Market Week Ahead (June 22–26): Will the USD Pass June's Final Test?

13 minutes for reading

Markets enter the final week of June under elevated uncertainty, shaped by a hawkish Fed and renewed volatility in oil. The Fed held rates at 3.75% last week, but Chair Warsh's commentary and the updated projections sent a clear message: rates will stay restrictive for as long as the inflation outlook demands. Oil added its own layer of turbulence, first falling sharply on reports of a potential US-Iran deal, then recovering as news of a renewed Ormuz Strait closure reignited supply concerns. In this article we have prepared an analysis of the week's key data releases: from Canada's CPI on Monday to the final US GDP and Core PCE on Thursday, with Australia's inflation and the Fed's annual bank stress tests in between. Inside, you'll find technical reference points, key price levels and the latest market sentiment across leading assets.

In Brief

- Canada CPI (Monday, June 22) — the key inflation reading for Bank of Canada rate expectations in H2.

- Australia CPI (Wednesday, June 24) — the RBA's main policy input, with a direct read-through to AUD.

- Fed Bank Stress Tests (Wednesday, June 24) — annual check on the resilience of major US lenders and their dividend capacity.

- Australia Labour Market (Thursday, June 25) — jobs data to complete the picture on the Australian economy.

- US Final GDP Q1 and Core PCE (Thursday, June 25) — the week's defining releases for the dollar and Fed rate expectations.

The central question this week is whether US data validates the Fed's hawkish stance or gives markets any reason to revisit rate expectations. Final GDP and Core PCE on Thursday carry the most weight for the dollar and FX majors.

On the commodity and currency side, Canada's CPI on Monday provides the first test for the loonie, while Australia faces a two-day double release: inflation on Wednesday and jobs figures on Thursday.

Key Events of the Week

| Date | Event | Instruments | Importance |

|---|---|---|---|

| Mon, Jun 22 | Canada CPI | USD/CAD, Canadian bonds, Oil | ●●● High |

| Wed, Jun 24 | Australia CPI | AUD/USD, Australian bonds, Gold | ●●● High |

| Wed, Jun 24 | Fed Bank Stress Test Results | US Banking Sector, S&P 500 Financials, Risk Appetite | ●● Medium |

| Thu, Jun 25 | Australia Labour Market | AUD/USD, AUD/JPY | ●● Medium |

| Thu, Jun 25 | US Final GDP Q1 + Core PCE | EUR/USD, USD Index, Gold, S&P 500 | ●●● High |

Instant Access to Global Markets with RoboForex MobileTrader

22

Jun

Forecast

2.9% y/y

Previous

2.8% y/y

Why It Matters

After the Bank of Canada held rates at its last meeting, investors are reassessing the odds of further action in the second half of the year. Inflation remains the central input for that decision. Any acceleration beyond the consensus forecast would push back easing expectations and shift the debate toward whether a hike is back on the table.

Market Reaction

A CPI reading above forecast would support the Canadian dollar and pull USD/CAD lower as markets adjust BoC rate expectations upward. A miss would reinforce the case for a prolonged hold and add room for the pair to extend its current advance. Oil will amplify or dampen the move depending on the direction of Brent at the time of the release.

