle faces fierce competition from giants such as Alphabet Inc. (NASDAQ: GOOG), Amazon.com, Inc. (NASDAQ: AMZN), and Microsoft Corporation (NASDAQ: MSFT), which dominate the cloud technology market. If Oracle fails to implement innovations fully and offer competitive pricing, it may lose market share, thereby reducing its revenues.

#.Economic downturns: Oracle’s business model is enterprise-focused and reliant on corporate IT budgets. During recessions or economic slowdowns, companies may delay or reduce spending on software, cloud services, or hardware upgrades, which would directly impact Oracle’s revenues.

#.Limited infrastructure scalability: with rapidly growing demand for cloud services, particularly from AI-related projects, Oracle may face a shortage of computing capacity. Despite the announced data centre expansion plans and significant capital investment, the process of ramping up infrastructure takes time and resources. This may delay the execution of contracts and revenue recognition and even lead to client attrition to competitors with more scalable architectures. As a result, short-term revenue growth may be limited despite strong demand.

#.Infrastructure constraints and execution risks for AI projects: amid explosive demand for cloud and AI services, Oracle is aggressively expanding its data centre capacity, but the construction and commissioning of infrastructure take time and require substantial capital outlays. The company is already facing delays in certain AI-focused data centre projects, including those for major clients such as OpenAI. This creates risks of delayed contract execution, delayed revenue recognition, and a potential reallocation of some demand to competitors that can scale infrastructure more quickly.

#.Rising debt burden and credit risk: to finance AI investments, Oracle has issued tens of billions of USD in bonds in recent years, pushing total debt above 100 billion USD, while free cash flow has turned negative amid record CapEx. The company is becoming increasingly dependent on external financing, and bondholders require regular fixed payments, unlike shareholders, who may tolerate negative FCF in anticipation of future growth. Against this backdrop, the cost of default insurance for Oracle (CDS) has risen to its highest level since 2009, reflecting an elevated market perception of credit risk. If conditions in debt markets deteriorate, the company may be forced to cut back on CapEx, slowing the rollout of AI infrastructure, or raise capital on less favourable terms.

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex bears no responsibility for trading results based on trading recommendations described in these analytical reviews.