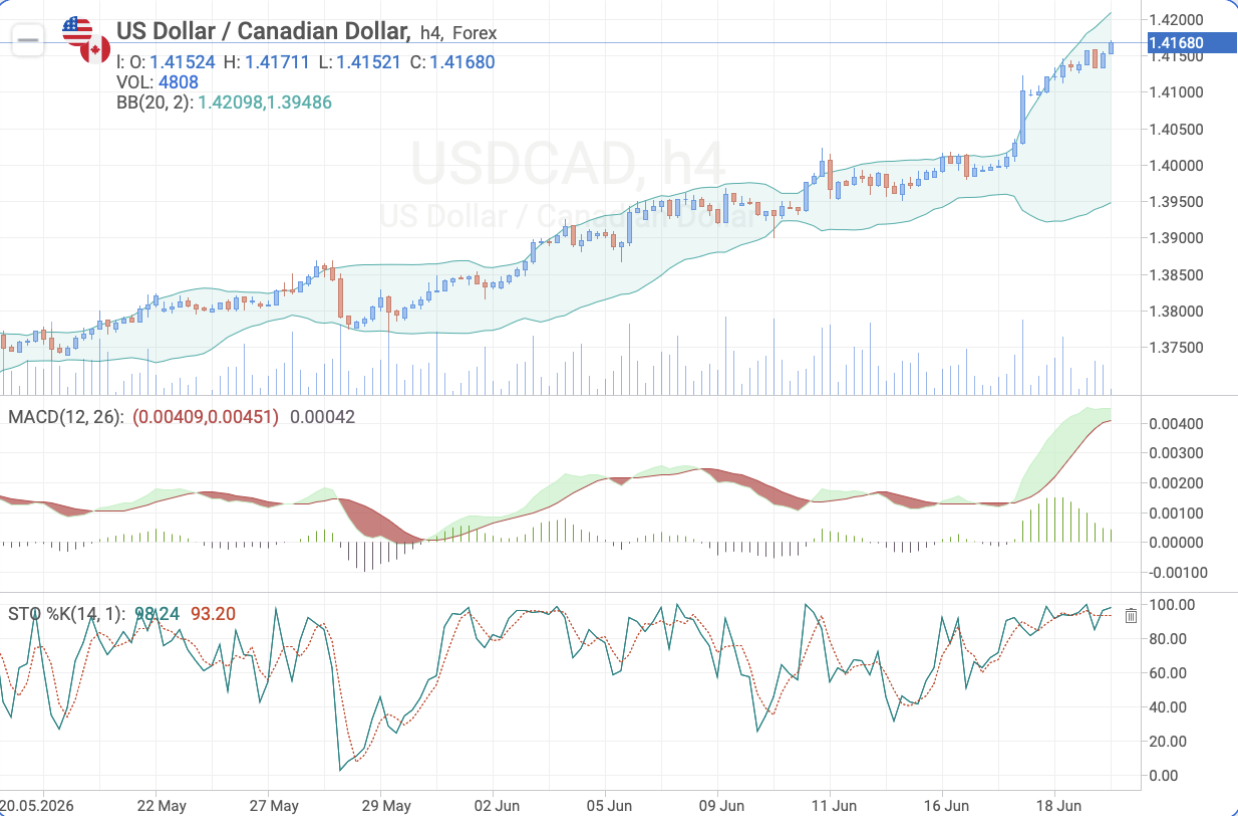

Market Sentiment

Sentiment on USD/CAD remains clearly bullish. The pair has been in a steady uptrend since late May, consolidating at multi-month highs near the upper Bollinger Band at 1.4210. MACD is positive and accelerating, confirming momentum. The stochastic oscillator is deep in overbought territory at 98, which flags the risk of a brief consolidation, but the underlying trend structure remains intact. A CPI beat would give the loonie temporary support, though the broader bias favours continued USD strength while the pair holds above 1.4100.

Source: RoboForex. Past performance is not indicative of future results.

Key Levels — USD/CAD

| Level | Value |

|---|---|

| Resistance | 1.4200 / 1.4250 |

| Support | 1.4100 / 1.4000 |

| Target | 1.4200 |

24

Jun

Forecast

4.4% y/y

Previous

4.2% y/y

Why It Matters

Inflation is the Reserve Bank of Australia's primary policy input. After the RBA held rates at its last meeting, the market is watching closely for signs of a renewed price acceleration. A reading above forecast would revive the debate around further tightening and provide a meaningful lift for the Australian dollar.

Market Reaction

A stronger-than-expected CPI would support AUD/USD and bring RBA tightening expectations back into focus. A soft reading would add downward pressure on the pair and give sellers room to push toward the 0.6950 support zone. Gold may also react to the Australian inflation data, given its sensitivity to global inflation signals.

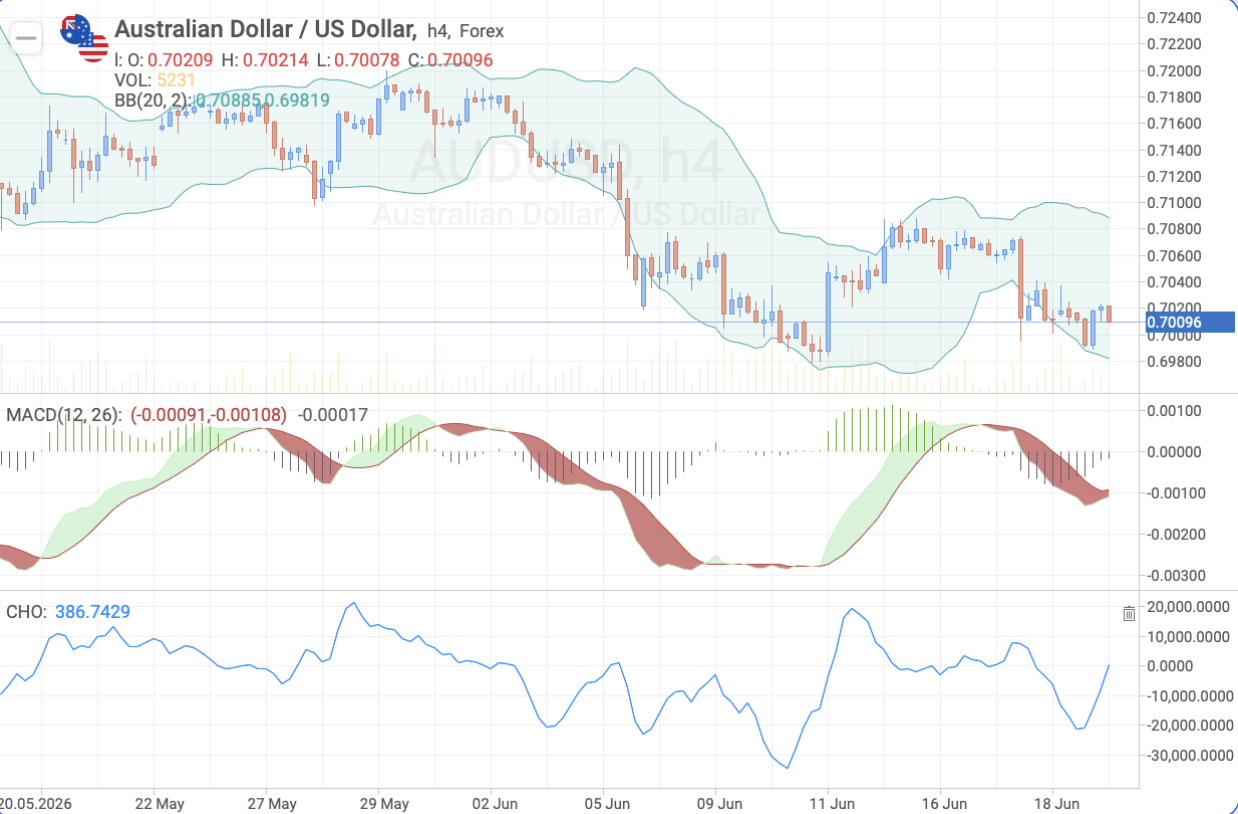

Market Sentiment

Consensus on AUD/USD remains moderately negative. The pair has been under sustained pressure following a series of weak sessions and is currently trading near the 0.700 psychological level, close to the lower Bollinger Band at 0.6982. MACD is in negative territory, though the Chaikin Oscillator has started turning up from deeply negative readings, suggesting some buying interest is returning at these levels. The overall price structure favours the downside. A CPI miss would accelerate a move toward 0.6950; a beat could trigger a short-covering rally toward 0.7040.

Source: RoboForex. Past performance is not indicative of future results.

Key Levels — AUD/USD

| Level | Value |

|---|---|

| Resistance | 0.7040 / 0.7080 |

| Support | 0.6990 / 0.6950 |

| Target | 0.6950 |

24

Jun

Why It Matters

Each year the Fed runs major US banks through hypothetical crisis scenarios to assess their resilience. The results determine directly how much capital banks can return to shareholders through dividends and buybacks. Following the regional banking stress of recent years, investors are giving these results considerably more attention than they did historically. Strong outcomes would open the door to increased capital distributions across the financial sector.

Market Reaction

Solid stress test results would lift financial sector stocks and support broader risk appetite. Weakness in any major lender's results would pressure the S&P 500 Financials index and weigh on the wider market. The broader equity reaction tends to be limited unless results surprise significantly in either direction.

Market Sentiment

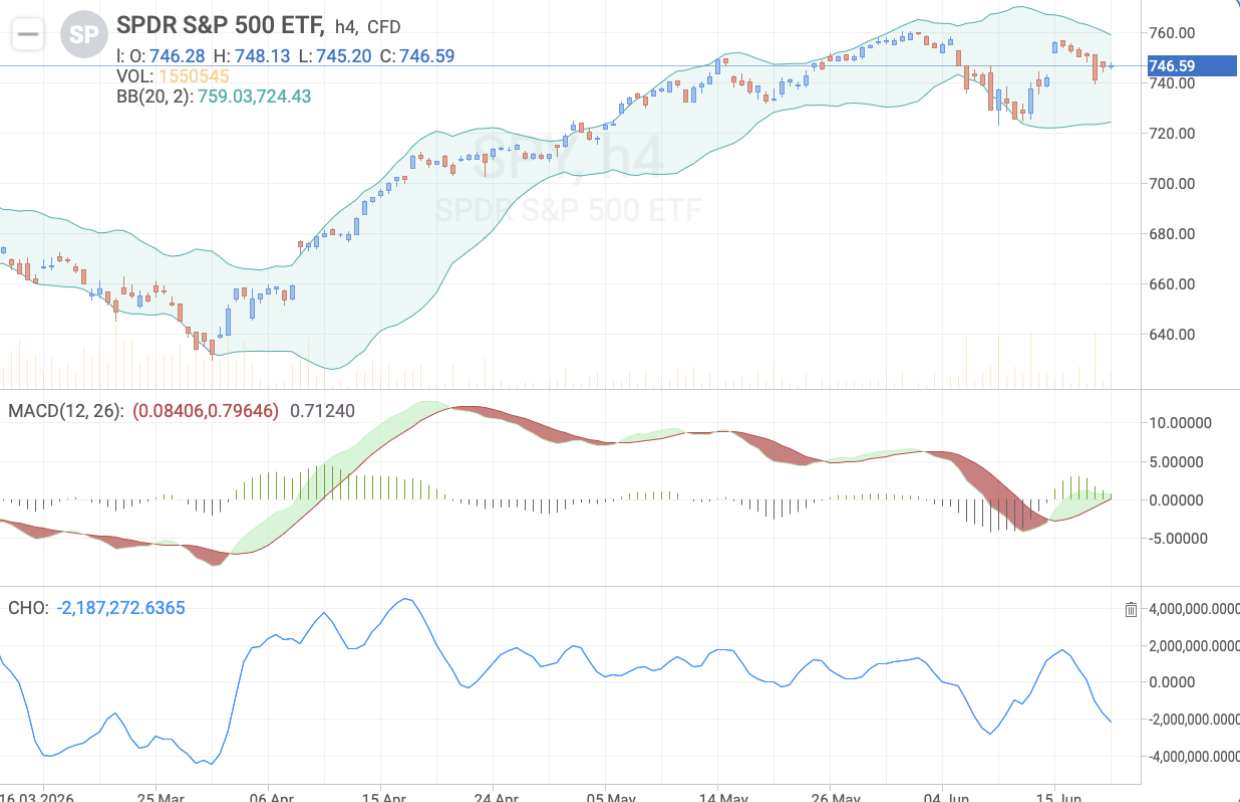

Equity sentiment is cautiously constructive. The S&P 500 stabilised above the 740 support zone following the early-June correction and MACD is crossing back into positive territory, suggesting the worst of the selling pressure has passed. The Chaikin Oscillator remains negative, pointing to continued caution among institutional participants. Strong stress test results could provide additional fuel for a recovery toward the upper Bollinger Band near 759. While the index holds above 740, the near-term bias is to the upside.

Source: RoboForex. Past performance is not indicative of future results.

Key Levels — S&P 500

| Level | Value |

|---|---|

| Resistance | 760 / 770 |

| Support | 740 / 725 |

| Target | 760 |

25

Jun

GDP Forecast / Core PCE

+1.6% q/q / +0.2% m/m

Previous

+1.6% q/q / +0.2% m/m

Why It Matters

This is the week's defining release for the US dollar. The final GDP reading will confirm how durable growth was in Q1, while Core PCE — the Fed's preferred inflation gauge — will show how much price pressure persisted over the same period. Together, these figures will either validate or challenge the hawkish stance the Fed confirmed last week. Any deviation from the consensus, even modest, is likely to move dollar pairs sharply given where rate expectations currently stand.

Market Reaction

Data coming in above consensus on both fronts would reinforce the case for rates staying higher through year-end, supporting the dollar and pushing EUR/USD lower. Softer readings would give markets reason to reassess the pace of tightening and trigger a dollar pullback, with EUR/USD and gold likely to see the sharpest recovery.

Market Sentiment

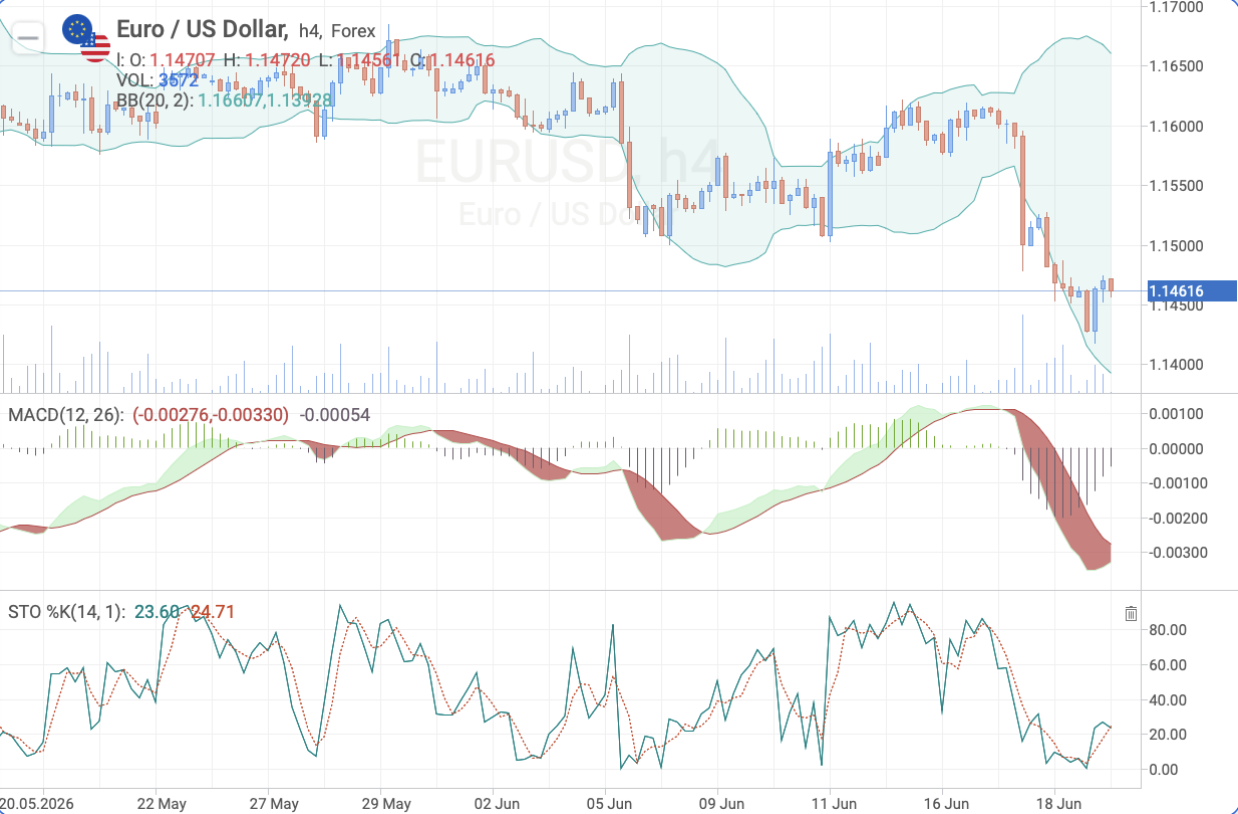

Following last week's Fed meeting, the market remains moderately bullish on the US dollar. EUR/USD has been in a sustained decline since early June and is currently trading near 1.1460, close to the lower Bollinger Band at 1.1393. MACD is deeply negative, and the stochastic oscillator is approaching oversold levels at 23, which raises the probability of a short-term technical bounce. However, the downtrend structure remains firmly intact. Strong GDP and Core PCE data would extend the move toward 1.1400; only a meaningful miss would give EUR/USD room for a meaningful recovery toward the 1.1500 resistance zone.

Source: RoboForex. Past performance is not indicative of future results.

Key Levels — EUR/USD

| Level | Value |

|---|---|

| Resistance | 1.1500 / 1.1600 |

| Support | 1.1450 / 1.1400 |

| Target | 1.1400 |

Track the forecasts and actual figures for each event — the gap between consensus and actual readings is what determines how sharply prices move. Learn more about how to read the economic calendar and trade the news.

Conclusion

The week closes out June with a concentrated run of data that will settle several open questions. Canada's CPI on Monday and Australia's inflation and jobs releases on Wednesday and Thursday give commodity currency traders two distinct set-ups on either side of the week. The Fed's stress test results on Wednesday matter for bank stocks and broader risk appetite.

Thursday's US data carries the most weight. If Final GDP and Core PCE land in line with or above consensus, the dollar's recent recovery gains firmer ground and the "higher for longer" case gets another data point in its favour. A softer outcome would give markets the first tangible reason to revisit rate expectations — and that shift could be felt across FX, equities and gold simultaneously.

Any information provided in articles on this website is based solely on the personal opinions of the authors. These articles should not be construed as trading recommendations or a call to action. The authors and RoboForex accept no responsibility for the results of any trades made on the basis of these recommendations and reviews. Past performance is not indicative of future results. Trading stocks and CFDs involves a high risk of capital loss.